Key points:

- Australia’s economic recovery has been uneven with remaining job losses heavily concentrated in lower-wage roles.

- Both higher and lower-wage construction and hospitality jobs have been notably slow to recover.

- Those joining the unemployment queue may be particularly vulnerable to the decision at the end of March to cut unemployment benefits.

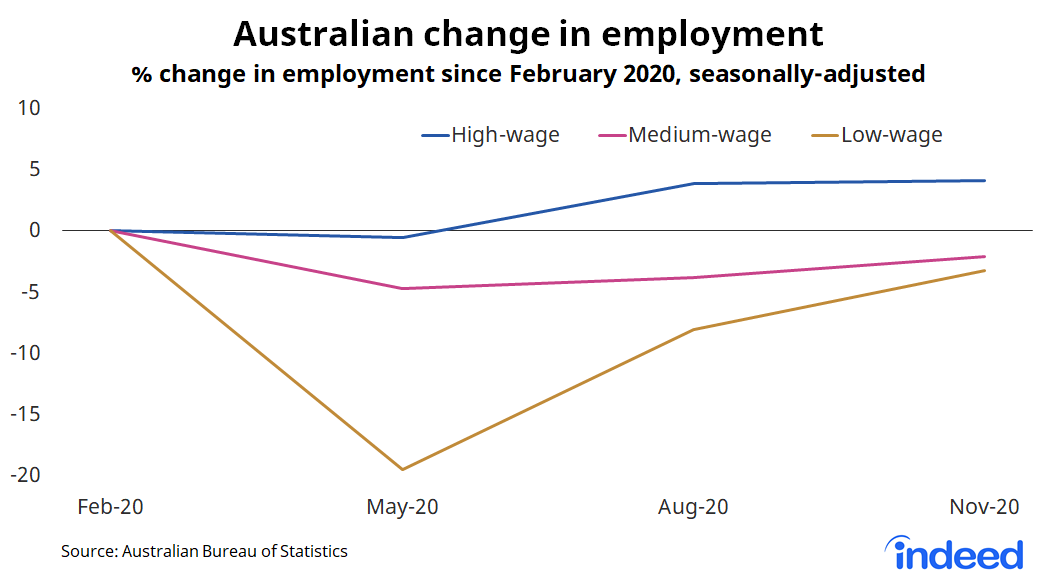

Australia has mounted an impressive but uneven recovery from the COVID-19 crisis. In January, Australian employment was just 0.5% below its pre-crisis peak in February, recovering much faster than in previous recessions. Employment among high-wage earners has thrived, easily exceeding pre-crisis highs. Unfortunately, the same cannot be said for those earning lower wages.

Employment remains well below its peak among lower-wage earners, driven largely by slow recoveries in hospitality and recreation, according to occupation-level data from the Australian Bureau of Statistics (ABS). Jobs for middle-wage earners also haven’t fully recovered.

Across the income distribution, there are some clear exceptions to these broad trends. For example, among high-wage roles, those in the construction sector haven’t recovered. And, in lower-wage roles, sales and gardening positions have bounced back.

These figures have clear implications for public policy. Is the recent decision to cut unemployment benefits, scheduled for the end of March, premature? And should some sectors receive ongoing support to reflect the greater damage they sustained during the pandemic?

Australia’s uneven jobs recovery

In November, employment in high-wage occupations was an impressive 4.1% above its pre-crisis level. High-earning occupations are those where average weekly earnings are $1,713 or more per week (see methodology section below). High-wage jobs dipped only modestly during the COVID-19 crisis, partly reflecting the high number of healthcare roles in this category and the ease with which many high-wage jobs can be performed remotely.

By comparison, COVID-19 has been a rollercoaster ride for lower-wage workers, defined as those earning under $864 per week. Restrictions on economic activity slammed lower-paying jobs, such as those in hospitality, recreation and retail, causing employment to fall initially 20%. While there has been improvement in recent quarters, employment in lower-wage occupations is still 3.2% lower than in February.

Medium-wage workers experienced a more modest jobs recession, but also a relatively slow recovery. In November, employment for these workers was still 2.1% below its February level.

Australian high-wage occupations have been a bright spot

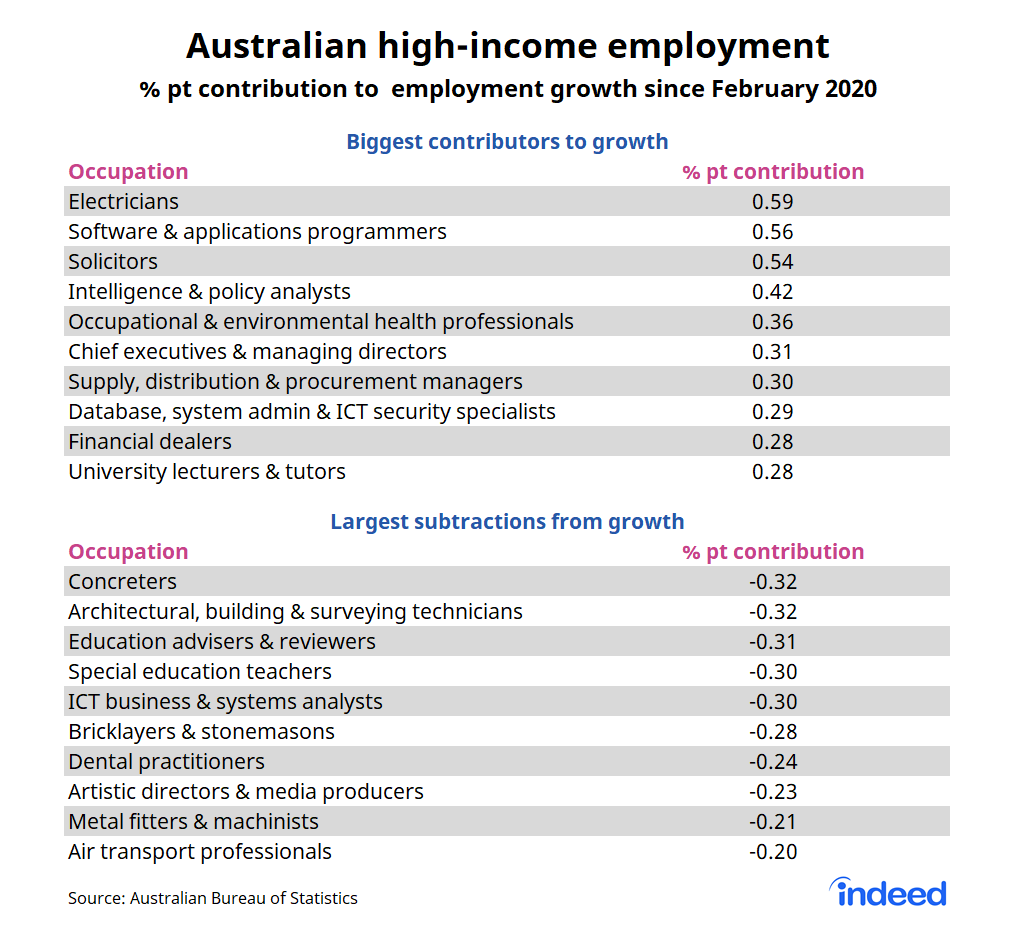

Although the nationwide employment trends are clear — high-wage employment has thrived — there are a range of high-earning occupations where COVID-19’s impact has persisted. The table below highlights the ten occupations that have contributed the most to and the ten that have subtracted the most from high-wage employment growth since February 2020.

The pandemic created few issues for electricians and tech workers. Solicitors and intelligence analysts also did well. And if you were a CEO or managing director, you had little to fear.

However, for many high-wage construction workers, the pandemic has been challenging. Occupations such as concreter, architect and bricklayer & stonemason are among those that have subtracted the most from high-wage employment growth. The construction sector was not directly targeted by economic restrictions, but it tends to be highly cyclical. Earlier research has established that construction is a consistent underperformer during a recession.

Results have been mixed for some industry groups. For example, employment for university lecturers & tutors has grown, possibly due to seasonal factors. November is exam season and universities don’t begin the academic year until March. At the same time though, employment for education advisers/reviewers and special education teachers have registered large declines.

The education sector has experienced considerable uncertainty throughout the pandemic, with schools temporarily shuttered and international students unable to enter the country. The university system was also denied access to JobKeeper wage subsidies.

Australian middle-wage occupations have recovered slowly

Some middle-wage jobs have fared well. Employment among primary school teachers is considerably higher than pre-crisis, which could also have a seasonal component.

Accountant, office manager, handyperson and multimedia specialist & web developer have been among the strongest middle-wage occupations during the recovery, contributing solidly to overall employment growth.

In contrast, the impact of COVID-19 restrictions is apparent in occupations such as retail manager and cafe manager. In construction, earthmoving plant operator and painter have posted job losses.

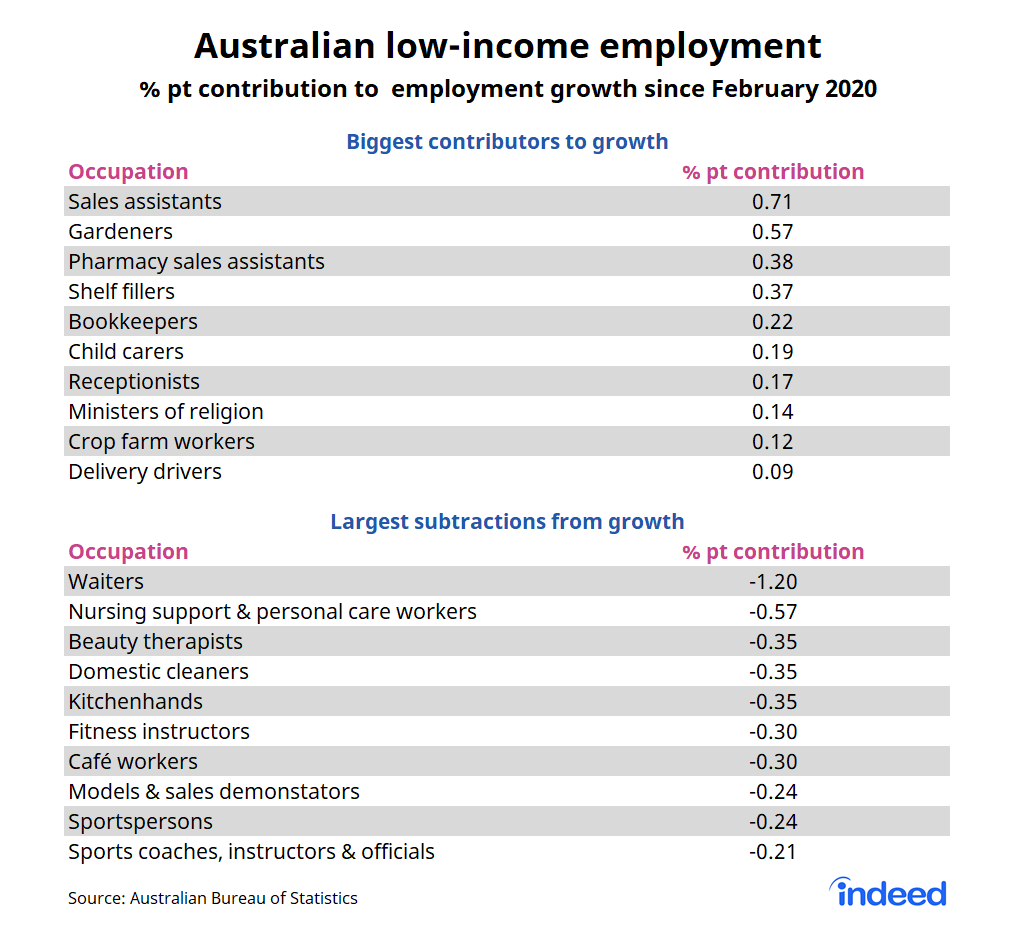

Australian low-wage occupations have been hit hardest

For lower-wage workers, jobs in cafes and restaurants have been slow to return, particularly for waiters, kitchenhands and cafe workers. Many restaurants continue to operate below capacity because of social distancing, limiting the scope for job growth. Victoria’s second shutdown, from July to November, also contributed to hospitality’s slow recovery.

The fitness sector has also been slow to come back. Fitness instructor, sportsperson and sports coach, instructor & official have subtracted considerably from employment growth since February.

Of course, some lower-wage occupations have bucked that trend. Leading the way are sales assistant, gardener, pharmacy sales assistant and shelf filler.

Childcare worker has been one of the strongest-performing lower-wage occupations despite temporary shutdowns and changes in government policy. And delivery driver, an occupation whose workers have played a key role connecting businesses with their customers during lockdowns, has also contributed to growth.

Implications

These trends have important implications for policy. First, COVID-19 job losses are highly concentrated among lower-wage occupations and to a lesser degree among medium-wage jobs. That means that those who joined the unemployment queue during the crisis are at risk of long periods of joblessness.

At the end of March, the federal government will discontinue the JobSeeker support supplement, which will cause unemployment benefits for a single person without dependents to fall from $1,115.70 per fortnight at the height of the crisis to just $565.70 per fortnight. That cut may be ill-advised given that it will be shouldered primarily by those least able to bear it.

Second, a small share of sectors remain highly affected by COVID-19 and recession. Ongoing fiscal support for hospitality, recreation and construction may be appropriate based on the profile of job losses across the income distribution. Stripping these sectors of support while their recovery is in its infancy may prolong the pain for affected workers.

Australia’s economic recovery has progressed faster than policymakers anticipated. But naturally, it has been uneven and some sectors or industries have been left behind. Ideally the recovery will continue to strengthen, creating opportunities in segments that have struggled. Still, Australia must not lose sight of the fact that the COVID-19 recession has generally hit lower-wage and more vulnerable workers much harder than those higher on the income distribution.

Methodology

Occupation-level data from the Australian Bureau of Statistics comprise 344 separate occupations. The threshold for high- and low-wage occupations was determined by first removing the top and bottom 10% of occupations to reduce the impact of outlier values and then calculating the standard deviation of wages from the remaining sample. A standard deviation is a measure of variance across a data set and can be used to determine how far a value, in this case occupation wage, differs from the average.

High-wage occupations are those that were more than one standard deviation above the average, above $1,713 per week, covering 28% of all occupations and 25% of employment. Low-wage occupations were more than one standard deviation below the average, below $864 per week, covering 17% of all occupations and 25% of employment.

Contribution to growth is calculated by taking the change in employment since February 2020 for each occupation against the overall change in category employment over the same time frame.