Key points:

- Nonfarm payrolls fell by 92,000 in February, according to the Bureau of Labor Statistics, far below consensus expectations of roughly 50,000.

- Healthcare — a sector that sustained job growth through most of 2025 — shed 28,000 jobs, largely because a Kaiser Permanente strike sidelined more than 30,000 workers during the BLS survey week. Even adjusting for the strike, payrolls would have been deeply negative.

- The labor force participation rate slipped to 62%, its lowest level since December 2021 outside the pandemic, even as the prime-age employment-to-population ratio held at 80.7% — still above the 2019 average of 80%.

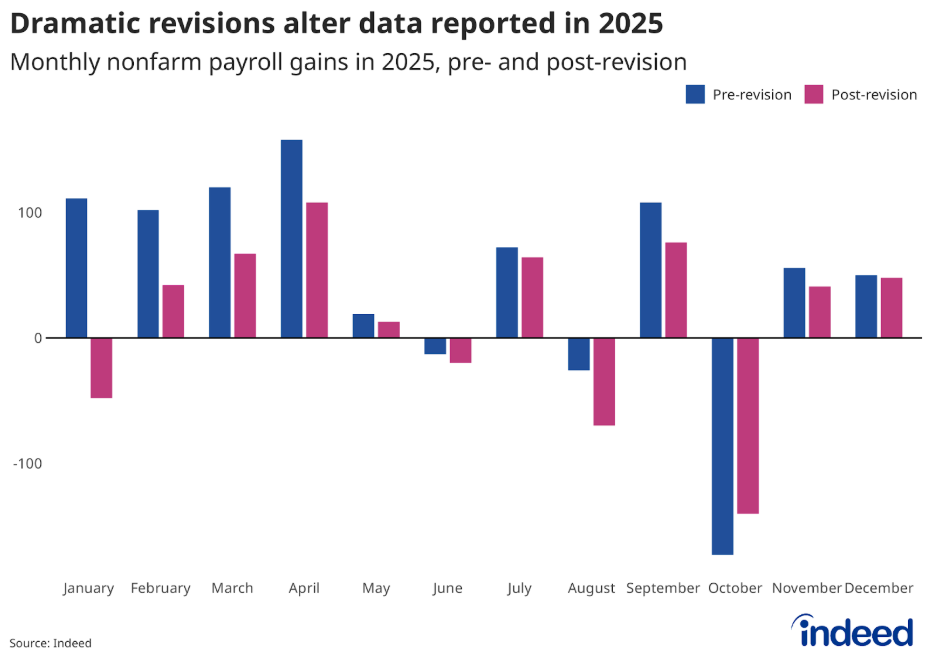

Today’s jobs report was overwhelmingly disappointing — there’s no other way to say it. While economists expected the economy to add 50,000 jobs in February, today’s release shows we lost 92,000 jobs instead. Job loss occurred in nearly every sector of the economy, including healthcare, a major change from the story we’ve become accustomed to over the past year. Additionally, revisions to December show we ended 2025 in a worse spot than we previously believed. While January’s jobs report raised hopes that the labor market might be turning a corner, the February report swings that discussion in the opposite direction, pointing instead to continued evidence of softening and emerging warning signs across several industries.

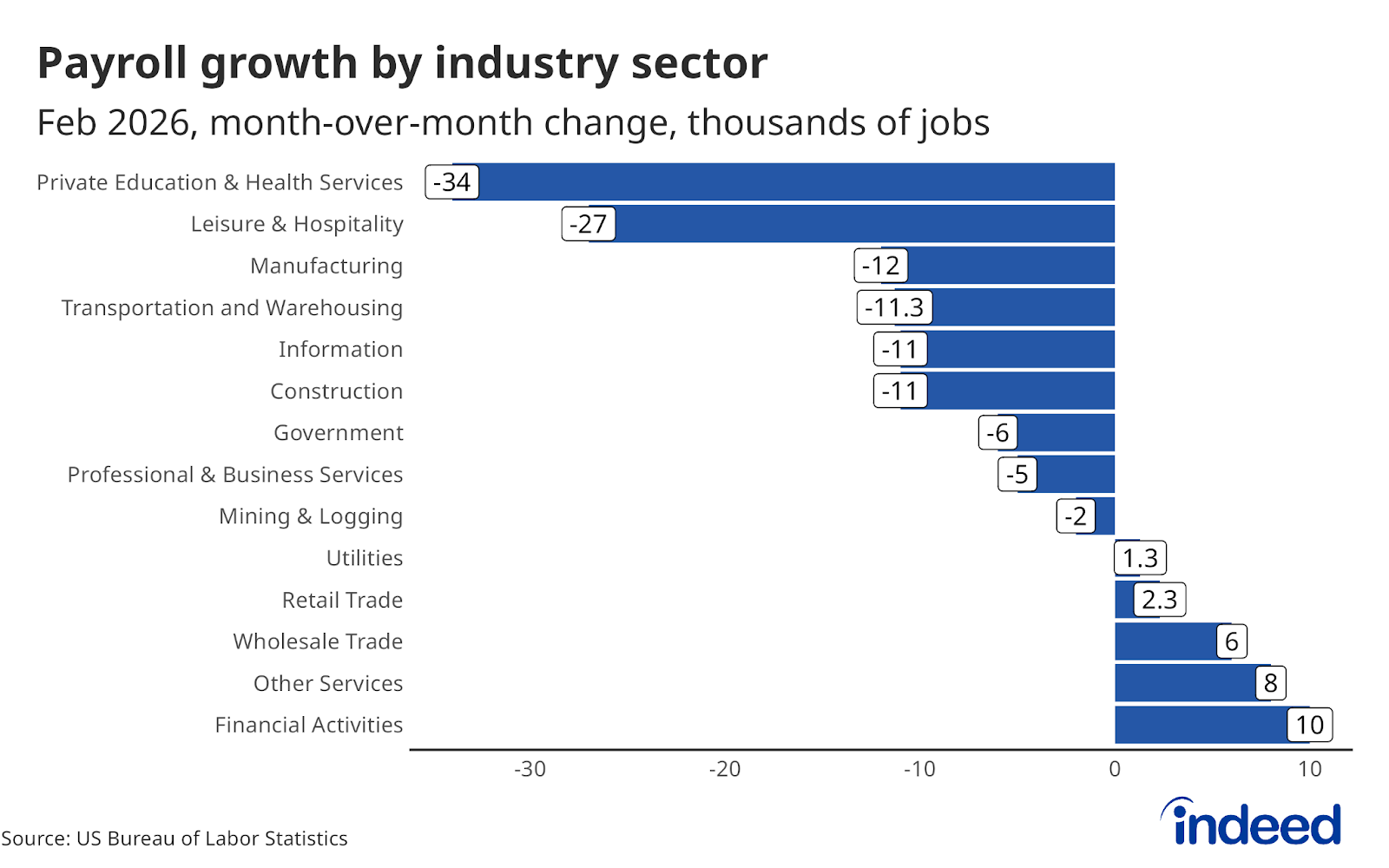

The healthcare subsector shed 28,000 jobs in February after adding an average of 30,000 jobs per month over the past 12 months. While this was partially driven by strikes, the change is still notable. Leisure and hospitality also fell by 27,000 jobs, as employment declined in accommodation and food service roles. The only sectors to add jobs in February were financial activities, wholesale trade, retail trade, utilities, and other services.

The labor market has continued to hum along in recent years, often balancing bright spots in the data with otherwise glum news. Unfortunately, today’s report looks weak across the board.

For policymakers at the Federal Reserve, the outlook got far more complicated as they head into their mid-March meeting. Inflation remains stubbornly above the Fed’s 2% goal, but the labor market may be moving from merely bent to genuinely broken. Even more concerning, the February data does not take the evolving war with Iran into account. The March jobs report may reflect early effects of the conflict, but much of the potential impact depends on the duration and extent of the war.

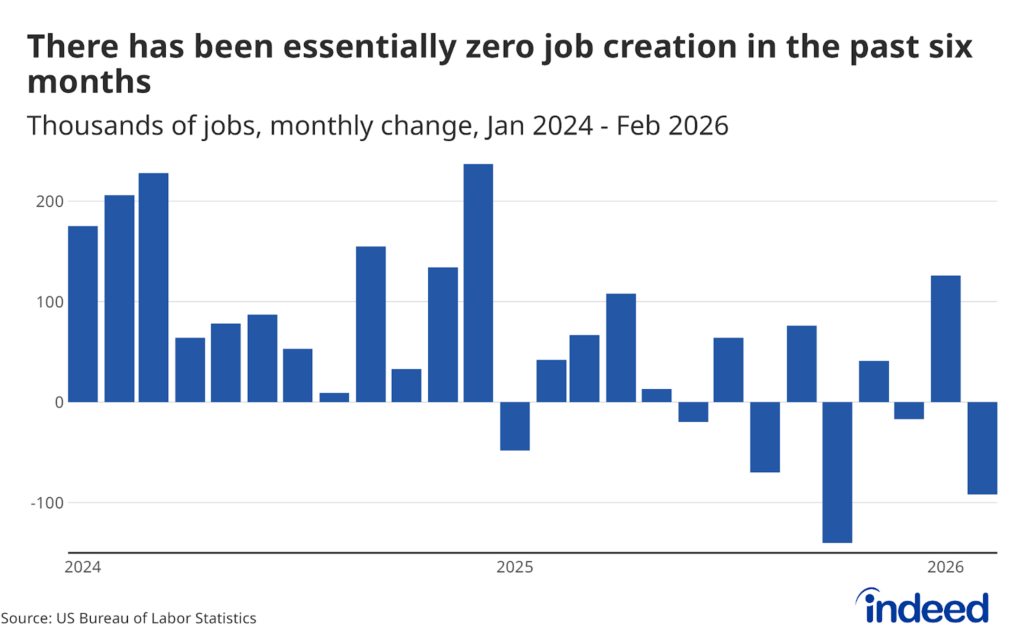

Today’s data show that the labor market has averaged essentially zero net job creation over the past six months. This is concerning because when an economy stops creating jobs, it’s often not long before it starts losing them. The key question now is whether February was a temporary setback or the start of a more concerning trend.