Key points:

- The latest data from the Indeed Wage Tracker shows posted wages grew at a 4.7% annual rate in July, down from 5.8% in April and 8% last July.

- Posted wages are likely to return to their average pre-pandemic growth rate sometime between October and December if the current pace of deceleration continues.

- With inflation cooling and unemployment remaining low, the Federal Reserve should be encouraged by the concurrent slowdown in posted wages.

Our monthly Labor Market Update looks at an important labor market trend through the lens of Indeed data. A more comprehensive view of the US labor market can be found in our US Labor Market Overview chartbook. Data from our Job Postings Index—which stands 27.4% above its pre-pandemic baseline as of August 18—and the Indeed Wage Tracker are regularly updated and can be downloaded on our data portal and GitHub.

Inflation is retreating, if not yet routed. While it remains above the Federal Reserve’s 2% target, inflation has come down considerably in recent months. But it remains unclear if inflation can continue to fall to its desired level without causing significant damage to a thus far surprisingly resilient labor market. A common argument holds that inflation will only truly come down to acceptable levels if wage growth is pushed down by a significant surge in unemployment. But as Federal Reserve policymakers head to the annual Jackson Hole conference this week, they should be comforted by the fact that wage growth appears to be coming down on its own, without a spike in unemployment.

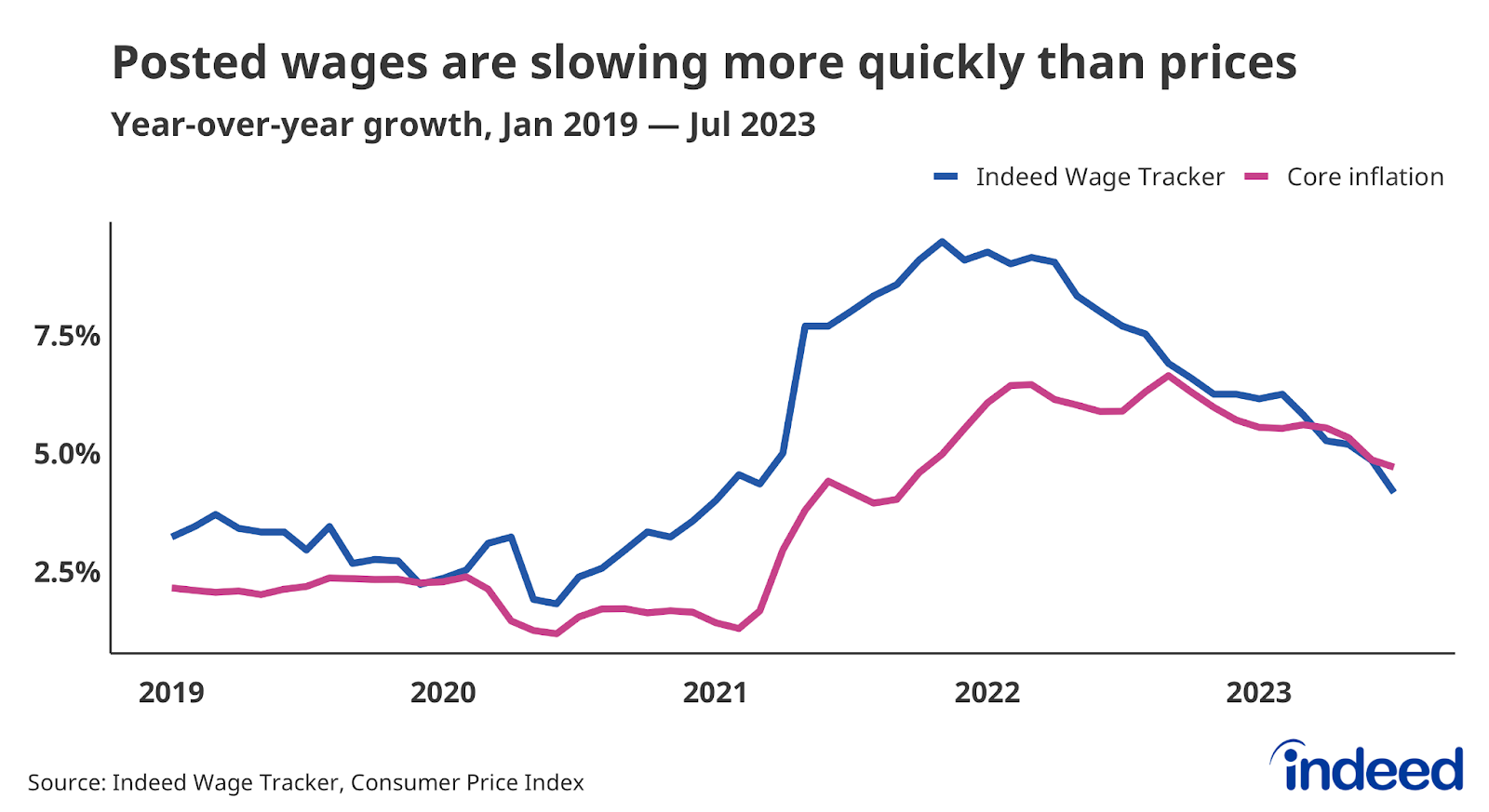

Posted wages grew 4.7% year-over-year in July 2023 on a three-month average basis, according to the latest data from the Indeed Wage Tracker. This number is down from 5.8% as recently as April of this year, and 8% in July 2022. While posted wage growth is still above its 2019 average of 3.1%, it might not remain elevated for much longer. Assuming the current pace of deceleration continues, posted wages will return to their 2019 average growth rate sometime between October and December.

Given the recent trends in inflation, anyone concerned about a “wage-price” spiral should be relieved. The risk of a resilient labor market keeping wage growth (and therefore inflation) elevated is diminishing. Posted wages have grown more quickly than core inflation for the past several years, but wage growth has now slipped below core inflation—a sign at odds with the idea that the labor market will add fuel to the inflationary fire.

Additionally, posted wage growth is a measure of wage growth for new hires, a segment of the labor market that leads the overall labor market. Like the Indeed Wage Tracker, wage measures covering all workers will likely lag a measure. Wage growth might already be on a path back toward levels experienced by employers and workers in 2019, even if this trend is not yet fully reflected in other wage growth measures. Fed policymakers should consider they might not have to take much more action to adequately cool the labor market down.

None of this is to say that the Federal Reserve should immediately declare victory in the fight against inflation. Instead, as the Fed tries to fulfill its dual mandate to keep inflation low and employment high, it should remember that the national labor market is an ally and not an adversary. Slowing wage growth will help. The labor market is cooling in a slow but sustainable fashion, with wage growth slowing and unemployment remaining low.

For more on the current state of the US labor market, including the latest from the Indeed Job Postings Index check out our US Labor Market Overview chartbook.

Methodology

To calculate the average rate of wage growth, we follow an approach similar to the Atlanta Fed US Wage Growth Tracker, but we track jobs, not individuals. We begin by calculating the median posted wage for a given country, month, job title, region, and salary type (hourly, monthly, or annual). Within each country, we then calculate year-on-year wage growth for each job title-region-salary type combination, generating a monthly distribution. Our monthly measure of wage growth for the country is the median of that distribution. Alternative methodologies, such as the regression-based approaches in Marinescu & Wolthoff (2020) and Haefke et al. (2013), produce similar trends. More information about the data and methodology is available in a research paper by Pawel Adrjan and Reamonn Lydon, Wage growth in Europe: evidence from job ads, published in the Central Bank of Ireland’s Economic Letter series.