Key points:

- Headline numbers in job reports show an economy still adding jobs, with low unemployment and layoffs.

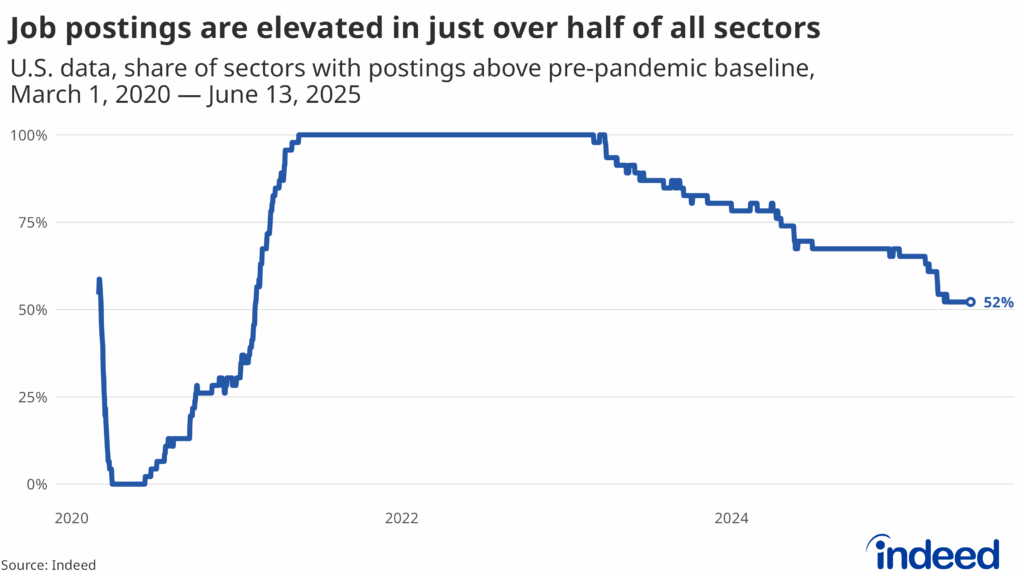

- The number of sectors with strong job postings is declining, landing at a little more than half in May.

- The labor market — lately in a state of deep freeze — is turning into stagnation as employers and employees hold off on making key decisions.

Our monthly Labor Market Update examines important trends using Indeed and other labor market data. Our US Labor Market Overview Chartbook provides a more comprehensive view of the US labor market. Data from our Job Postings Index — which stood 5.8% above its pre-pandemic baseline as of June 13 — and the Indeed Wage Tracker (including sector-level data) are regularly updated and can be accessed on our data portal.

Looking for a job is always challenging, but it can feel especially frustrating when the economic headlines don’t match one’s experience. Economic reports continue to show a strong labor market: unemployment remains low, job growth consistently exceeds expectations, and layoffs are minimal. Yet many job seekers are finding fewer work opportunities, especially students and recent graduates (internship and summer job postings are both at multi-year lows). At the same time, immigration restrictions, shifting trade policies, and the looming threat of Gen AI’s effect on the labor market add to the uncertainty.

In short, while the data paints a picture of resilience, the lived experiences of many Americans tell a different — and more sobering — story.

May’s job report showed the economy beating expectations and adding 139,000 jobs. But a closer look reveals a more nuanced picture. The breadth of job growth is narrowing. May’s diffusion index — a measure of how many sectors are adding jobs to the economy — stood at 50%, indicating neither a strong nor weak mix, but a downward trend over time. Healthcare continues to be a major driver, with 44% of new jobs in May coming from that sector.

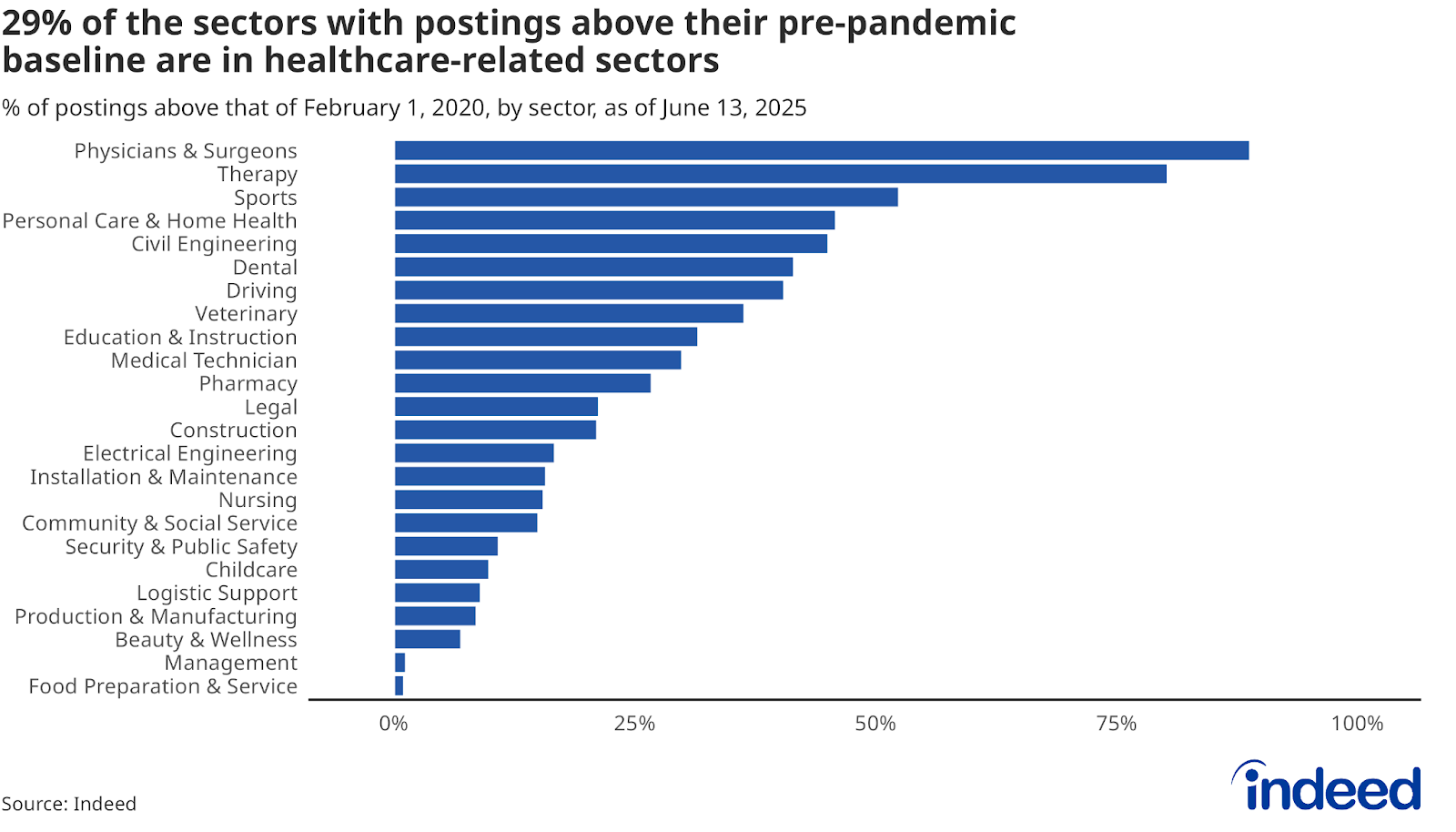

As for job opportunities, as of June 13, 52% of all sectors have job postings above their pre-pandemic baseline, marking a steady decline following strong gains through 2022. Unsurprisingly, given May’s job report, 29% of sectors outperforming their pre-pandemic posting levels are healthcare-related. There are still some bright spots — engineering roles remain resilient, and certain in-person service jobs (like food preparation, childcare, and personal care) continue to show strength. However, traditional office-based roles and tech jobs (along with retail and hospitality job postings) have been on a downward trend. Despite overall job growth, the foundation is becoming increasingly concentrated — and more fragile.

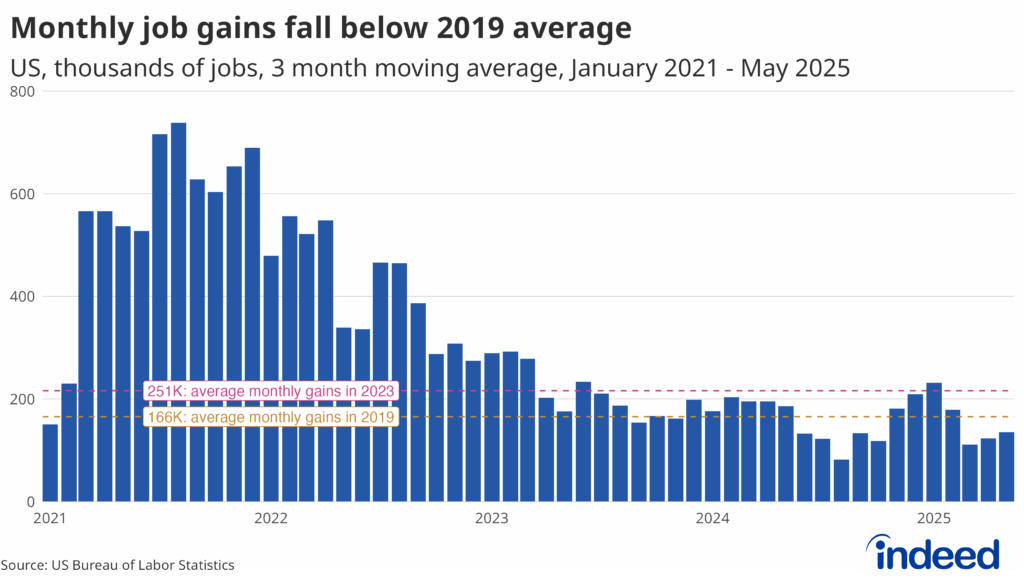

While May’s job report exceeded expectations, the broader trend tells a more cautious story. The three-month average of job gains has consistently fallen below 2023 levels, and for the past three months, it’s also lagged behind 2019’s pre-pandemic averages. The key concern is not the speed of the slowdown, but its persistence. While the labor market has undergone a necessary cooling period, it may be approaching an inflection point where the capacity for further deceleration without broader economic consequences becomes uncertain.

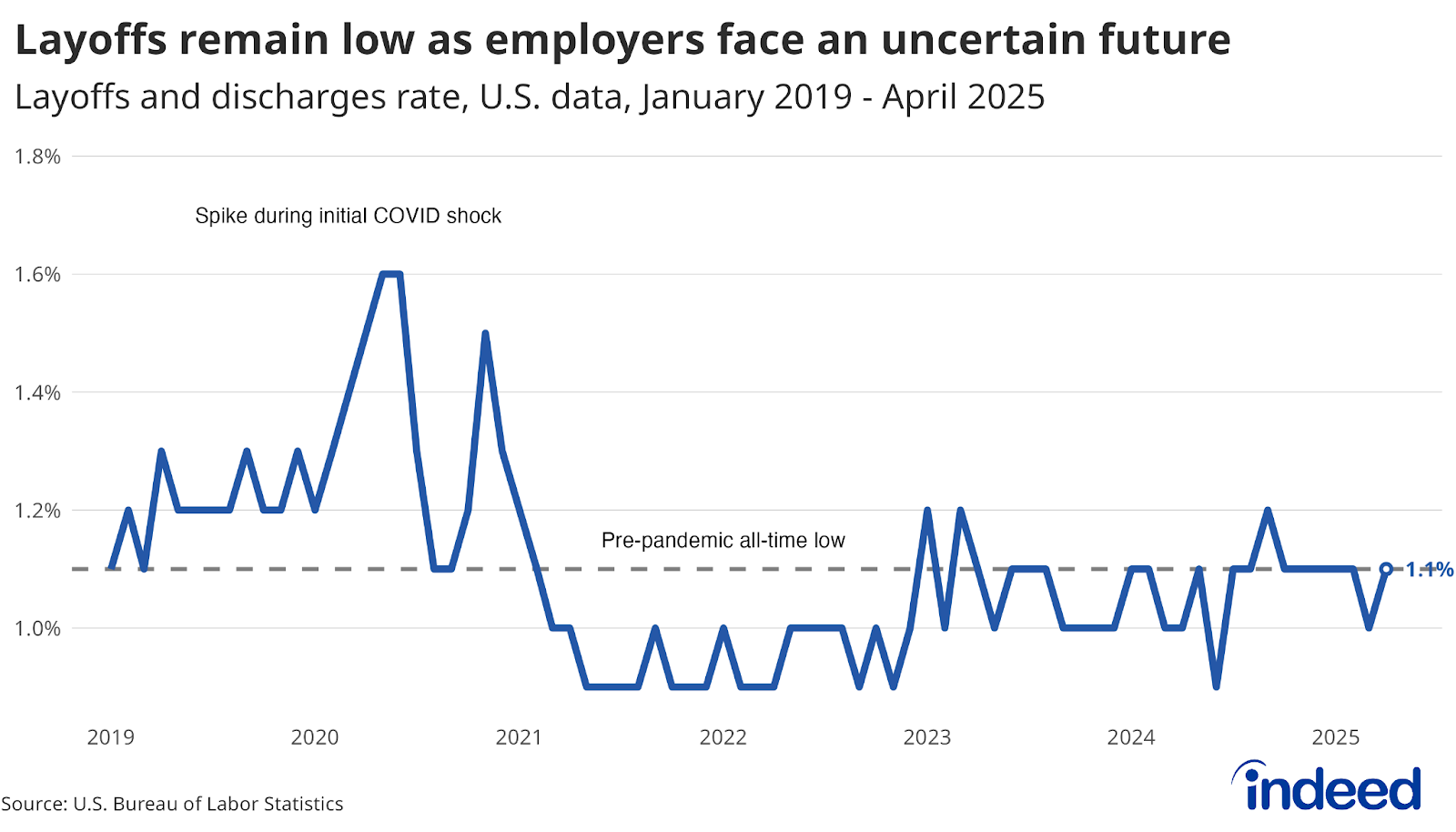

At the same time, businesses are holding tightly to their workers, still feeling the aftershocks of the 2022 employment scramble, when competition for talent was fierce across nearly every sector. Even in industries like information and tech, where job growth has slowed, employers are hesitant to let people go. A low layoff rate usually signals a strong labor market, but not if it’s borne out of hesitation for the future, instead of growth.

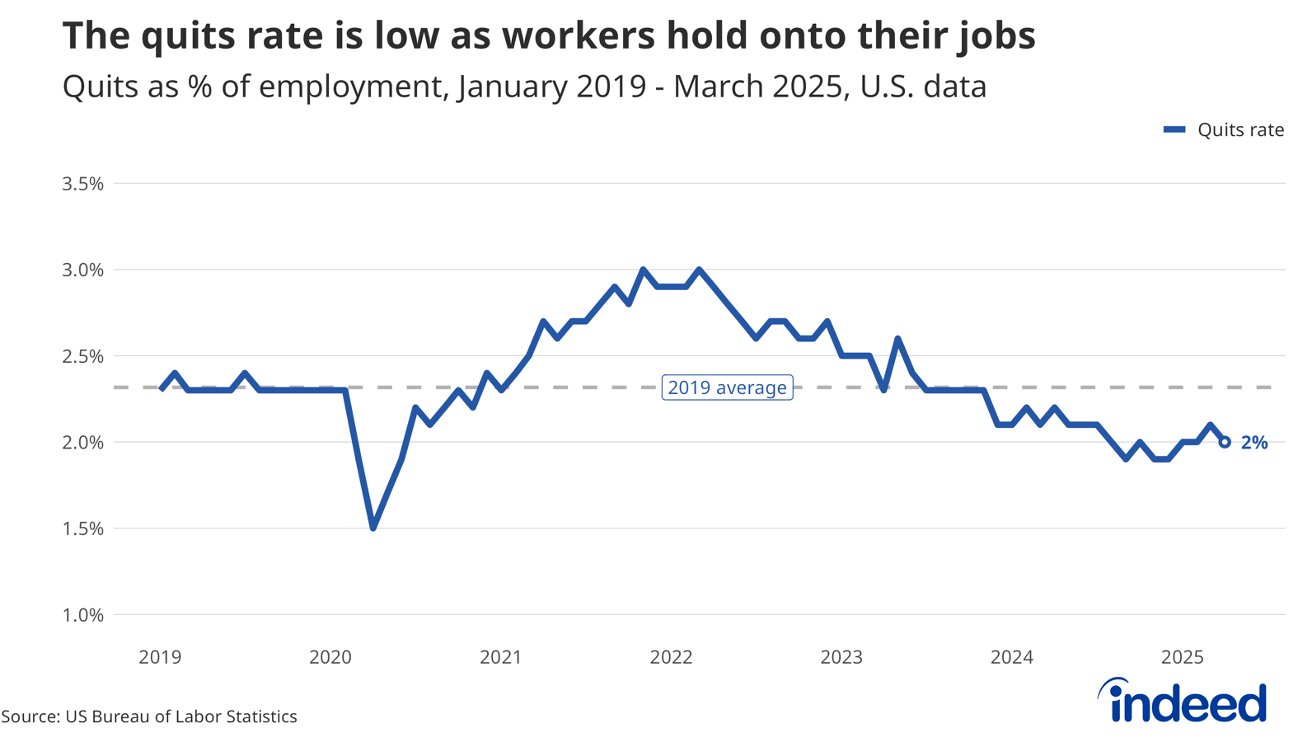

Workers themselves mirror that caution. The quits rate has dropped well below its 2019 average, a sharp contrast to the “Great Resignation” of 2022. One possible explanation is that the flurry of job-switching during that period led to better long-term matches, reducing the need to move again. But the quits rate is also a key barometer of worker confidence, not just in the availability of new opportunities, but also in the security of those roles. Job-to-job transitions not only account for a large portion of hires, but they also make for more efficient matches and increase productivity. Right now, both employers and employees seem to be navigating cautiously, unsure of what’s around the corner, turning our meandering labor market into a stagnant one.

While the major indicators suggest the labor market is sluggish, smaller signals point to underlying erosion. Teenage unemployment — a group typically first to be let go and last to be hired — has been creeping up, and competition for summer jobs in 2025 is fiercer than in recent years. Hiring is also slowing among businesses with fewer than 50 employees, which can often be an early warning sign. Smaller companies tend to delay major decisions during uncertain times, so a drop in their hiring activity may foreshadow broader challenges ahead.

Another important consideration is how the pandemic reshaped our expectations of labor market shifts. The sudden shutdowns of 2020 triggered an unprecedented economic collapse — an outlier even among recessions. What followed was a rapid rebound, driven by surging demand and massive policy responses, setting off a rollercoaster of economic volatility over the past five years. This whiplash may have conditioned many to expect dramatic changes in headline numbers. But economic slowdowns aren’t always so explosive. If you’re waiting for a sharp, unmistakable drop to confirm a weakening labor market, you may be waiting a while. Instead, it’s more useful to look beneath the surface at a range of indicators that, together, offer a clearer picture of where the labor market is really heading.

Conclusion

The data isn’t wrong, but it is nuanced. While headline labor market data continues to suggest strength, a deeper look reveals a more complex and cautious reality. The labor market is no longer growing broadly or robustly; instead, it’s showing signs of stagnation and concerns of erosion. Both employers and employees appear hesitant — holding onto existing roles and avoiding risk amid ongoing uncertainties. The future won’t be defined by dramatic swings, but by more gradual, nuanced shifts. Understanding these subtleties — and looking beyond the surface numbers — will be key to navigating the months ahead.

Methodology

Data on seasonally adjusted Indeed job postings are an index of the number of seasonally adjusted job postings on a given day, using a seven-day trailing average. February 1, 2020, is our pre-pandemic baseline, so the index is set to 100 on that day. We seasonally adjust each series based on historical patterns in 2017, 2018, and 2019. We adopted this methodology in January 2021. Data for several dates in 2021 and 2022 are missing and were interpolated. Non-seasonally adjusted data are calculated in a similar manner, except that the data are not adjusted to historical patterns.

The number of job postings on Indeed.com, whether related to paid or unpaid job solicitations, is not indicative of potential revenue or earnings of Indeed, which comprises a significant percentage of the HR Technology segment of its parent company, Recruit Holdings Co., Ltd. Job posting numbers are provided for information purposes only and should not be viewed as an indicator of the performance of Indeed or Recruit. Please refer to the Recruit Holdings investor relations website and regulatory filings in Japan for more detailed information on revenue generation by Recruit’s HR Technology segment.