The Big Picture

The US labor market appears to have found its (perhaps temporary) footing — albeit on lower ground. After three years of cooling from pandemic-era highs, the data increasingly suggest that the labor market, especially demand, has started to bump along the bottom. Job postings, unemployment, and openings have all been oscillating in a narrow range since late last year, even as month-to-month volatility and geopolitical uncertainty make any single reading hard to interpret. The low-hire, low-fire dynamic persists, but it may now be better understood as a new steady state rather than an ongoing deterioration.

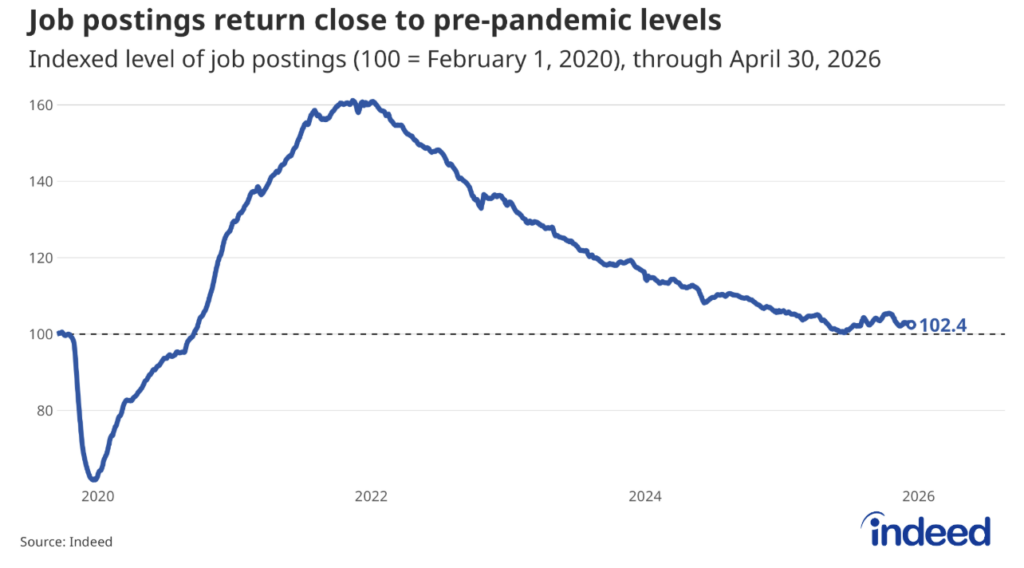

Job Postings

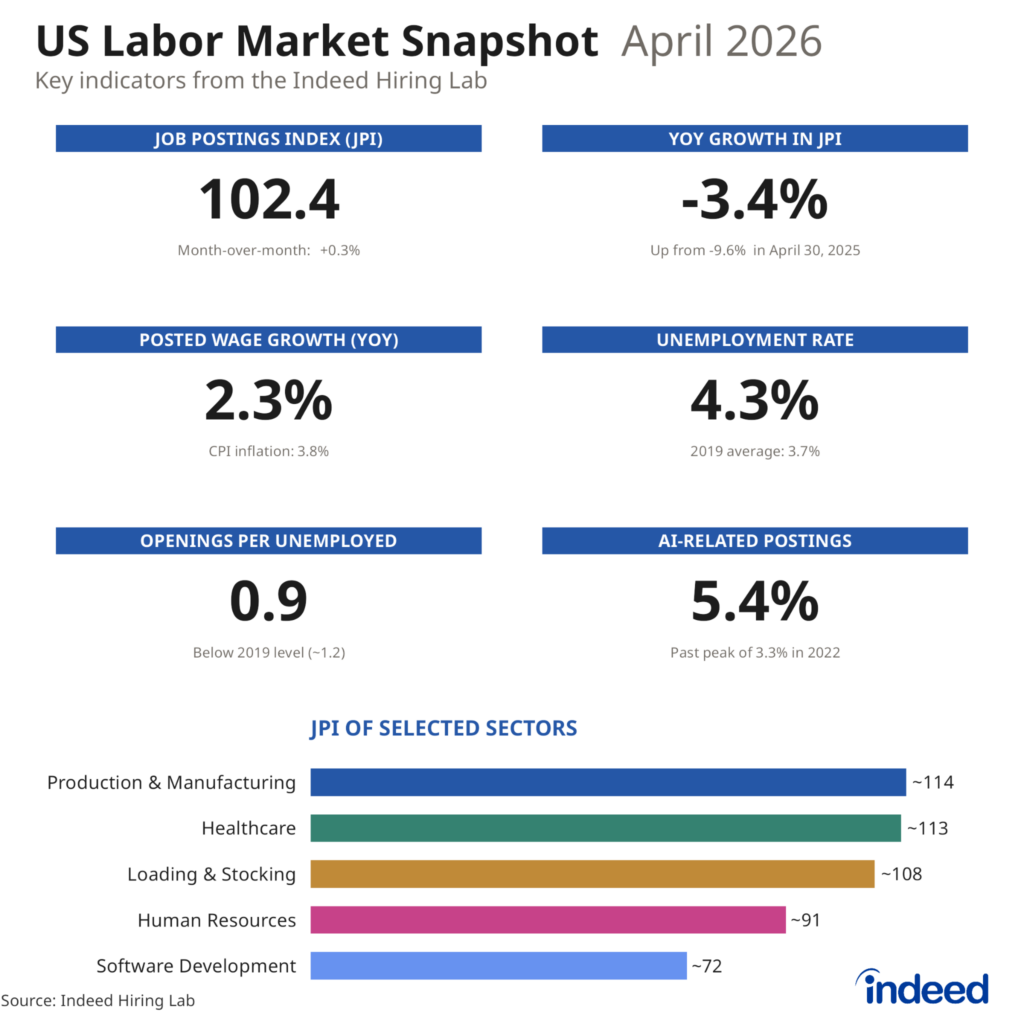

Where we are: Indeed’s JPI stood 2.4% above pre-pandemic levels at 102.4 as of April 30, 2026. This is among the lowest readings of the JPI since spring 2021, though a slight recovery from a trough seen last October.

Direction of travel: While year-over-year readings over the last few months have remained negative, they are continually edging towards zero. As the JPI continues to bump along the bottom, month-over-month values have been a mix of small positive and negative readings.

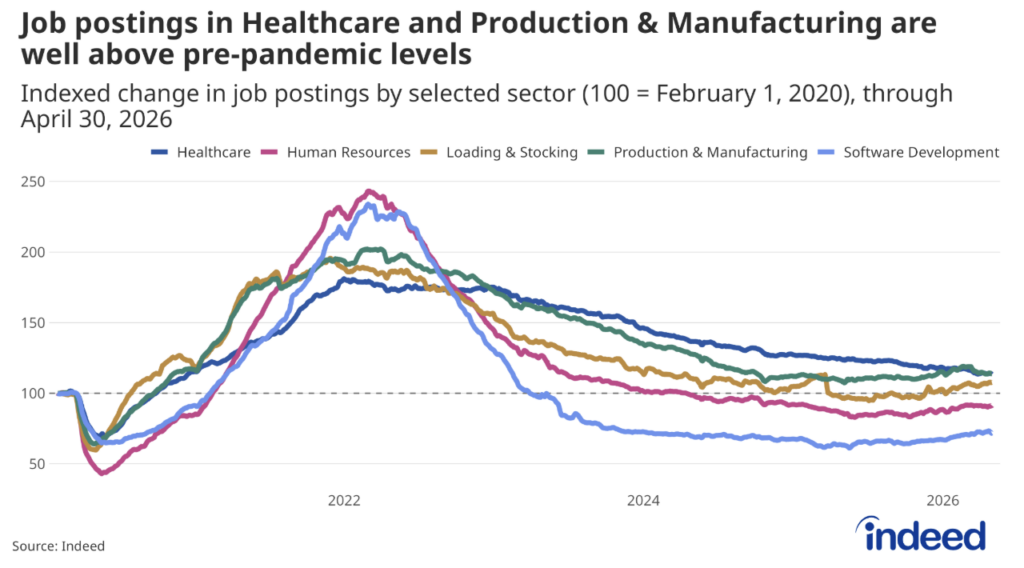

Sector split: Some healthcare postings remain well above their pre-pandemic baseline, even as the nursing sector continues to cool. While software development and IT roles sit roughly 30% below that baseline, software development jobs — especially ones linked to AI —are experiencing a strong pickup in demand, with that sector up 14% on a year-over-year basis as of April 30, 2026. Half of all sectors tracked are now near or above pre-pandemic levels, but the gap between the strongest and weakest is striking.

Wages

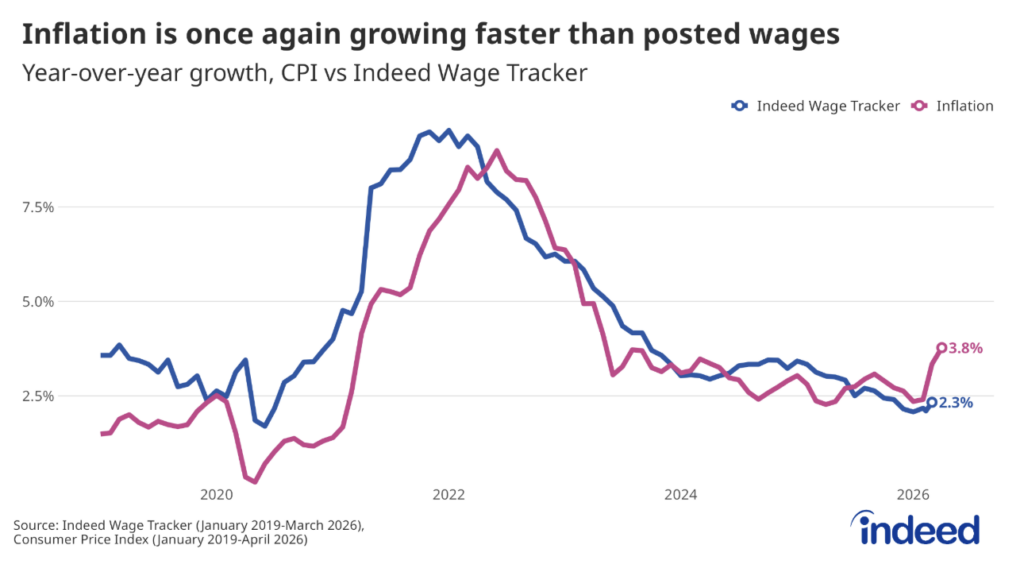

Headline: Posted wage growth has continued to decelerate, with the Indeed Wage Tracker clocking growth at 2.3% on a year-over-year basis as of March 2026. While we no longer see the wages growth decelerating quite as much as it did a few years ago, current growth levels are an outgrowth of a much cooler, less competitive labor market.

Versus inflation: Of note remains the fact that inflation, as measured by the Consumer Price Index, has recently picked up. As inflation runs hotter than wage growth, consumers’ purchasing power will diminish and households’ paychecks won’t carry them quite as far as they used to, potentially impacting consumption.

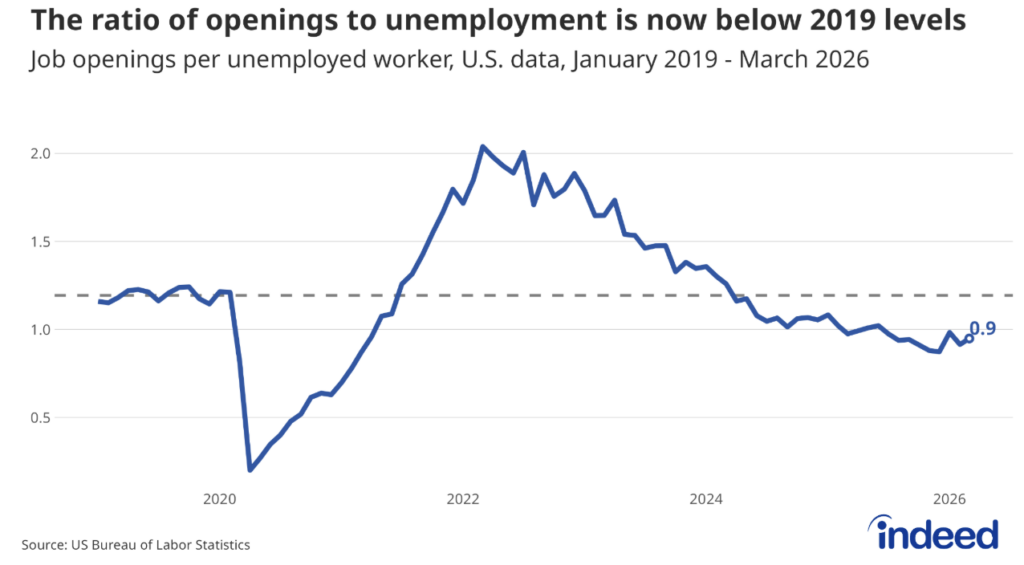

The Labor Market Balance

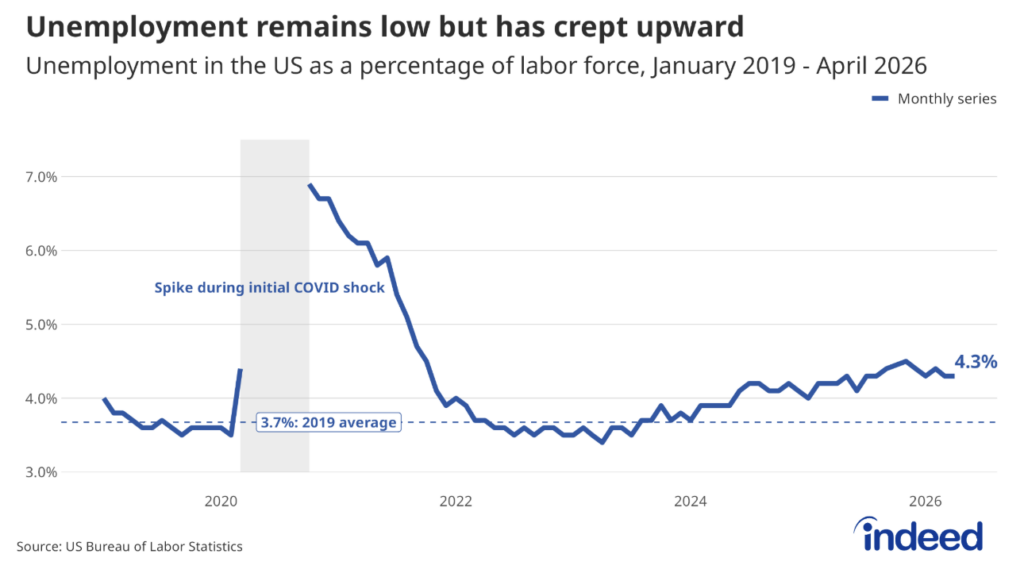

Unemployment: With last Friday’s jobs report, the unemployment rate now stands at 4.3%. While this is still a historically low level, it continues the recent trend of more elevated rates.

Job openings per unemployed worker: The vacancy-to-unemployment ratio has dropped to 0.9, meaning there is less than one available job vacancy per unemployed worker. Similar to slowing wage growth, this ratio is in line with the cooling, less competitive labor market we have been experiencing.

Hires, quits, and layoffs: The quits rate remains subdued at 2.0%, suggesting workers aren’t confident they can find better opportunities elsewhere. Layoffs remain near historic lows, and hires — the recent spike notwithstanding — remain well below the post-pandemic rise, thereby reinforcing the low-hire, low-fire that has defined the labor market for over a year.

What We’re Watching

- Embracing the new normal: The world of work is starting to look different, not just with AI influences but also how the labor market is responding to our aging population and immigration policy.

- AI’s dual edge: Over 5% of job postings now mention AI, and software development job postings are up 14% year-over-year, with over 47% of job postings in the sector mentioning AI. But AI is also driving displacement: the information sector’s layoff rate doubled over the past year to 2.4%, the sharpest increase of any sector, in part driven by AI. We continue to watch the balance between destruction and creation.

- Geopolitical headwinds and inflation: The Iran conflict has pushed CPI to 3.8%, widening the gap with posted wage growth and further squeezing real purchasing power. US postings have dipped modestly since the conflict began, but the knock-on effects — consumer confidence, business investment, and a Fed now even less likely to cut rates — may prove more significant in the months ahead.

The full chartbook with additional sector, wage, and JOLTS detail is available here.

Infographic titled “US Labor Market Snapshot: April 2026” presenting key indicators from the Indeed Hiring Lab. The Job Postings Index (JPI) sits at 102.4, up 0.3% month-over-month but down 3.4% year-over-year (an improvement from -9.6% in April 2025). Posted wage growth has slowed to 2.3% year-over-year, trailing CPI inflation of 3.8%, while the unemployment rate stands at 4.3%, above the 2019 average of 3.7%. Job openings per unemployed worker have fallen to 0.9, below the 2019 level of roughly 1.2, and AI-related postings have climbed to 5.4%, well past their prior peak of 3.3% in 2022. A bar chart of selected sectors shows Production & Manufacturing (~114) and Healthcare (~113) well above the February 2020 baseline, Loading & Stocking (~108) modestly above, and Human Resources (~91) and Software Development (~72) still below pre-pandemic levels.