Key points:

- Job openings dropped slightly to 6.9 million from a revised 7.2 million in January, with little movement as employers remained cautious.

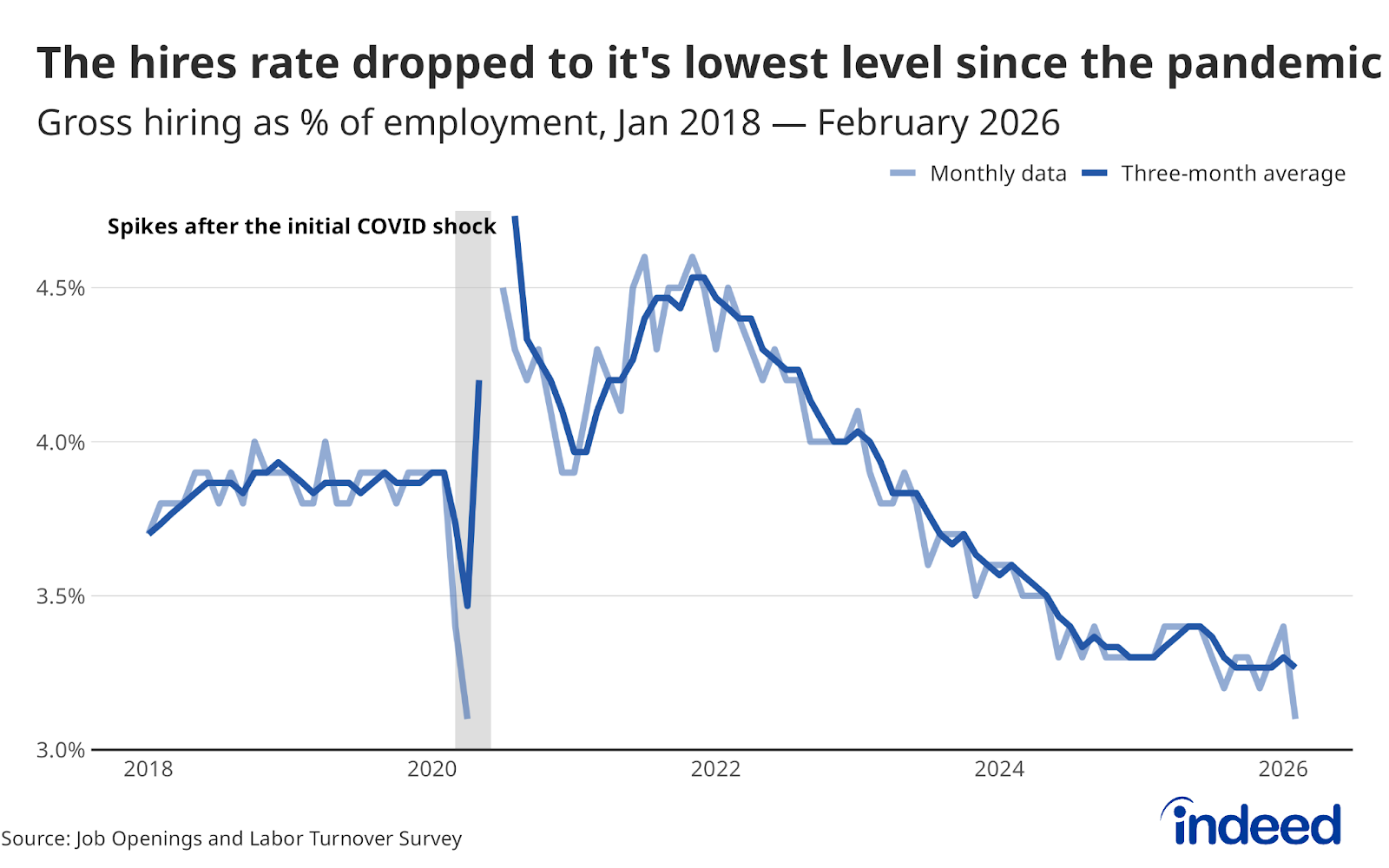

- The hires rate declined to 3.1 in February, matching the COVID-low observed in April 2020.

- The quits rate has stood at or below 2.0% for eight consecutive months and dropped to 1.9% in February.

- Layoffs remained low, but ongoing volatility spurred by the conflict in the Middle East could rapidly change the picture.

The February JOLTS report showed a slight decline in job openings, to 6.9 million from 7.2 million in January. The low-hire, low-fire dynamic that has defined this market for the better part of a year was firmly intact through February. The engine was running; it was just stuck in neutral.

It is very important to note that these data predate the conflict in the Middle East, making it both a clean read on where the labor market stood and a snapshot that may already feel like ancient history. The conflict with Iran, which began on February 28, sharply increased oil prices and is likely to ratchet up global inflationary pressure. Brent crude stands above $110 a barrel, and economists are raising the specter of stagflation, rising prices alongside a labor market that was already losing momentum before the first strike was launched.

Notably, the hires rate declined to 3.1 in February, the lowest level since January 2011, matching the COVID-era low observed in April 2020. Hires rates have dropped across a number of sectors, with the most severe declines over the last year registered in the construction and professional & business services sectors. The decline from 3.4 to 3.1 between January and February is the largest drop in a single month since 2016 (outside of the pandemic), which is concerning given the ongoing impacts of the conflict in Iran.

The quits rate remains the number to watch — and continues to disappoint. Eight consecutive months at or below 2.0% reflects a workforce that doesn’t feel it can afford to take chances. That risk aversion was elevated before oil prices spiked. And with energy costs climbing and household budgets strained, workers may be even less likely to leave jobs voluntarily. The market was stuck in neutral going into this conflict. Getting it into gear just got harder.

The Federal Reserve’s position has also grown more complicated. A softening labor market argues for rate cuts; an oil-driven inflation surge argues against them. February’s JOLTS offers one last clear look at the road behind us. The road ahead is considerably less certain.