Key points

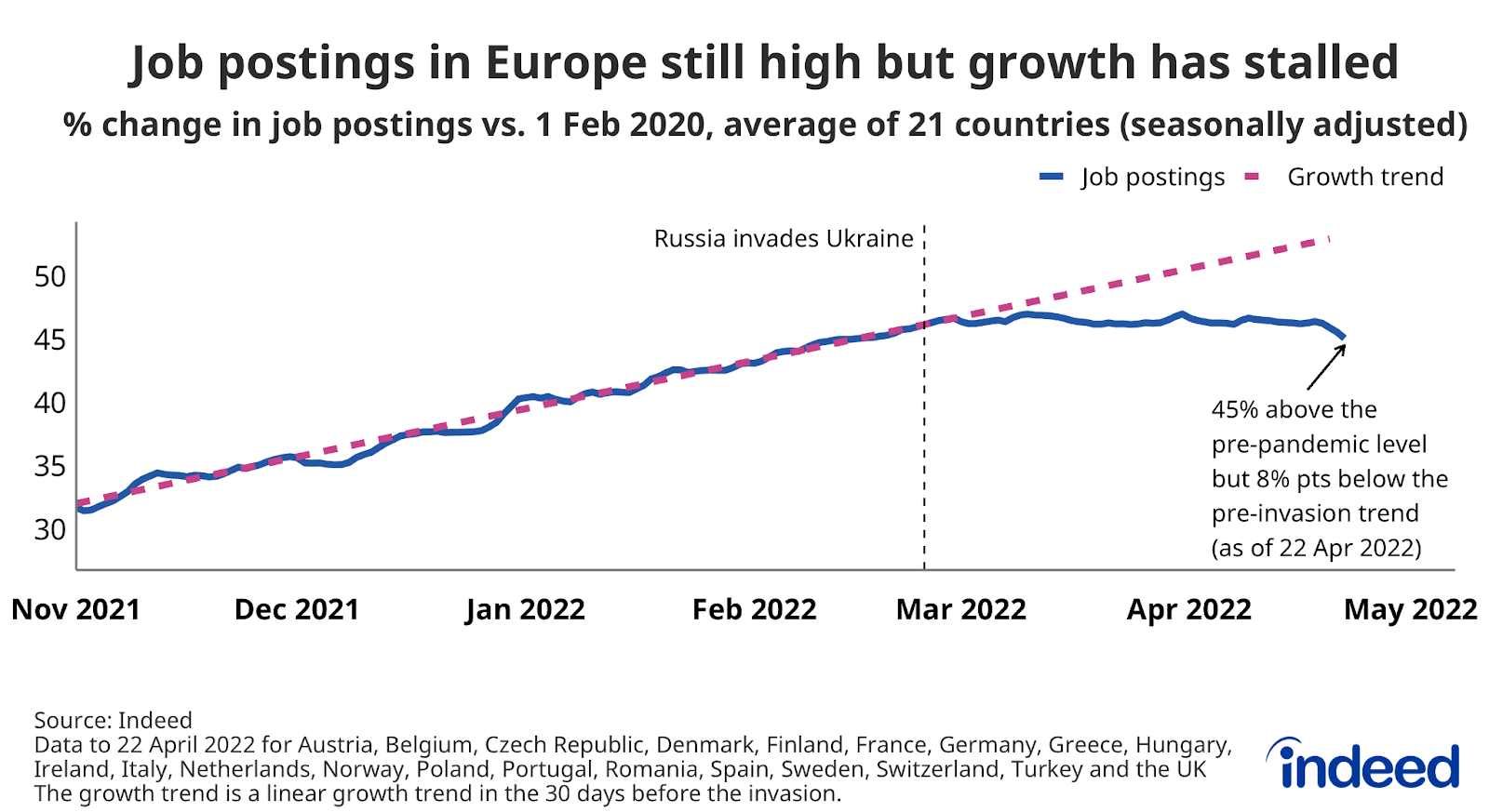

- Since late February, job postings in the 21 European countries with an Indeed job site have on average fallen eight percentage points relative to their pre-war trend.

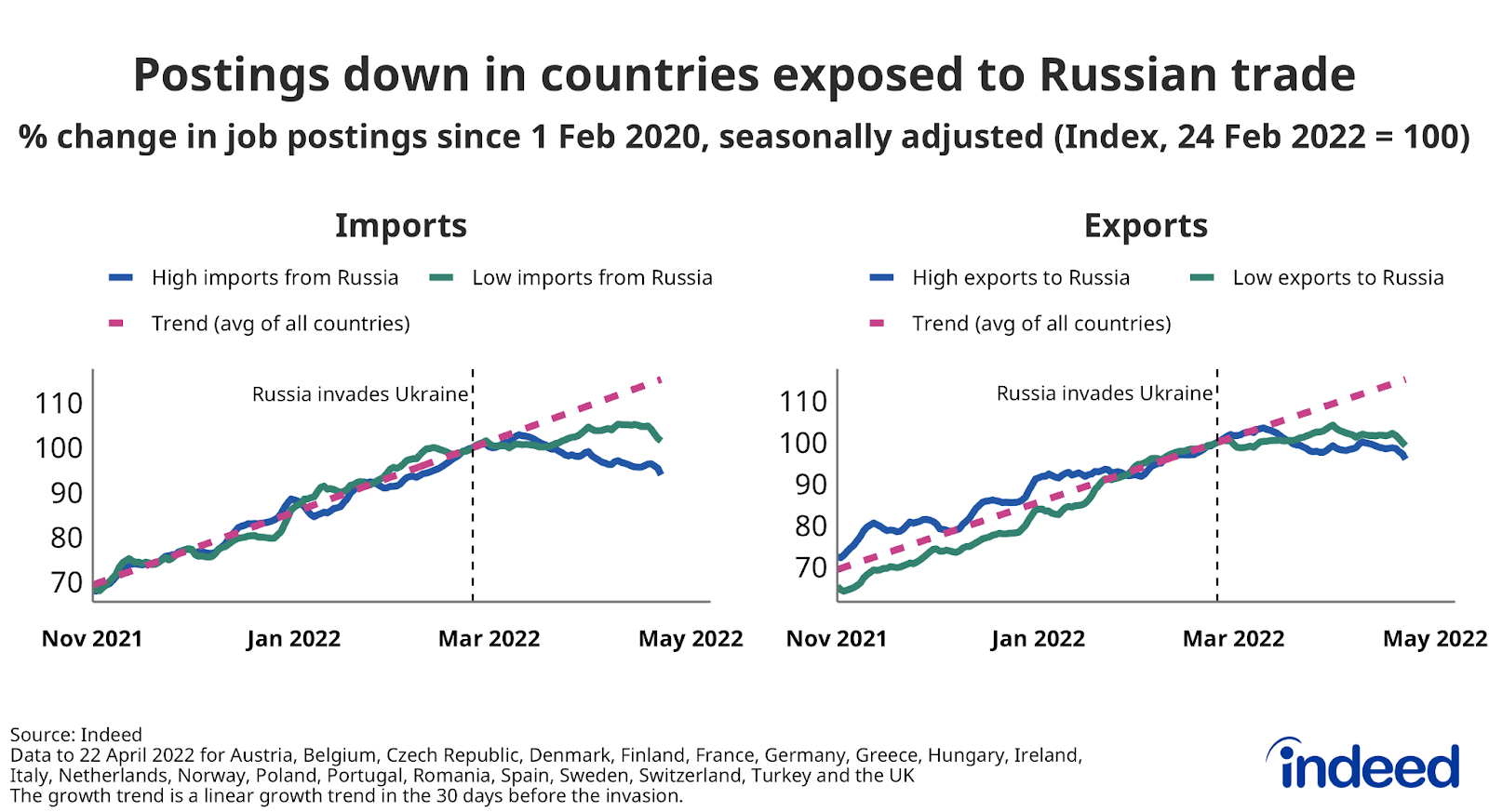

- Postings fell in countries with high imports from Russia and in energy-intensive sectors like manufacturing and transport, suggesting the war in Ukraine is starting to affect the labour market.

- Despite the slowdown, the labour market remains strong, with average postings in Europe still 45% higher than before the pandemic as of 22 April 2022.

The war in Ukraine appears to be affecting European economies just as inflation is biting. Consumer confidence is down and people are reducing non-essential spending. The World Bank and the IMF have shaved almost a percentage point off their global growth forecasts for 2022 and some countries may take an even bigger hit if the conflict is prolonged. One analysis estimates that if Germany is cut off from Russian energy imports, its GDP may decline by as much as 3% — a substantial impact. Commentators are increasingly talking about the risk of recession.

We looked at job postings in the 21 European countries that have an Indeed site to see how the labour market is responding to the crisis (see Methodology for a list of countries). Job ads are a timely indicator, highly correlated with economic output, that supplements surveys and other real-time measures of economic activity.

On average, Indeed job postings in Europe started to stagnate in late February, coinciding with the start of the war. And there were on average actual falls in job ads in countries with high imports from Russia and for the types of jobs found in energy-intensive sectors, like manufacturing and transportation.

These trends are consistent with the hypothesis that the war has weakened the economic outlook via three channels: confidence, which affects all countries and sectors; trade; and commodity prices. The silver lining is that postings are still high compared with historical levels, suggesting the labour market is still relatively strong. That might help mitigate the impact of the crisis on employment.

Job postings remain elevated but growth has stalled

The chart shows our usual measure of the growth of job postings on Indeed. As of 22 April 2022, average postings across the 21 countries in our sample were 45% above their pre-pandemic level. But growth fizzled out in late February. Postings are now one percentage point below their level on the day of Russia’s invasion and eight percentage points below their pre-invasion growth trend.

What led to the slowdown? One reason might be that postings simply reached their natural peak. After all, they could not have grown forever. The timing relative to the war in Ukraine might have been mere coincidence.

However, we found two trends that suggest the slowdown was — at least partly — related to the war. First, job postings on Indeed fell on average in countries with high trade with Russia relative to the size of their economies and continued to grow in countries with low trade with Russia, albeit at a slower rate than before the war. Second, job ads fell in occupational categories common in energy-intensive sectors — driving, logistics and manufacturing — while holding up in other categories.

Job postings fell in countries that trade more heavily with Russia

We approximated each country’s exposure to the economic fallout of the war by examining the ratio of goods imports from Russia to GDP in 2020 — a back-of-the-envelope measure that aims to capture exposure to war-related trade disruption (see Chart A, Box 3 in the ECB’s Spring forecast for a similar approach).

The median ratio of Russian imports to GDP in our sample was 0.6%. The most exposed countries by this measure were Turkey (2.5%) and Russia’s neighbours, Finland (2.5%) and Poland (1.9%). Among Europe’s largest economies, imports from Russia were relatively high in the Netherlands (1.7%) and the UK (0.9%). Germany (0.6%) and Italy (0.5%) were close to the average, while France (0.2%) and Spain (0.2%) were at the low end.

To visualise the trends, we assigned countries to two groups, depending on whether the value of their goods imports from Russia relative to GDP was above or below the median in our sample. We then plotted job posting growth for each group, indexing both to 100 on the day of Russia’s invasion of Ukraine.

On average, postings fell three percentage points since the invasion in countries with high imports from Russia and grew nearly one percentage point in countries with low imports from Russia (see chart below). Exports to Russia also seemed to matter. Job ads fell almost two percentage points in countries with high exports and less than half a percentage point in countries with low exports. Interestingly, even though postings grew in countries with low trade exposure, the average growth rate was lower than before the war. These trends are consistent with the hypothesis that the economic impact of the war is a combination of a global uncertainty shock and country-specific trade shocks.

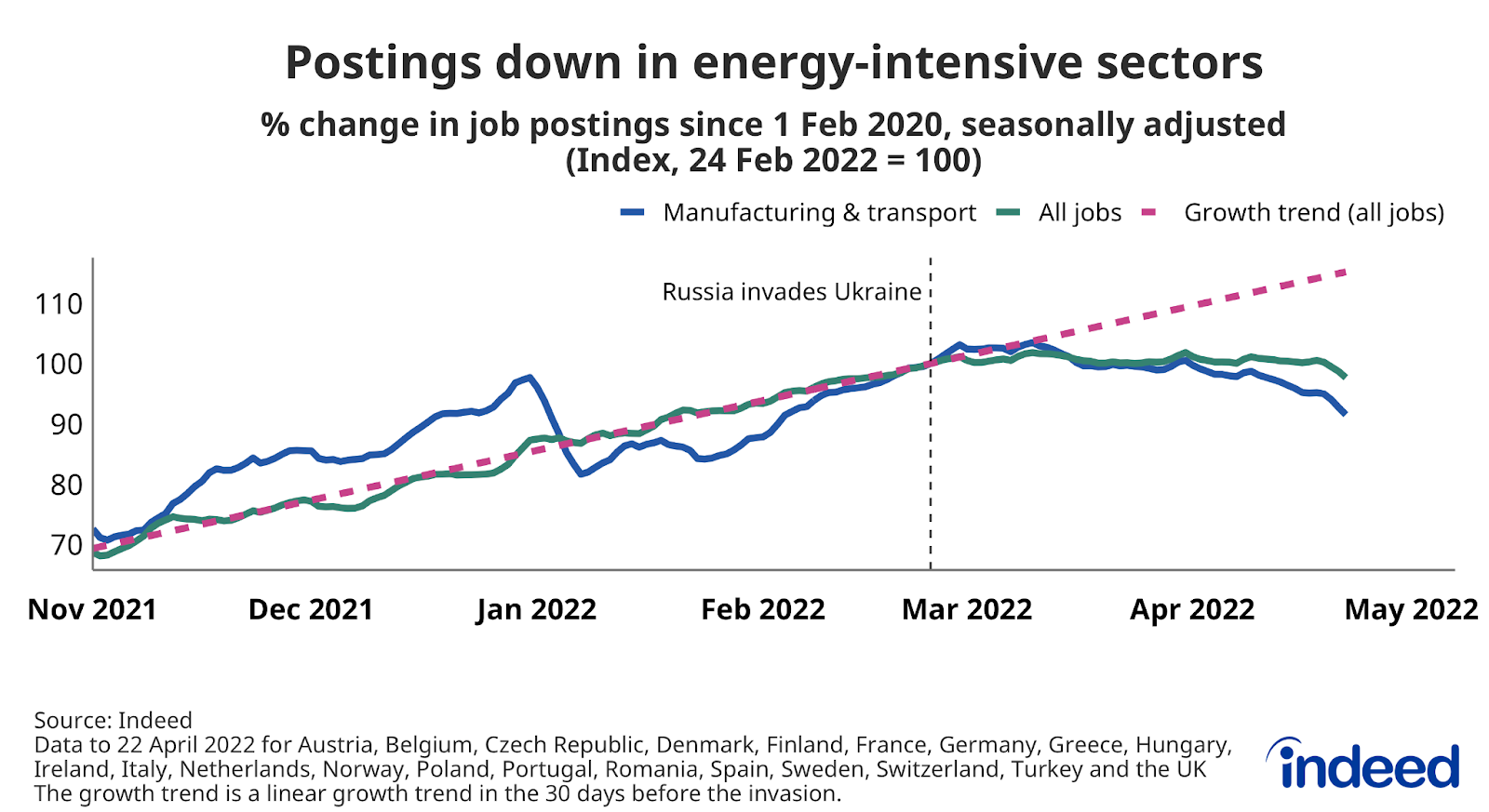

Job postings fell in energy-intensive sectors

Soaring commodity prices contributed to a record rate of inflation in the Euro area and the highest rate of inflation since the early 1990s in the UK in March. In this situation, one might expect energy-intensive sectors to pull back most on hiring. For instance, recent survey data indicate a sharper drop in business confidence in manufacturing than in services. Since mapping job postings to sectors is difficult, we looked instead at job ad trends in three of Indeed’s standard occupational job categories that can be considered typical of energy-intensive sectors: driving, logistics and manufacturing.

On average, postings in these areas fell five percentage points since late February across the countries in our sample — more than the one percentage point decline in all jobs. This suggests that commodity prices are another channel through which the war is affecting the economy and the labour market, although other factors, like supply-chain bottlenecks, might also be playing a role. If high inflation continues to dampen consumer spending, we may see the effects spread to other sectors too.

Labour market still robust but the slowdown is a concern

Imports from Russia and occupational trends are crude measures of country exposure to the Ukraine conflict. Still, the data offer evidence the conflict is having a real impact on the labour market. The good news is that job postings remain high relative to historical levels, indicating many employers are moving ahead with hiring plans. But the slowdown is a concern for the near-term economic outlook.

Methodology

Goods imports as a share of GDP in 2020 are calculated using data from the IMF and the World Bank. 2020 is the last year for which consistent trade and GDP figures are available for all the countries mentioned in this post. Results are similar when using 2019 data.

All job posting growth figures in this blog post are the percentage change in seasonally adjusted job postings since 1 February, 2020, using a seven-day trailing average, except when stated otherwise. 1 February, 2020, is our pre-pandemic baseline. We seasonally adjust each series based on historical patterns in 2017, 2018, and 2019. Each series, including the national trends and occupational sectors, is seasonally adjusted separately. We adopted this methodology in January 2021.

We included data for 21 European countries with an Indeed site: Austria, Belgium, Czech Republic, Denmark, Finland, France, Germany, Greece, Hungary, Ireland, Italy, Netherlands, Norway, Poland, Portugal, Romania, Spain, Sweden, Switzerland, Turkey and the UK. Recent job posting trends for individual countries can be found here.

The number of job postings on Indeed.com, whether related to paid or unpaid job solicitations, is not indicative of potential revenue or earnings of Indeed, which comprises a significant percentage of the HR Technology segment of its parent company, Recruit Holdings Co., Ltd. Job posting numbers are provided for information purposes only and should not be viewed as an indicator of performance of Indeed or Recruit. Please refer to the Recruit Holdings investor relations website and regulatory filings in Japan for more detailed information on revenue generation by Recruit’s HR Technology segment.