Key Points:

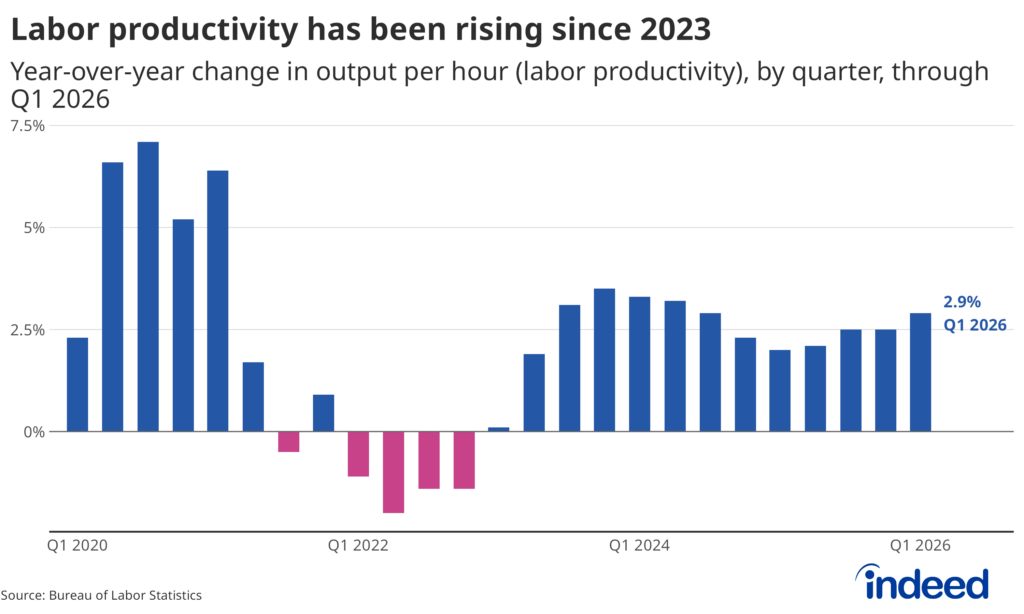

- Nonfarm business sector labor productivity increased by 2.9% year-on-year in Q1 2026, according to preliminary estimates from the Bureau of Labor Statistics. Output increased 1.5%, and hours worked increased 0.7%.

- Real hourly compensation increased by 1.4% overall year-on-year, but fell 0.5% from last quarter.

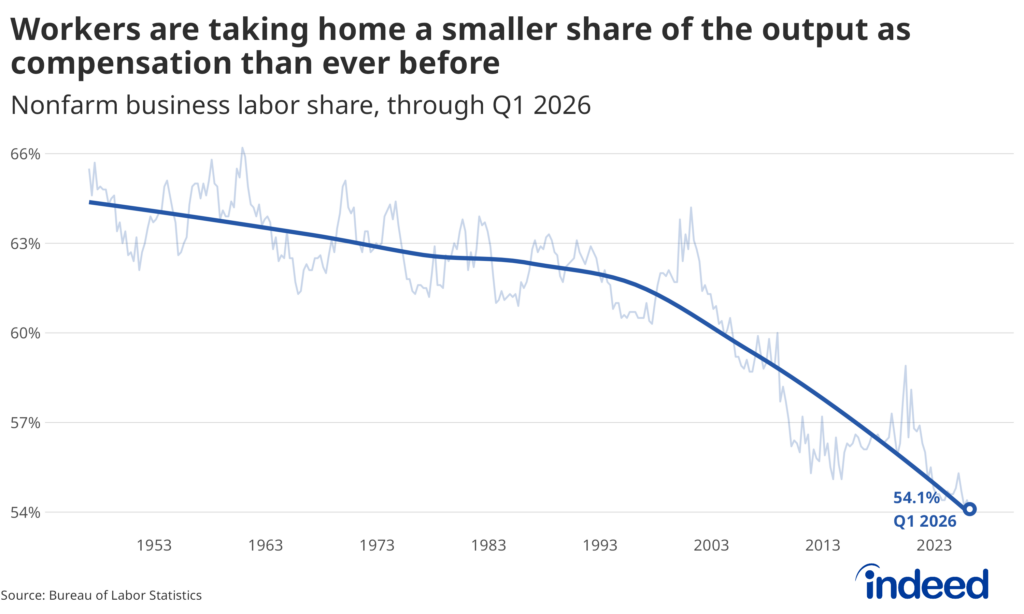

- Labor share dropped to 54.1%, the lowest since the metric was first measured in 1947.

The ongoing reversal of the immediate post-pandemic productivity slump continued in Q1, with US nonfarm business productivity rising 2.9% year-over-year. Consistent productivity growth in recent years is a sign of an economy that has settled onto a steady, if unspectacular, growth path following a decline in output per hour worked driven by the 2022-era surge in hiring. The more recent rise in productivity also coincides with rapidly rising investment in AI, which is showing signs of making workers more productive, but may also be pushing the returns from these productivity gains away from workers and towards investors and business owners, as labor share declined to its lowest recorded level. So far, many of these gains in productivity have come even as hiring has been muted, with employers squeezing more from their existing workforces rather than expanding. But there are limits to that squeeze, and if/when there is no more slack left to pull on in the market, this recent productivity boom may end up stalling out.

While productivity is rising, workers are capturing a smaller slice of the spoils than at any point in modern history. Just 54.1% of all output was paid back to workers as compensation, the lowest share ever recorded. Productivity is rising and output is growing, but the benefits are increasingly flowing to business owners and investors instead of workers.

To add on to that, average weekly hours for private-sector workers have barely moved, holding around 34 hours over the past 3 years. Same hours, but more output is an indication of the utilization squeeze at work. So, workers are simultaneously getting an increasingly lower share of the output as wages, while producing more per hour. Which raises an important question: once that squeeze runs its course and there’s no more slack to extract, how much of the current productivity trend actually holds?

Notably, a recent BLS analysis found that software investment grew 11.1% annually between 2019 and 2024, the fastest of any asset category by a wide margin. BLS refers to this software investment measure as a proxy for AI adoption, meaning the surge in that category is a signal of how quickly businesses are embedding AI into their production processes.

Those investments may be starting to show up in the labor productivity numbers: workers producing more per hour is exactly what you’d expect as AI tools get embedded across business functions. But total factor productivity, a measure that seeks to isolate genuine efficiency gains and gauge whether output is growing beyond what the level of investment alone would predict, actually decelerated in 2025, from 1.5% to 0.8%. That means efficiency gains on their own did not contribute to labor productivity growth in 2025 as much as in 2024. Instead, capital spending – including on AI – did. Put simply, companies are betting heavily on AI, and AI is contributing to productivity growth through this capital spending, but not yet through efficiency.