Key points:

- Job openings remained unchanged at 6.9 million in March after February openings were revised up, according to the US Bureau of Labor Statistics.

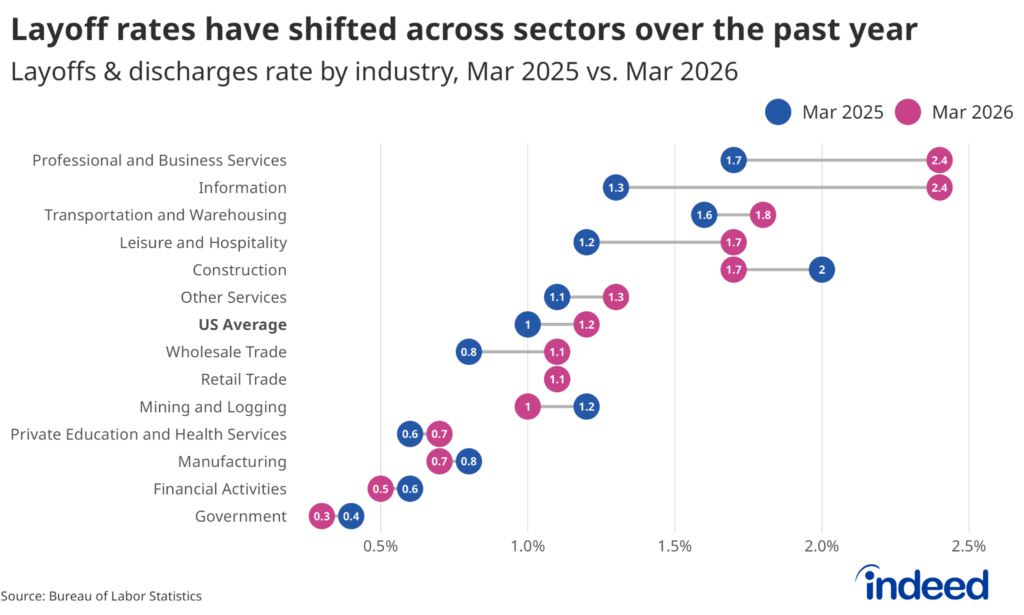

- Layoff rate increased slightly to 1.2% from 1.1%.

- The quits rate moved up slightly to 2%.

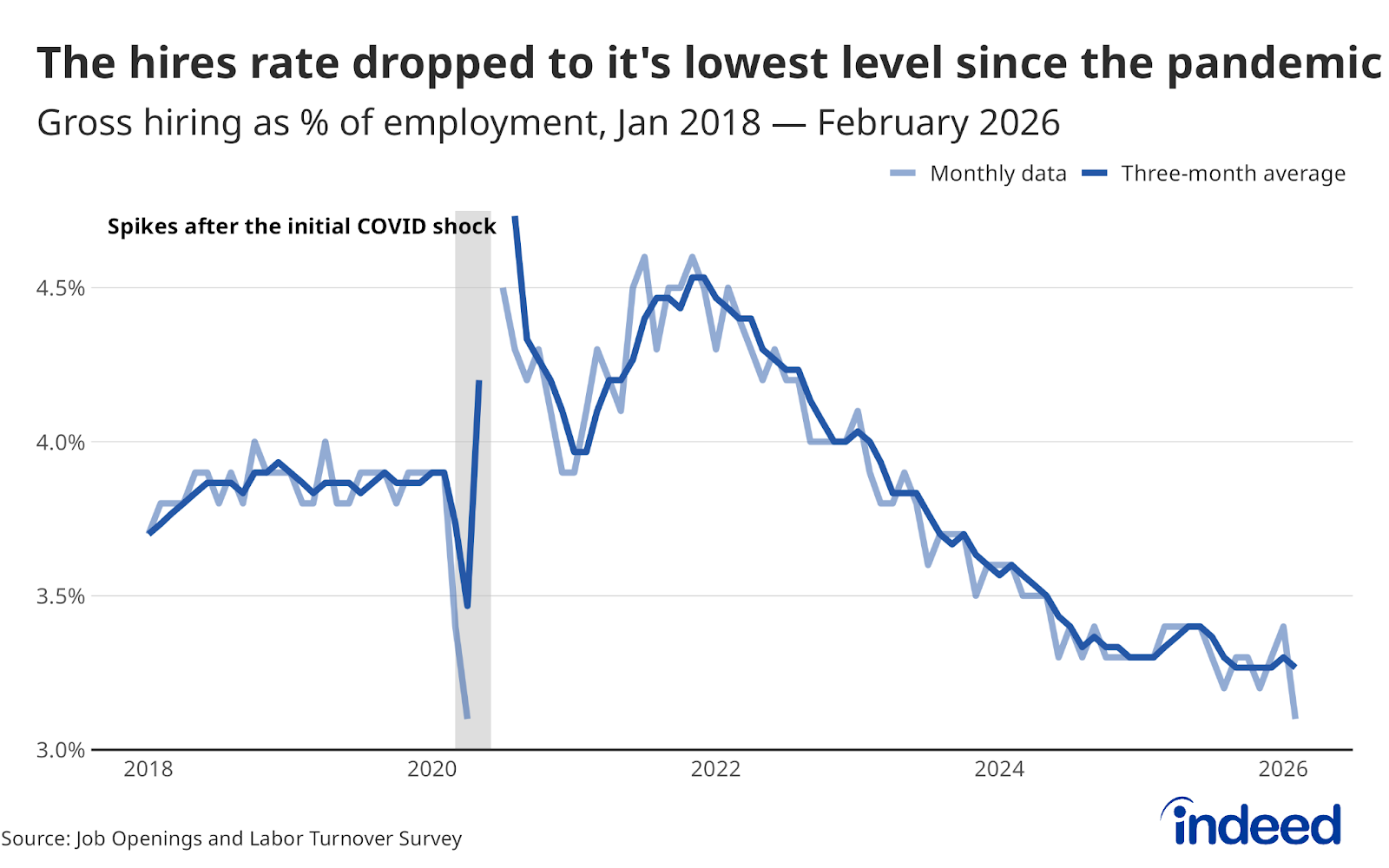

- The hires rate increased to 3.5% in March 2026.

Today’s JOLTS data shows the labor market largely held steady in March, despite intensifying conflict in the Middle East and the ongoing drumbeat of AI disruption, with openings flat from last month and the low-hire/low-fire dynamic broadly continuing for another month. But the headline stability might be somewhat deceptive, and masks some interesting trends that will bear watching going forward. A slight uptick in hires, quits, and layoffs may signal more dynamism beginning to return to the market after years of limited turnover. And while the headline numbers were largely steady, underlying data show the market’s broad resilience is far from uniform, highlighted by a worrisome rise in layoffs in the tech sector that could indicate further AI disruption to come.

The low-hire, low-fire dynamic that has defined this market for over a year didn’t change much in March, but showed some early potential signs of movement. The hires rate increased to 3.5% while the quits rate rose marginally to 2%, where it spent much of the past year. At 1.2%, layoffs remain low overall, but the headline number tells a deceptively calm story. Which sectors are seeing cuts matters just as much, and the industry breakdown reveals why some job seekers may feel particularly unsettled, especially those in white-collar fields.

The layoff rate in the information sector, which includes many tech jobs, rose from 1.3% to 2.4% over the past year, the largest increase of any sector and nearly five times the US average. Professional and business services and leisure & hospitality followed, climbing by 0.7 and 0.5 percentage points respectively. Meanwhile, private education and health services, construction, government, and financial activities saw their layoff rates hold steady or decline.

Recent layoffs announcements, especially in the technology sector, have explicitly cited AI as a driver. As firms ramp up investment in AI, the key thing to look out for is whether and how quickly new roles are created that offset those losses. Either way, these layoff announcements are still working their way through the data, meaning March may be foreshadowing what April and May will confirm.

The job openings data reinforce the same divide. Information job openings were down -33% year-over-year, the steepest decline of any private sector, followed by other services (-21%) and professional & business services (-20%). The Indeed Job Postings Index, which tracks job openings closer to real time than JOLTS, tells the same story. Tech-adjacent sectors remain among those with the largest declines in job postings levels relative to pre-pandemic levels. For example, IT infrastructure, operations, and support have around 30% fewer roles than before the pandemic.

Government job openings are down 13% year-over-year, driven largely by a 41% drop in the number of federal openings since last March – a time that coincides with DOGE’s efforts to cut government headcount. On the other end, retail trade openings grew 58% year-over-year, and manufacturing was up 18%. These highlight segregated labor markets that barely resemble each other.

Put simply, a software engineer, a construction worker, and a retail trader looking at the same headline job opening numbers or hires rate are experiencing fundamentally different realities as job seekers. Stability, in this market, is less a general condition and more a matter of where you are standing.