Key points:

- The FOMC voted today to hold its target federal funds rate at 3.5% to 3.75%. The decision to hold comes as the war in Iran continues to drive up energy prices and slow hiring limits job growth. An extended conflict risks the continued buildup of this stagflationary pressure.

- The meeting marked the likely end of Jerome Powell’s tenure as Fed Chair as the US Senate aims to confirm Kevin Warsh to the position before the next Fed meeting in June. Warsh’s proposals to limit forward guidance and prioritize new data sources are likely to change the way the Central Bank communicates with the public.

The FOMC voted to keep its target federal funds rate unchanged for a third straight meeting today, in line with market expectations. The decision came amid pressure on both sides of the Fed’s dual mandate, as the war in Iran upends energy markets while long-term unemployment continues to grow. The challenging backdrop for policymakers is reflected in the four dissents to today’s policy action — the most in any meeting since October 1992. With one Governor preferring to lower rates, and three other voting members signaling that the next interest rate move may well be up rather than down, the lack of unity among the committee may foreshadow sharper divisions ahead.

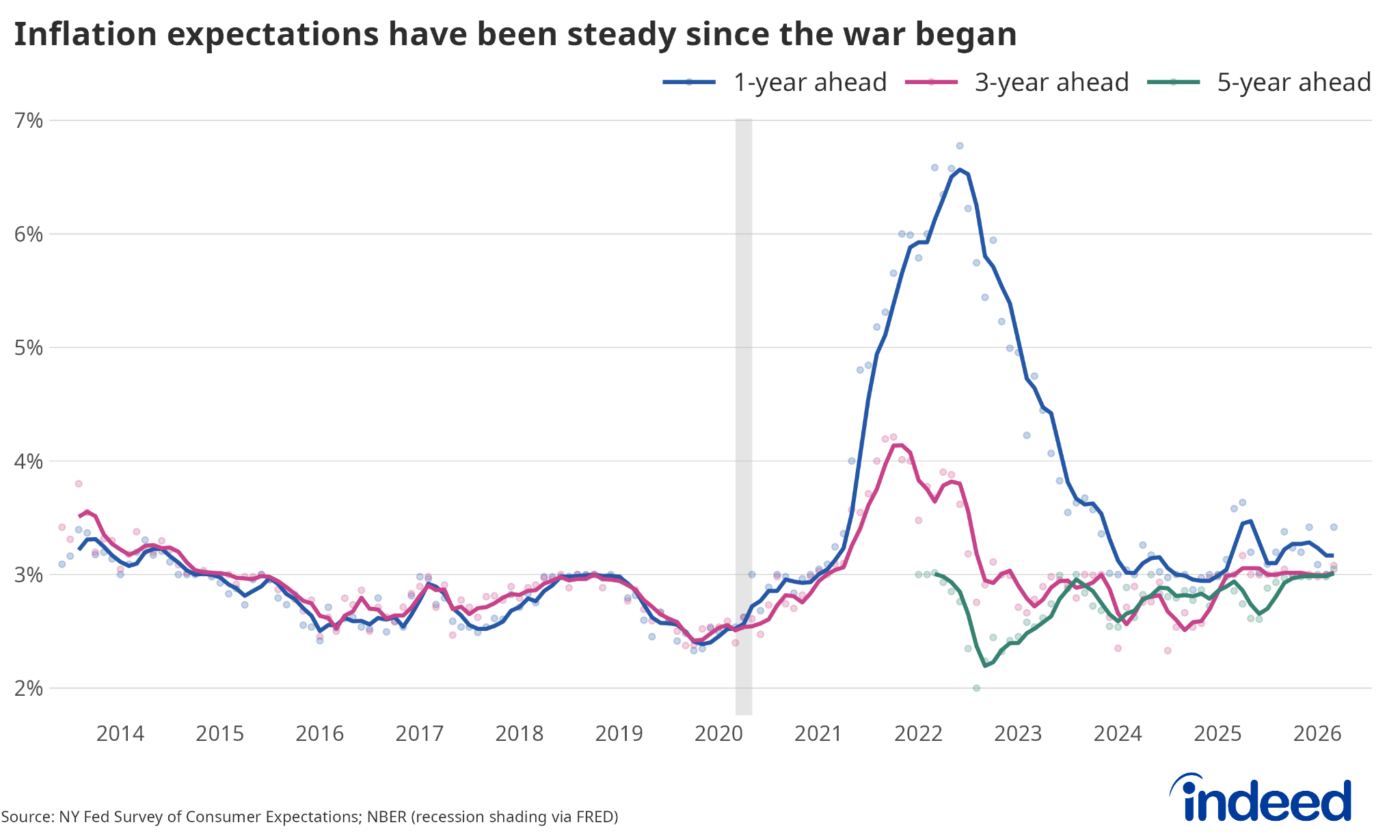

Headline inflation jumped to 3.3% year-over-year in March, driven in large part by a 21% spike in gas prices from February. While the Fed generally aims to weather this type of short-term supply disruption and allow the economy to unwind itself, an extended conflict could force its hand if expected price increases become entrenched. So far, expectations have held up well. According to the Federal Reserve Bank of New York, median 3-year-ahead and 5-year-ahead consumer inflation expectations showed little change in March, and the rise in 1-year-ahead expectations was relatively small. But that could change quickly. Over the coming months, the Fed will likely watch long-term inflation expectations as closely as it does inflation itself, if not more so.

As for the labor market, the surprising strength of last month’s jobs report likely allowed the Committee to feel comfortable staying in wait-and-see mode for now. But cracks are still showing. Long-term unemployment has steadily grown since the pandemic, and the strong March reading could not fully offset weaker reports from earlier in the year. While still unlikely, the possibility is growing that stagflationary pressures — stubbornly high inflation coupled with weak economic and labor market growth — could eventually force the Fed to hike rates into a slowing labor market.

The path forward is also complicated by impending leadership changes at the Fed upon the expiration of Jerome Powell’s second term as chair in May. The confirmation of Kevin Warsh to replace Powell looks likely to wrap up in the next few weeks. Warsh has publicly indicated openness to cutting rates soon, and his first opportunity to shift towards that policy could come as early as June. Barring a meaningful shift in the labor market data or in the Middle East situation, it would be surprising if Warsh were able to foster consensus in the 12-person committee to resume easing in his first month. That said, his first meeting will serve as a meaningful signal on how to read the Fed in a post-Powell world. Warsh’s proposals to curtail some forward guidance and change which data the Fed prioritizes in its economic analyses would be material shifts in how monetary policy operates.