Key points:

- The share of US job postings on Indeed mentioning a 401(k) match has more than tripled since early 2020, averaging 24.7% between March and May 2026, compared to just 7.5% in early 2020.

- According to the Bureau of Labor Statistics, 72% of private-sector workers had access to a retirement plan in 2025, but only 53% participated, a 19-percentage-point gap.

- Notable gaps exist across occupations — 73% of management and professional workers participate in a retirement plan, compared to just 25% of service workers.

- Data from the BLS shows that employers spend $2.89 per hour worked on retirement and savings for management and professional workers, compared to $0.38 per hour for service workers.

Serious demographic change is underway — in 2010, 13.0% of Americans were age 65 or older. According to data from the Census Bureau, that number is now approaching 20% and is expected to keep growing as baby boomers age. As that share grows, so does the number of Americans depending on retirement savings to carry them through — savings that, for many, continue to be underfunded. Many of the workers filling the nation’s fastest-growing industries are the same workers least likely to be building retirement security through their jobs. Hiring has gone where the country needs it, but retirement benefits have not followed.

Data from Indeed show that employers have been promoting 401(k) plans and other defined contribution benefits more in recent years. And the Bureau of Labor Statistics’ National Compensation Survey (NCS), which includes Employee Benefits (EBS) and Employer Costs for Employee Compensation (ECEC), makes the retirement divide measurable. Access, participation, and the dollars employers contribute on workers’ behalf all vary sharply by occupation, wage level, and employer size.

Access to an employer-sponsored retirement plan is one of the clearest ways compensation shapes long-term financial security, not just next month’s paycheck. Because default enrollment and automatic payroll deductions nudge people to save when willpower alone often falls short, workers with access tend to save more consistently than those without. Yet that access remains uneven — concentrated in certain industries and full-time roles — meaning it’s often job quality, not just individual choice, that determines who builds retirement wealth over a career.

What Indeed job postings signal about retirement benefits

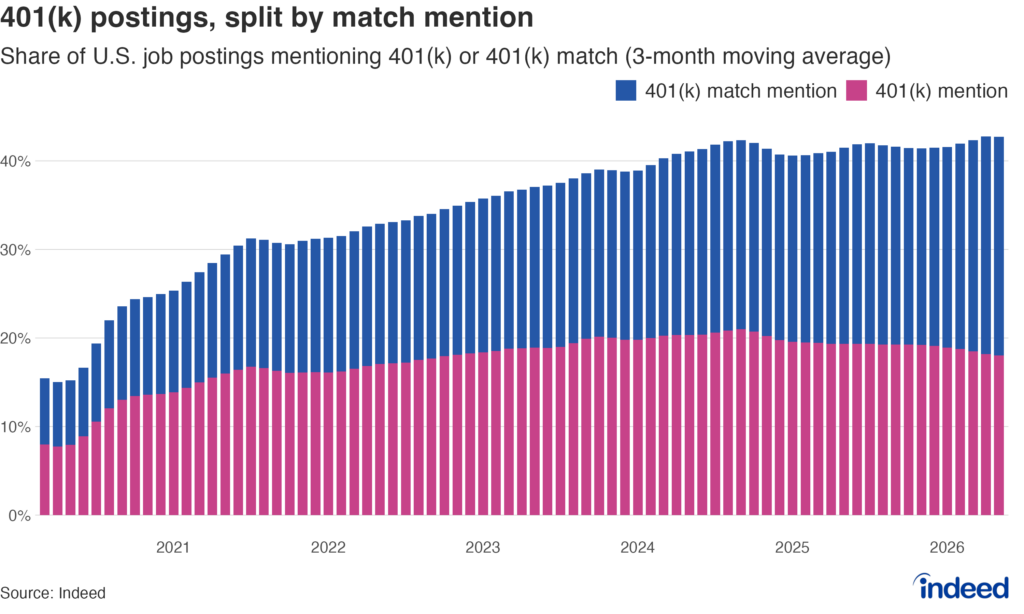

Indeed job postings show how employers are promoting retirement benefits in their job descriptions, and 401(k) mentions have grown since the start of the pandemic. In early 2020, just over 15% of postings on Indeed mentioned a 401(k) plan, with almost half (7.5%) mentioning that the employer provided a match to employee savings. By May 2026, nearly 43% of all postings mentioned a 401(k), and more than half (24.7%) mentioned a match. The share advertising a match has now surpassed the share that simply mentions a 401(k), a shift in what employers are highlighting about their retirement offerings.

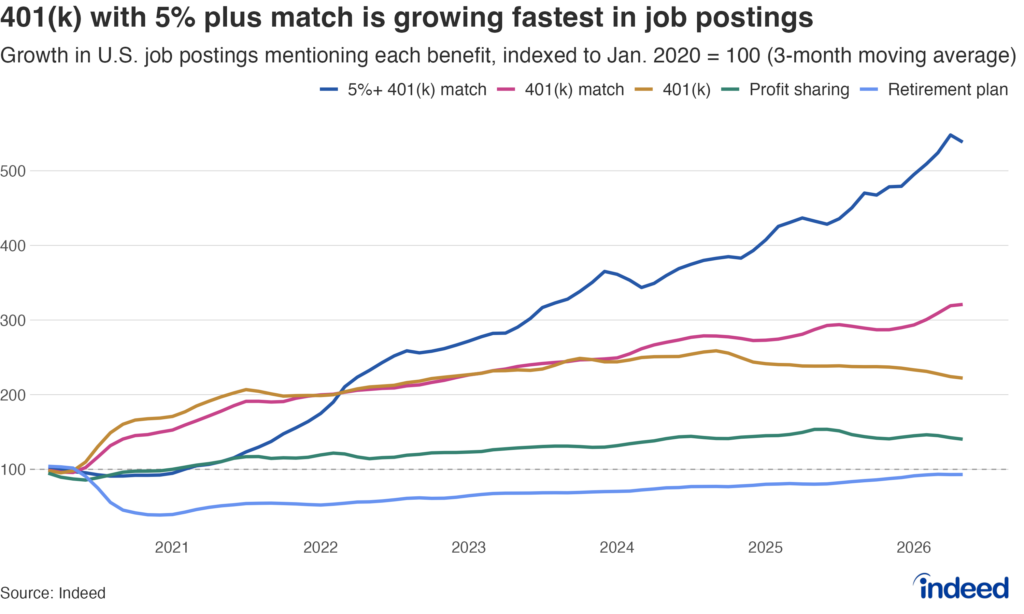

Not only are matches becoming more common, they have also grown more generous. When indexed to January 2020, the three-month-moving-average share of postings advertising a 401(k) match of 5% or higher has risen more than fivefold, outpacing the growth in any other category of retirement benefit. Over the same period, mentions of a generic “retirement plan” have barely moved from the baseline, and mentions of profit sharing have only grown modestly. While the 5% or higher match remains a small share of job postings, it is the retirement benefit category that is growing fastest.

The retirement divide is measurable

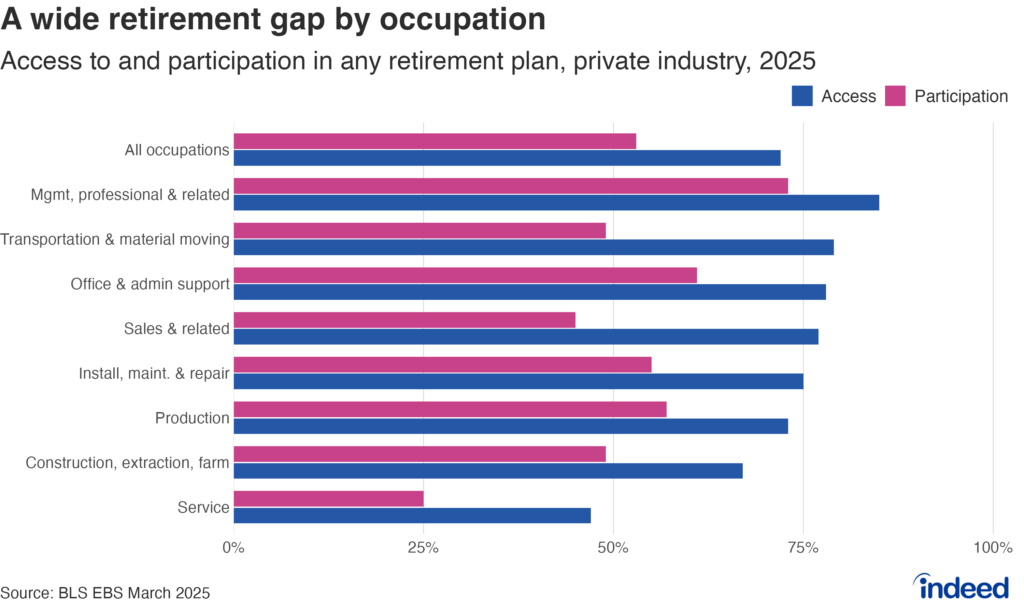

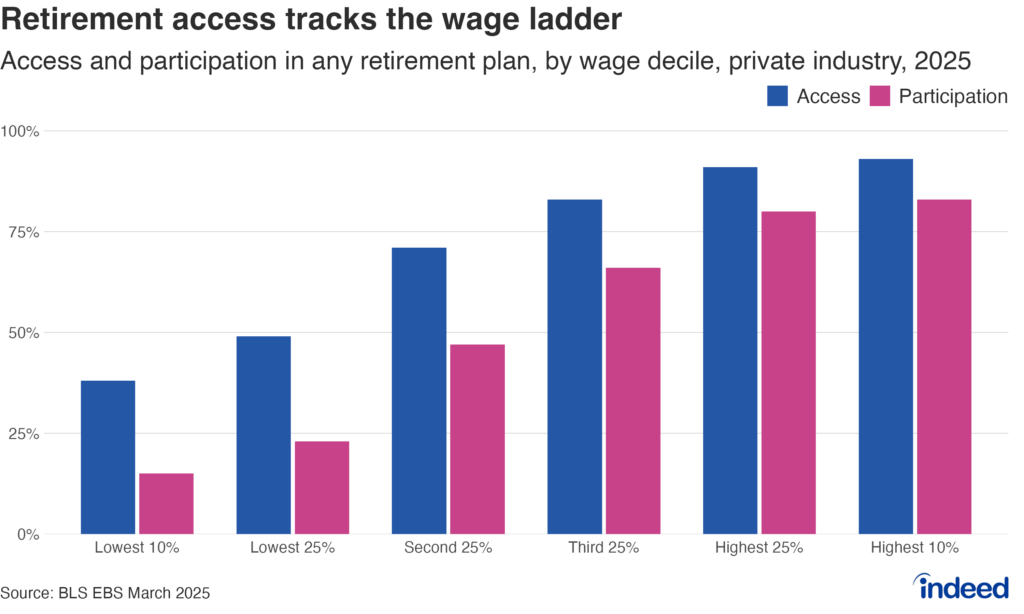

The rise in 401(k) advertising is one signal of what employers are putting forward to attract workers. But what those benefits look like for the workers receiving them is where the structural divide becomes visible. The differences in retirement benefits offered in the private sector begin at the door. According to the BLS, almost three-quarters (72%) of all private-sector workers had access to any retirement plan in 2025, and 53% participated. That access rate has crept up only modestly over the past 15 years (from 65% in 2010), while the participation rate has barely moved, from 50% to 53%.

Beneath the averages, the divide is severe. 85% of management and professional workers have access to a retirement plan, and 73% participate in one. Among service workers — a category that includes food-service workers, home health aides, janitors, and personal-care workers — less than half (47%) have access, and only 25% participate. The access gap between management and service workers has not budged in 15 years — 38 percentage points in both 2010 and today. The workers who already earn less and can least afford to retire are systematically the workers furthest from any meaningful employer-provided retirement plan.

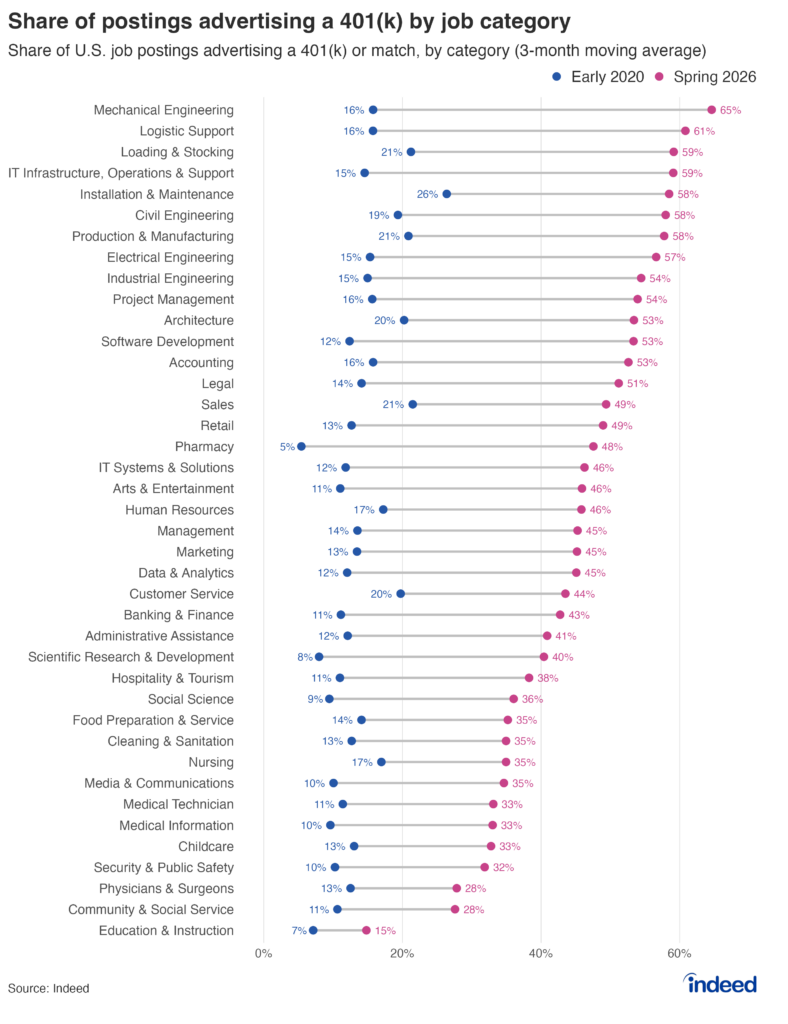

Indeed job postings provide a unique perspective from the initial recruitment phase. Since early 2020, the three-month moving average share of job postings advertising a 401(k) plan or match has grown (unevenly) in every one of Indeed’s occupational sectors. Within specialized and professional categories, the share often reaches half of all postings or more — 53% in accounting and software development, 58% in installation & maintenance, and 65% in mechanical engineering. In service and caregiving categories, mentions of 401(k) in postings are lower — 33% in childcare and 35% in nursing, cleaning & sanitation, and food preparation & service.

Contributions from employers follow the same pattern. Newly released ECEC data from March 2026 show employers contribute $2.89 per hour worked towards retirement for management and professional workers — more than seven times the $0.38 per hour they contribute for service workers. Compounded over a 40-year full-time career at 2000 hours a year, the difference between those two contribution rates exceeds $200,000 in employer contribution alone, even before accounting for worker contributions or any investment growth. The harsh reality is that many workers in service occupations may never have access to an employer-paid retirement system, and many who do have access may choose not to participate in the face of more immediate financial constraints.

The same pattern radiates outward across every dimension of the workforce. Almost all (93%) workers in the top 10% of earnings have access to a retirement plan, and 83% participate. Workers in the bottom 10% have a 38% access rate and a 15% participation rate. The gap here is even wider than across the occupational ladder, with 55 percentage points separating access (from top to bottom) and 68 percentage points separating participation. Similar divides exist among large and small employers and full-time and part-time workers.

The strongest labor demand often comes from industries with the weakest retirement security

Some of the occupations driving the most hiring in recent years offer some of the weakest long-term retirement benefits. Healthcare and social assistance accounted for the largest net job growth in the US over the last year, driven by demand for nurses, home health aides, and personal care workers. In May 2026, 70,000 jobs were added in leisure and hospitality, which has remained relatively strong as consumer spending continues to be robust. While job growth is robust in these sectors, the retirement benefits often are not.

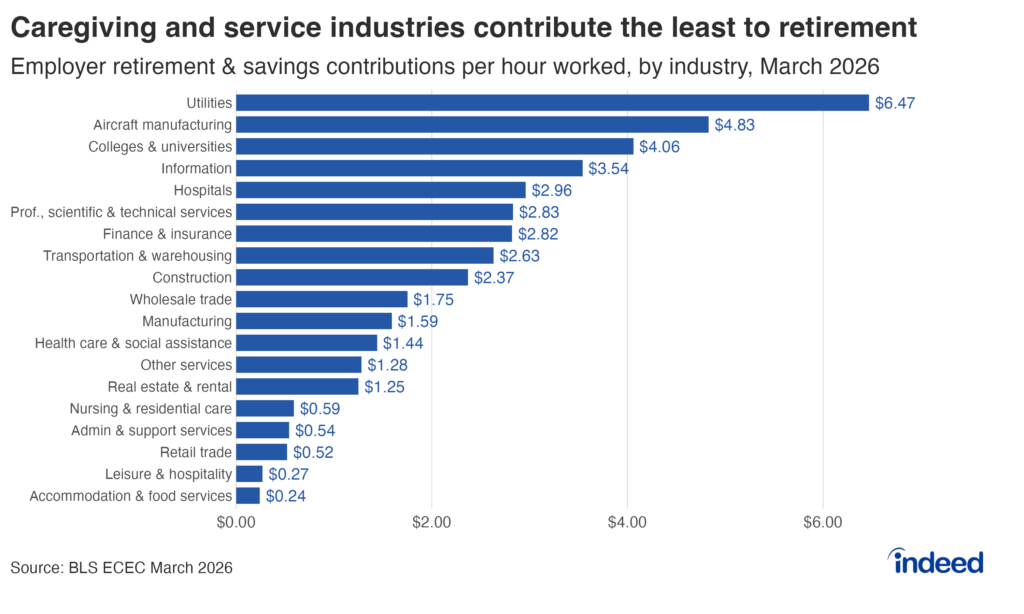

The contribution data from the ECEC makes the divide concrete. The March 2026 data show employers in accommodation and food services contributed just $0.24 per hour worked toward retirement. Leisure and hospitality, retail trade, administrative and support services, and nursing and residential care all clustered below $0.60. At the top of the employer contributions sit utilities, aircraft manufacturing, and information, where employers contribute $6.47, $4.83, and $3.54 per hour worked, respectively. Utilities and aircraft manufacturing are also among the most heavily unionized industries, and according to the BLS, union workers have 91% access to a retirement plan compared to 71% for nonunion workers. The contribution gap between the top and the bottom is more than twenty-five-fold, and many of the sectors growing the fastest are at the bottom of the contribution ladder.

Conclusion

The data tell a consistent story — job growth and retirement security are pulling in opposite directions. Some of the sectors adding the most jobs are the same ones that contribute the least towards employees’ retirement. The jobs are there, but the retirement security is not. As the country ages and the need for retirement funds grows, this divide may put additional strain on public benefits, including Medicaid and Supplemental Security Income (SSI), as well as on non-profits that work to support elderly Americans in need.

For employers, the rise in 401(k) advertising on Indeed shows that some employers are highlighting retirement benefits when hiring, though whether those benefits reach the workers most in need of retirement security is a separate question.

For job seekers, retirement benefits are more visible in job postings than they used to be, but that visibility isn’t evenly distributed. Two workers with the same starting salary, but in different occupations or industries, can face different retirement trajectories, and much of that difference is set by the employer, not by the worker’s saving discipline.

The retirement divide is structural. Closing it will be too.

Methodology

Access and participation estimates are from the BLS National Compensation Survey’s (NCS) Employee Benefits (EBS), March 2025 reference period, private industry workers. Employer retirement contributions are from the BLS NCS’s Employer Costs for Employee Compensation, March 2026 release, private industry.

Indeed’s job posting figures are based on monthly counts of U.S. job postings from January 2020 through May 2026. Each posting is classified by Indeed’s taxonomy as carrying one of several mutually exclusive 401(k)-related terms: a “401(k)”, a “401(k) matching,” or one of nine specific percent-match tiers (2% through 10%); and “profit sharing” as well as generic “retirement plan”. Posting shares are calculated as a 3-month moving average. Indexed chart values show the share of postings in each category as a percentage of that category’s January 2020 baseline (January 2020 = 100). Indexed values reflect relative growth from the baseline period, not absolute share of total postings.