The February Labour Force Survey was one of the weakest monthly prints we’ve seen in a while. The headline 84,000 employment drop was bad, and there weren’t many positive details beneath the surface. Full-time private-sector employees led the net decline, hours worked also fell, and the drop was widespread across sectors, with only 3 out of 16 industries adding workers. Meanwhile, the 0.2 percentage point uptick in the unemployment rate (to 6.7%) understated the weakness, as it was accompanied by falling labour force participation.

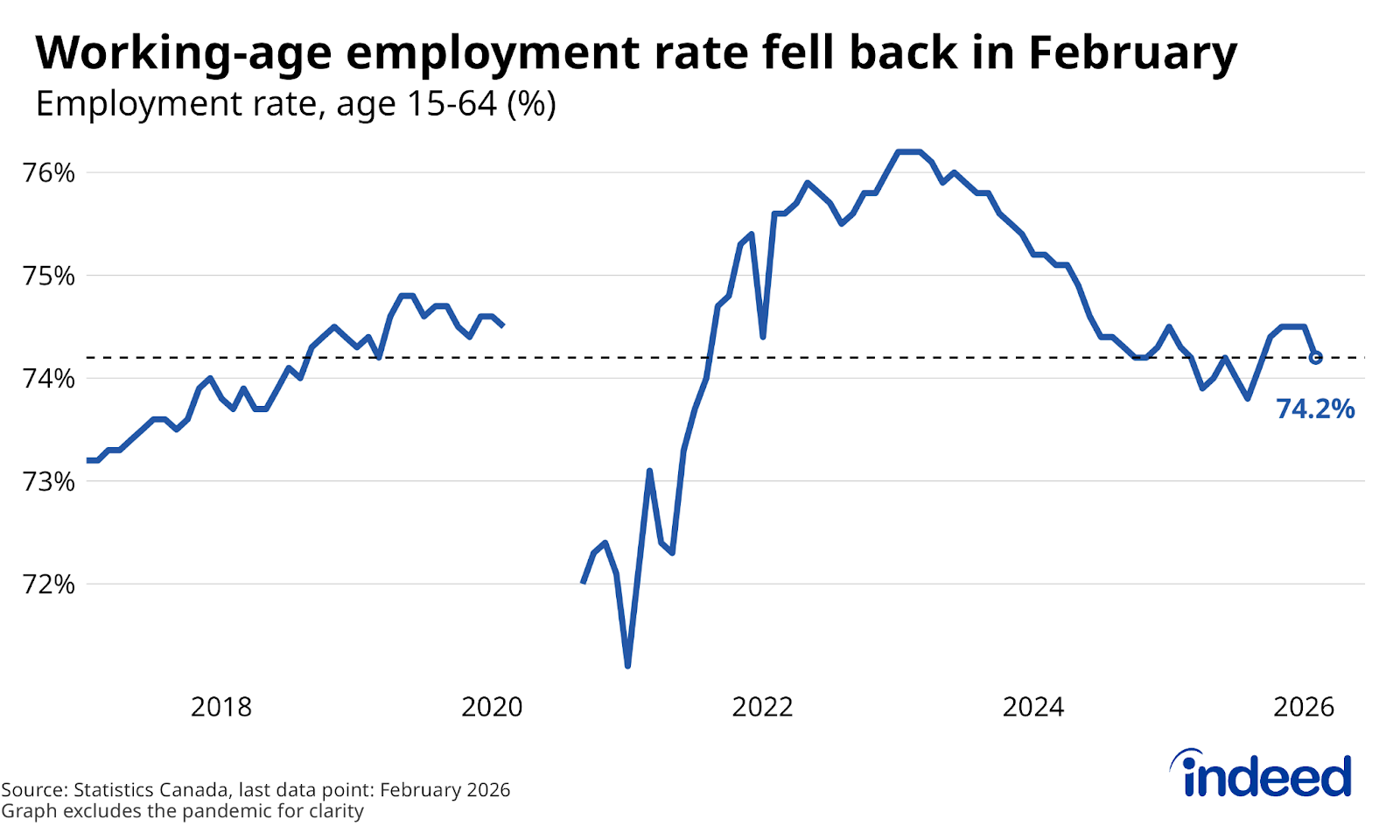

If there’s one somewhat silver lining in the numbers, it comes from zooming out at the broader context. The LFS is quite volatile: 2026 has started weak, but it followed a surprisingly strong stretch to end 2025 that didn’t have a clear economic driver. Some of the recent slip could be a direct reversal of that earlier strength. The working-age (15-64) employment rate dropped a sharp 0.3 percentage points, but at 74.2%, it remained slightly above where it stood in September, with youth (age 15-24) a key contributor to the volatility. To the extent that the previous strength was exaggerated, the trend has returned to the mean.

Projections for the Canadian economy in 2026 point to a soft but steady labour market, one where it’s tough to expect the weak market for job seekers to turn around. Given the monthly noise in the job numbers, a flat broader trend, along with slow population growth, will coincide with downbeat reports (like February’s). The concern now is that the looming clouds on the horizon, first from trade and now geopolitics, start to thunder.