Key Points:

- The UK labour market continues to show resilience in the face of a bleak economic outlook.

- The ongoing rebalancing of labour demand and supply will continue, with the historically tight labour market likely to loosen only gradually.

- Candidates are likely to retain a degree of leverage over pay and conditions, with flexibility set to remain a powerful tool for job attraction and retention.

- High wage growth has peaked, but its persistence remains key to the outlook for interest rates.

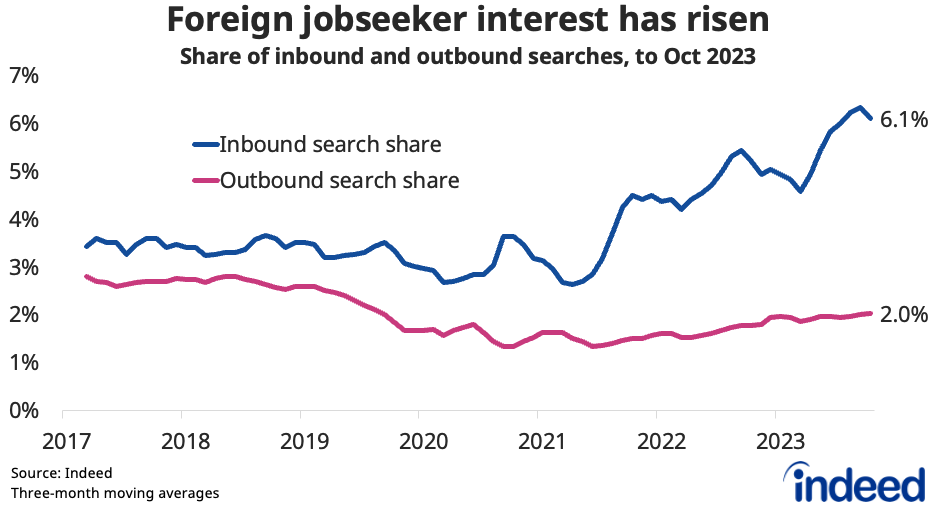

- Foreign interest in UK jobs has doubled in the past two years amid record net migration.

- GenAI will disrupt the job market and has already ignited rapid jobs growth in its creation and use.

The UK labour market was piping hot in 2022 and has spent much of 2023 slowly coming off the boil. And while the market continues to simmer, further cooling is on the cards for 2024, as the UK economy faces a challenging outlook and the fight against inflation remains far from over.

The rebalancing of labour demand and labour supply is ongoing, as vacancies drift down from peaks and labour participation recovers from the pandemic. But it’s still a fairly tight labour market by historic standards, and barring unforeseen shocks seems set to loosen only gradually going forward.

That means hiring conditions are set to remain somewhat challenging, particularly in lower-paid sectors (like hospitality, food, retail and distribution) experiencing persistent staff shortages post-pandemic and post-Brexit. It also means candidates are likely to retain some leverage around pay and conditions.

Amid grim economic outlook, demand for workers likely to soften further

The UK economy has faltered as policymakers have raised interest rates in an effort to get inflation under control. Recession risks remain, and growth forecasts for 2024 and beyond are anaemic. Inflation is well down from its peak, but the cost of living crisis is far from over, and households will continue to feel squeezed heading into a general election year.

The Bank of England (BoE) forecasts zero economic growth in 2024, and the forecast from the Office for Budgetary Responsibility (OBR) isn’t much better at 0.7%. Both organisations expect the economy to have grown by just 0.6% in 2023. Additionally, expansion is forecast to be sluggish in 2025 as well — with growth at 0.4% (BoE) and 1.4% (OBR). Against that backdrop, the labour market is expected to weaken further. Both the BoE and OBR anticipate unemployment rising modestly, from 4.2% currently to approximately 5% by 2025.

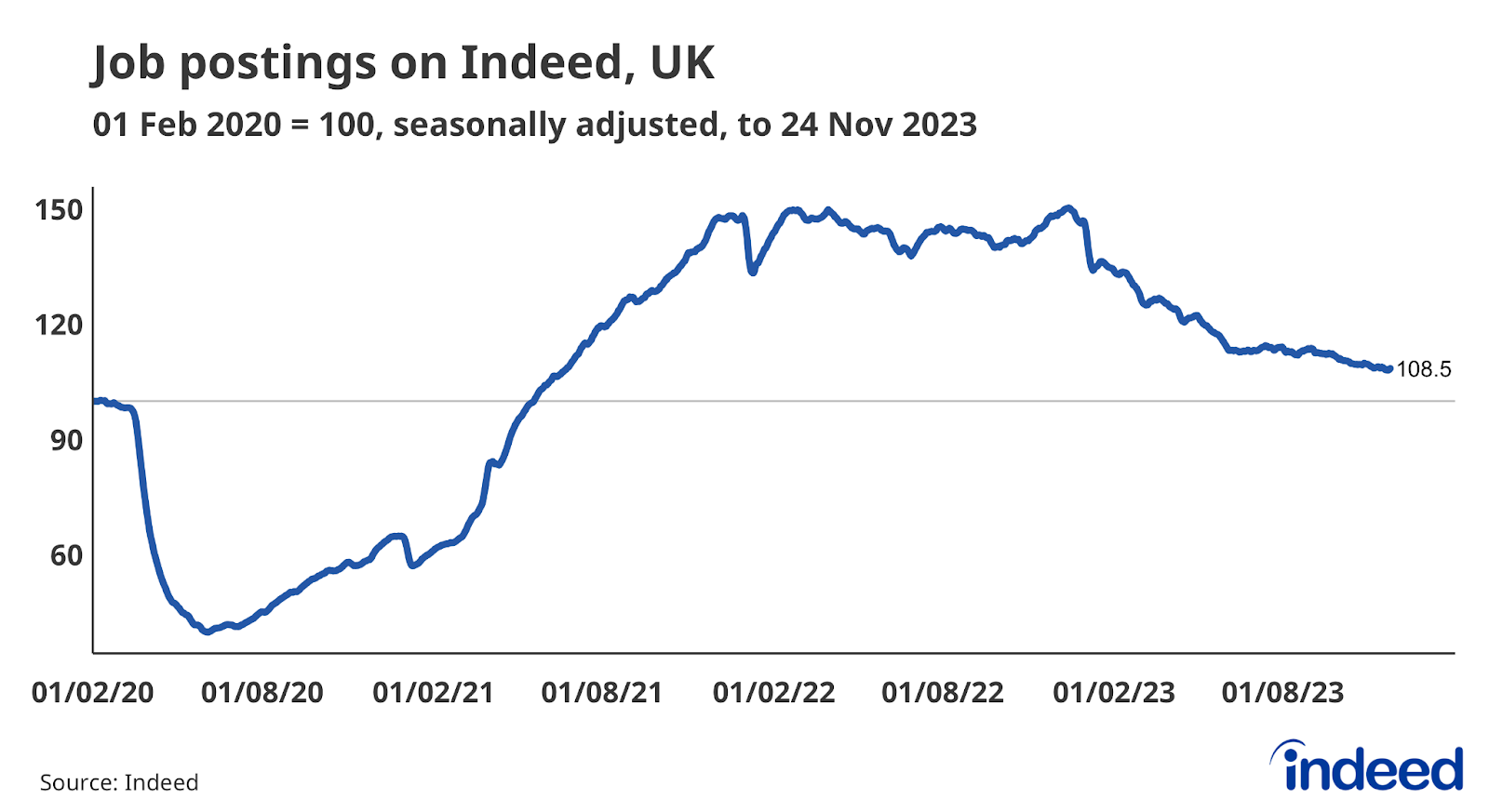

Employer hiring appetite has waned in recent months, though it remains stronger than pre-pandemic. As of 24 November, the Indeed Job Postings Index is down 28% from its December 2022 peak but is still 9% above its 1 February 2020, pre-pandemic baseline.

Office for National Statistics (ONS) data as of October show vacancies down 26% from their peak. However, because of a divergence in official measures of employment, it is unclear how much total employment has grown recently. Alternative indicators point to either flat or substantial growth in total employment over at least the past year.

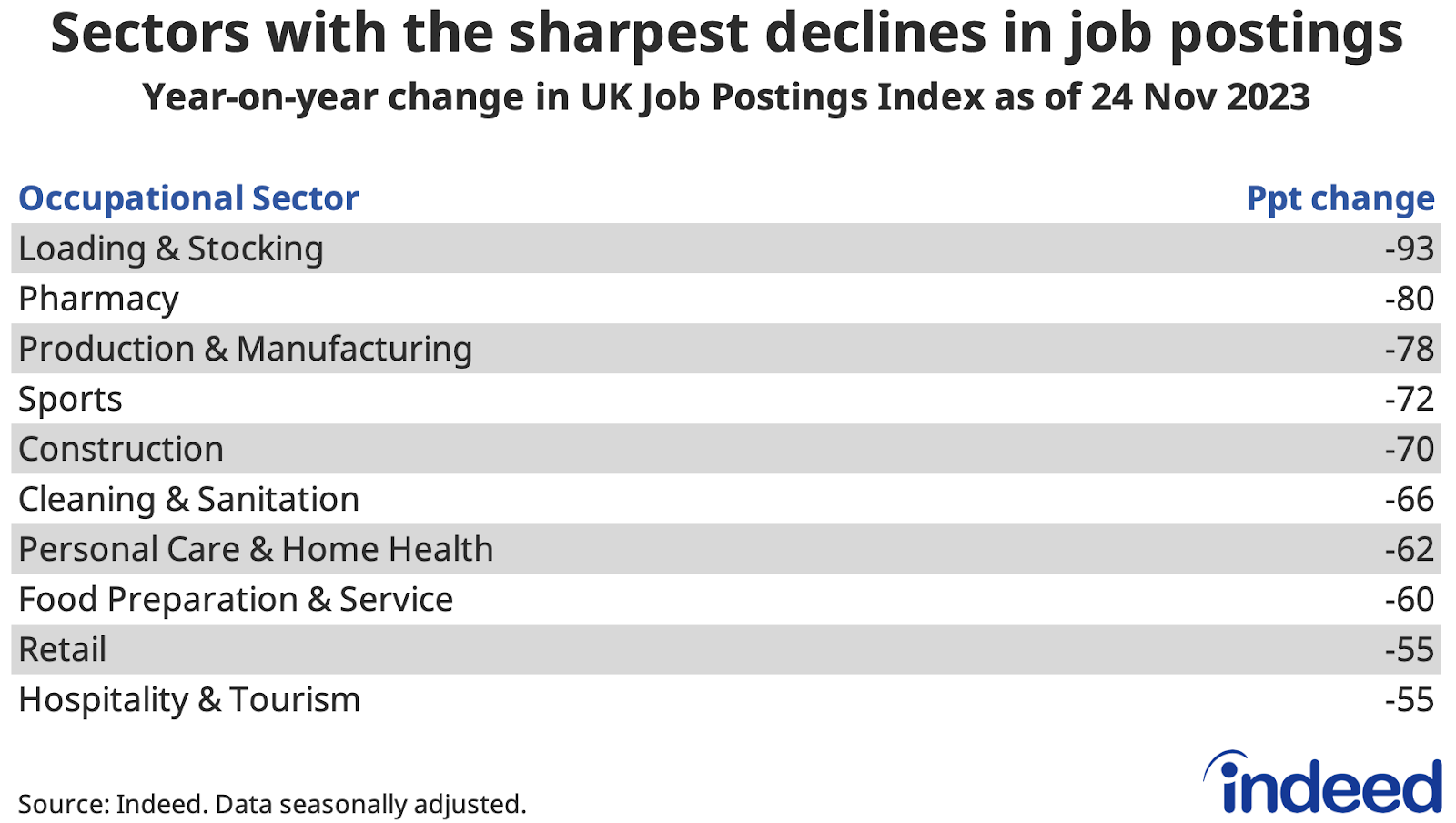

Many of the occupations with the largest year-on-year declines in job postings are associated with sectors reliant on under-pressure consumer discretionary expenditure, including production, retail, distribution and consumer services. Construction, meanwhile, has been hit by a housing market slowdown as interest rates have risen.

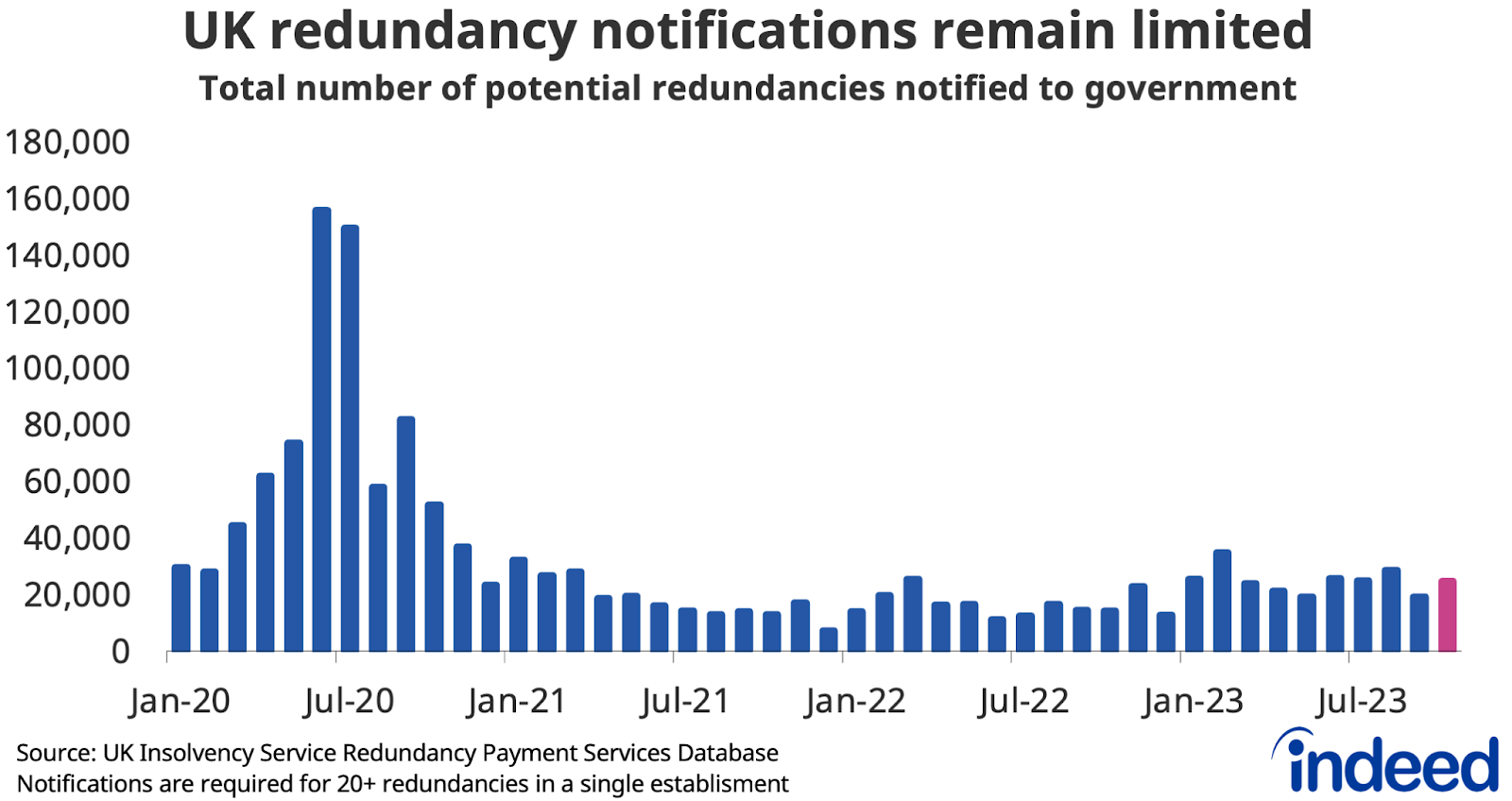

While the labour market has been showing clear signs of softening, with intentions to hire additional workers muted, employer intentions to shed their existing staff have remained limited. That may be partly because employers are mindful of how challenging hiring has been in the past few years, and would prefer to retain staff through what they hope may be a short-lived economic soft patch, leaving them better positioned to come through strongly on the other side.

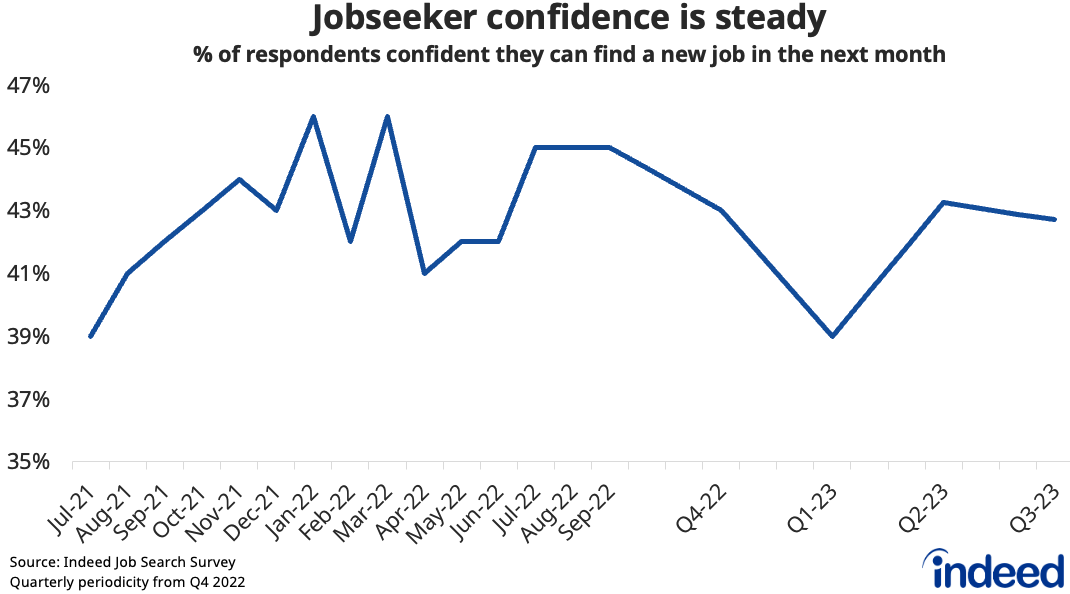

And despite some challenges, jobseekers remain reasonably confident in their ability to find a new position. Around 43% of survey respondents who were actively looking for a new job in September were confident they could find one in the next month, with sentiment having recovered after a dip at the beginning of the year.

Hiring conditions may ease, but only gradually

Concerns around the quality of official labour market data mean it’s hard to get an accurate read on how tight the labour market currently is. The number of unemployed and inactive workers is estimated from the ONS’ Labour Force Survey, which has been plagued by declining response rates. The figures show unemployment was 4.2% in the third quarter, up from 3.5% just over a year ago. This translates to a ratio of 1.4 unemployed persons per vacancy, up from 0.9 just under a year ago.

One factor supporting an increase in labour supply is immigration. New figures show net migration in 2022 was even stronger than initially thought at a record 745,000 new arrivals. In the year to June 2023, net migration remained high at 672,000. The figures reflect high arrivals from Hong Kong and Ukraine under humanitarian routes, though there has also been a large influx of students and people arriving with work visas to fill shortages in the healthcare system.

Foreign jobseeker interest in UK jobs has rebounded strongly from the pandemic. More than 1-in-20 (6.1%) UK job searches in the three months to October came from jobseekers located abroad, up from 4.5% in the same period in 2021. High foreign interest, combined with low outbound searches from UK workers looking at international opportunities, suggests that net migration will continue to be supported by inflows of people looking to work in the UK.

The Chancellor’s Autumn Statement featured a tightening of welfare to try and boost workforce participation among the long-term jobless, which the OBR estimates would increase employment by about 50,000 over the next five years. Meanwhile, cuts to National Insurance rates (social security contributions) are expected to raise employment by 28,000 over the same period, and increase total hours worked to the equivalent of 94,000 full-time workers.

But amid record NHS waiting lists, and with the number of people inactive due to long-term sickness standing at a record 2.6 million, the overall size of the workforce looks likely to remain constrained for some time.

Wage growth has probably peaked, but could prove stubborn

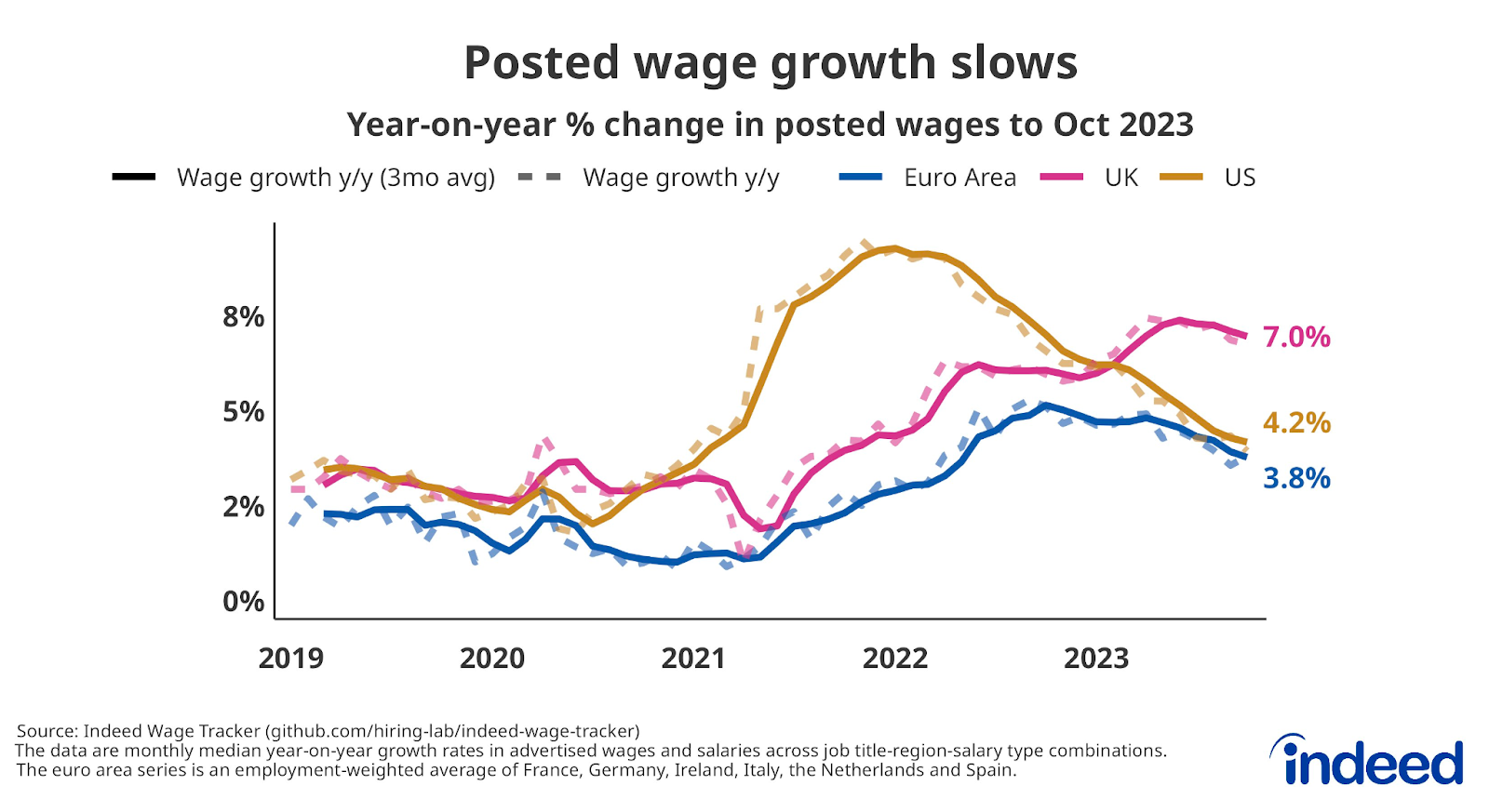

The annual pace of wage growth will be a key factor in helping the BoE determine if more interest rate hikes will be needed next year to tame inflation and cool demand. The Bank of England has said it expects wage growth to prove somewhat sticky, while “second-round effects in both domestic prices and wages are expected to take longer to unwind than they did to emerge”. The Bank expects private sector wage growth (currently running at 7.7% year-on-year) to ease in 2024 amid a looser labour market, but still be at a brisk 5% by end-2024.

The Indeed Wage Tracker shows posted wage growth dipped to 7.0% year-on-year in October, down from 7.4% in June. But the UK continues to see much stronger wage growth pressures than the US and euro area, underscoring the continued need for Bank of England vigilance.

The lowest-paid workers will again see a significant uplift in their wages next year, after the Chancellor announced a record 9.8% increase in the statutory minimum wage, to £11.44 an hour, effective from April 2024. That follows a 9.7% increase in April 2023.

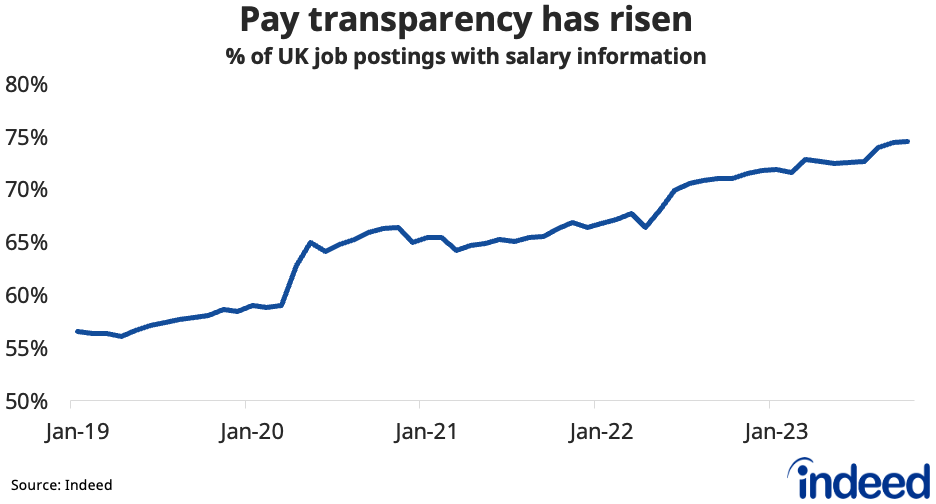

For jobseekers looking to obtain a pay rise, the good news is that a high and rising proportion of UK job postings include salary information (almost three-quarters of postings included pay information as of October). Wages may not rise as fast next year as they have this year, but in a still-tight labour market, employers may find it necessary to advertise what they are paying to attract talent ahead of their competition.

Flexibility will remain a focus despite return-to-office calls

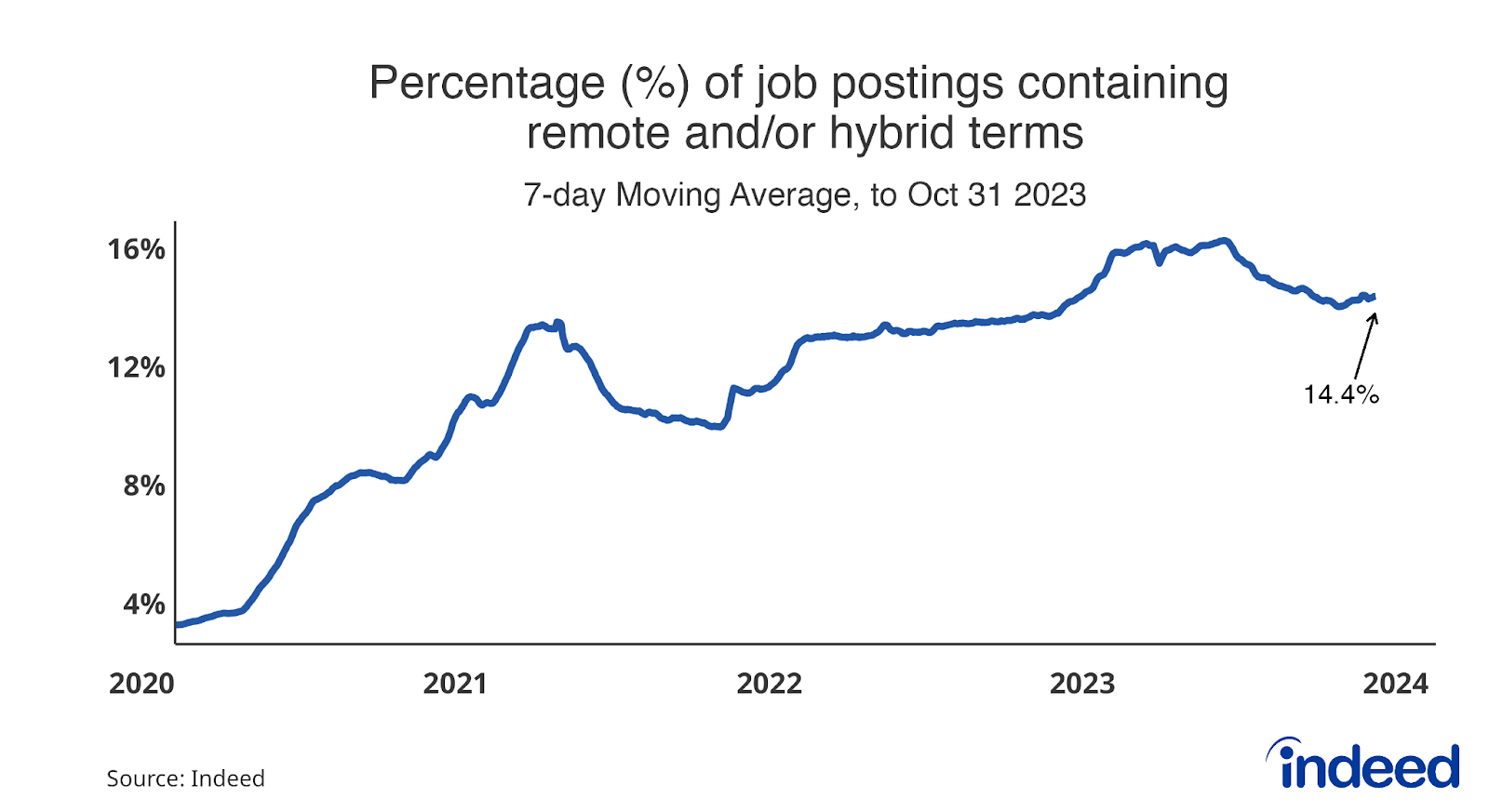

The prevailing post-pandemic job market has been a candidate-led one, but the ongoing softening of labour demand spells a shift in the balance of power towards employers. There are already signs of employers becoming less inclined to accede to the preferences of workers. Hybrid working is one example, with many companies having made return-to-office (RTO) mandates over the past year, and some surveys even suggest a majority of bosses think workers will return to the office five days a week.

The share of UK job postings mentioning remote or hybrid terms has dipped from 16.3% in early May to 14.4%, as of the end of October, but remains over three times higher than before the pandemic. Changes in the categories with the highest remote/hybrid postings shares are mixed: Tech occupations have seen falls in remote/hybrid postings shares over the past six months, whereas banking & finance, insurance and legal have seen increases, despite some high-profile RTO calls by prominent firms in those sectors.

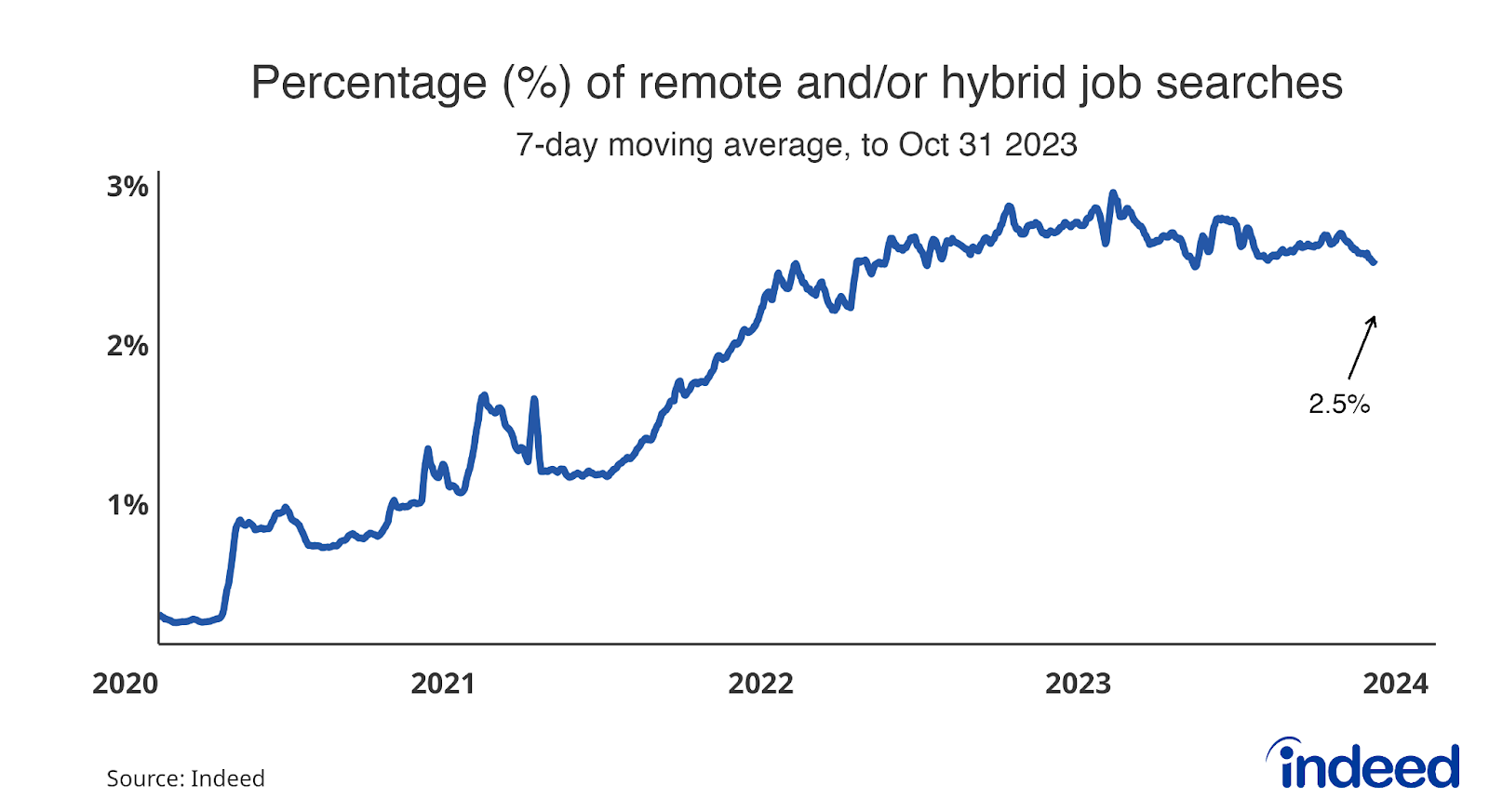

Jobseeker interest in remote and hybrid work remains high (albeit down slightly to 2.5% in October, from 2.9% in early 2023), having risen tenfold from pre-pandemic levels. Offering location flexibility will remain a powerful attraction and retention tool, particularly for smaller companies looking to compete for top talent with larger competitors.

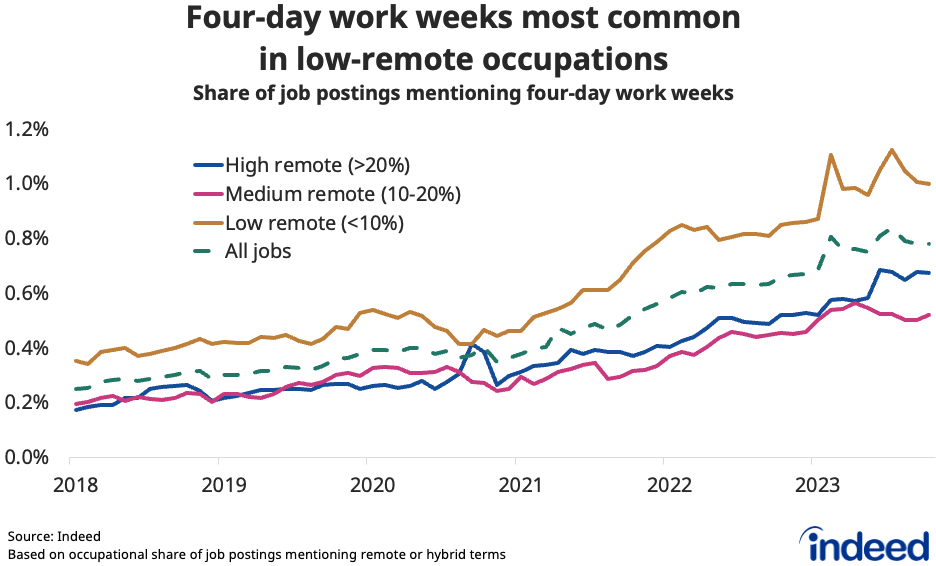

Of course, many jobs can’t be done remotely. But employers looking to recruit for in-person roles can still offer other forms of flexibility — around hours and shift patterns, for example. Another trend is that of offering four-day work weeks. The share of job postings mentioning four-day work week arrangements has been rising, though at 0.8%, remains a niche phenomenon. The share is highest (1%) among the least remote-friendly occupations (those with less than 10% of postings offering remote or hybrid), versus 0.7% for high-remote and 0.5% for medium-remote occupations. Categories most likely to offer four-day weeks include healthcare, childcare, manufacturing and food service.

GenAI is already creating as well as disrupting jobs

Generative artificial intelligence (GenAI) is increasingly shaping the labour market landscape. Virtually every job will face some level of exposure to potential GenAI-driven change. But while GenAI can learn to do some tasks reasonably well, it is unlikely to fully replace many jobs — especially those that require manual skills and/or deep personal connections.

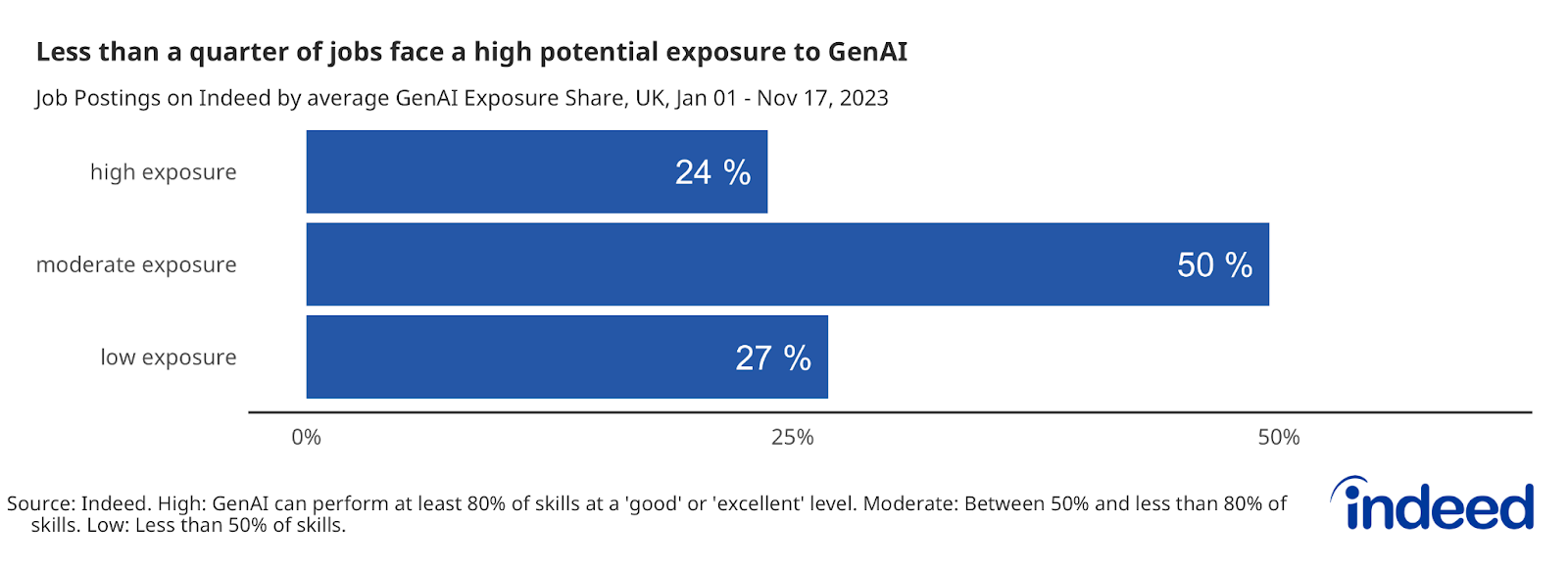

An analysis of UK job postings data indicates that 24% of jobs face the highest level of potential exposure (GenAI can perform 80% or more of the skills in these jobs reasonably well), whereas 27% face the lowest potential exposure (GenAI can perform less than half of the skills in these jobs reasonably well). As the technology continues to learn skills associated with certain jobs, it will augment or transform some more than others.

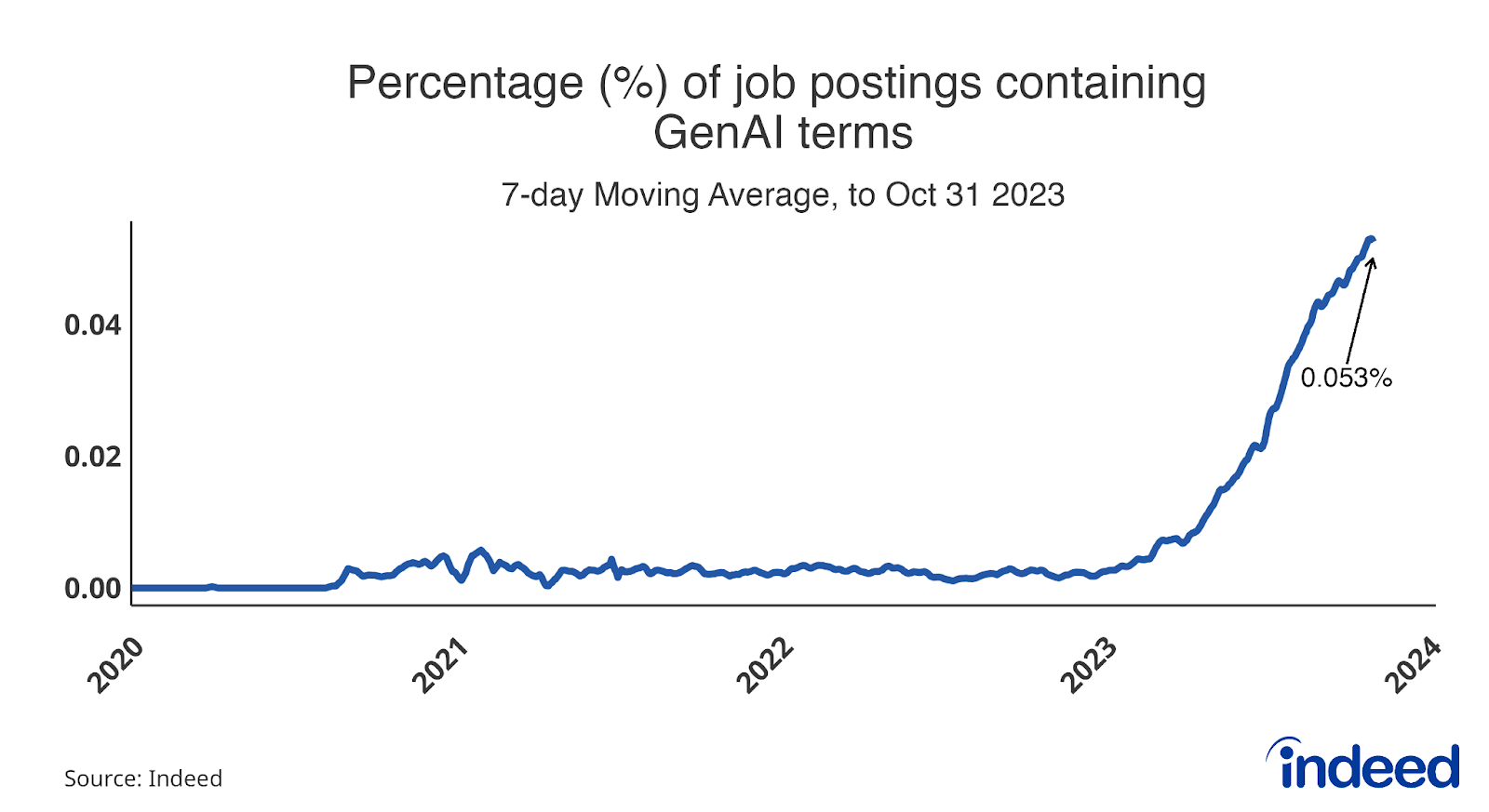

Meanwhile, jobs related to the creation and use of GenAI tools are surging, albeit from a very low base. As of the end of October, the share of UK job postings mentioning terms related to Generative AI stood at 0.05%, a twenty-six-fold increase since the start of the year. Though only 5 in 10,000 job postings means GenAI jobs aren’t yet common, we’re likely to see continued rapid growth in 2024 and beyond, as organisations integrate these tools into their businesses.

The growing utilisation of GenAI and other technologies, along with the rising demand for jobs involved in their development, has the potential to reshape the broader landscape of the labour market. While there is anticipated growth in GenAI-related positions in the coming years, it is crucial to consider whether this expansion is primarily driven by the creation of these tools, or if there is a corresponding increase in roles that actively utilise these tools. If the latter is lacking, the economic impact of AI and GenAI may be limited. Therefore, as we navigate the future of GenAI jobs, we’ll be monitoring both the overall quantity, and the leading occupational sectors contributing to this evolution.

Conclusion

The UK economy enters 2024 facing strong headwinds. But the labour market continues to show resilience, and the imbalance of labour demand and supply is only gradually easing. The path to a soft landing remains open, but there is still a long way to go and recession risks loom. Potential setbacks, including inflationary pressures proving stickier than expected, could yet force the Bank of England to press harder on the brakes, and lead to a sharper slowdown than we’ve seen to date. For now, the robustness of the labour market remains a rare economic bright spot as we head towards a general election year in which the economy’s fortunes will be under even heavier scrutiny than usual.

Methodology

Data on seasonally adjusted Indeed job postings are an index of the number of seasonally adjusted job postings on a given day, using a seven-day trailing average. February 1, 2020, is our pre-pandemic baseline, so the index is set to 100 on that day. We seasonally adjust each series based on historical patterns in 2017, 2018, and 2019. We adopted this methodology in January 2021. Data for several dates in 2021 and 2022 are missing and were interpolated. Non-seasonally adjusted data are calculated in a similar manner except that the data are not adjusted to historical patterns.

The number of job postings on Indeed.com, whether related to paid or unpaid job solicitations, is not indicative of potential revenue or earnings of Indeed, which comprises a significant percentage of the HR Technology segment of its parent company, Recruit Holdings Co., Ltd. Job posting numbers are provided for information purposes only and should not be viewed as an indicator of the performance of Indeed or Recruit. Please refer to the Recruit Holdings investor relations website and regulatory filings in Japan for more detailed information on revenue generation by Recruit’s HR Technology segment.

To calculate the average rate of wage growth, we follow an approach similar to the Atlanta Fed US Wage Growth Tracker, but we track jobs, not individuals. We begin by calculating the median posted wage for each country, month, job title, region and salary type (hourly, monthly or annual). Within each country, we then calculate year-on-year wage growth for each job title-region-salary type combination, generating a monthly distribution. Our monthly measure of wage growth for the country is the median of that distribution.

GenAI exposure shares were based on analysis of skills mentioned in job postings. Jobs in which 80% or more skills can be done “good” or “excellent” by GenAI were determined to have the highest potential exposure to GenAI-driven change. Jobs in which between 50% and less than 80% of skills can be performed good or excellent were determined to have a moderate potential exposure to GenAI. Jobs in which less than half of skills could be done good or excellent were determined to have a low potential for exposure. For more information on methodology see here.

The analysis of Generative AI job postings involved extracting job postings directly related to Generative AI, using specific keywords indicating its presence, such as “Generative AI,” “Large Language Models,” and “Chat GPT.”

We assess foreign job seeker interest in the UK by tracking the share of total searches on Indeed in the UK by job seekers with IP addresses outside of the UK. Job seekers whose location could not be determined were removed from the analysis.

We calculate pay transparency share in UK job postings by dividing the number of unique job postings with a salary into a total count of unique advertisements in a given month. Pay information is extracted from postings published on Indeed.com. Salaries advertised as being paid daily or weekly are omitted from the analysis.