Key points:

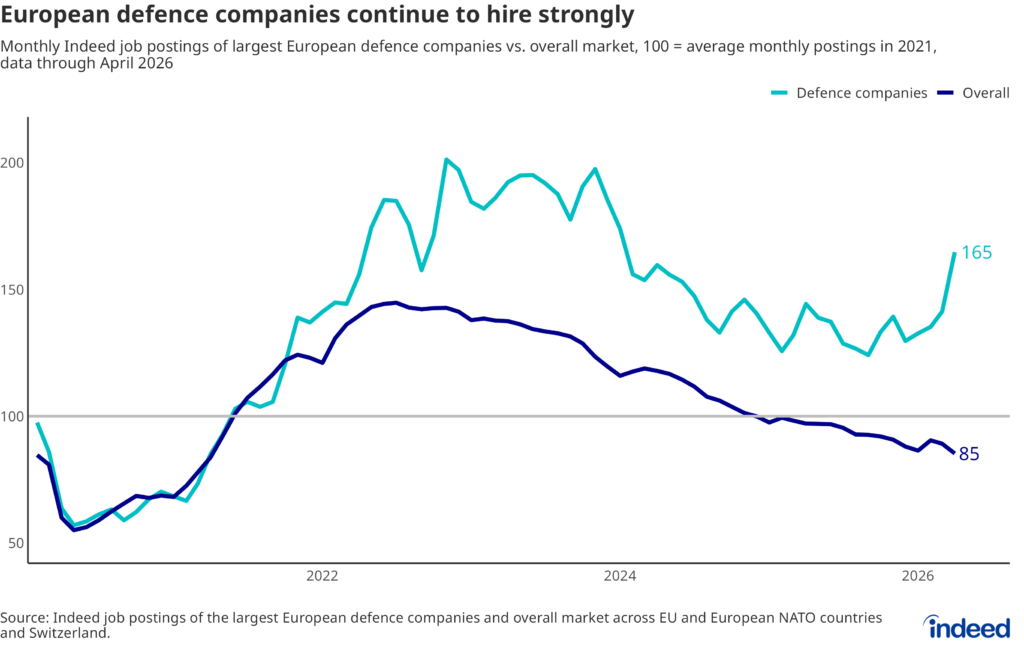

- As of April 2026, job postings at the largest European defence companies stood 65% above their 2021 average, while job postings overall are down 15% over the same period.

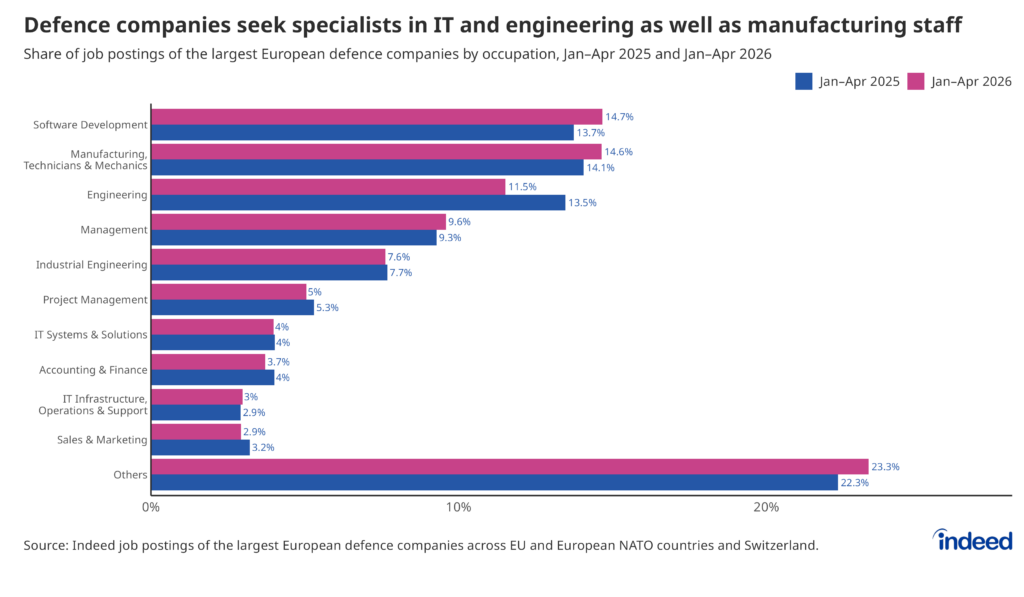

- The occupation mix has remained broadly stable year-on-year; defence companies continue to seek IT and engineering specialists, as well as technical manufacturing workers.

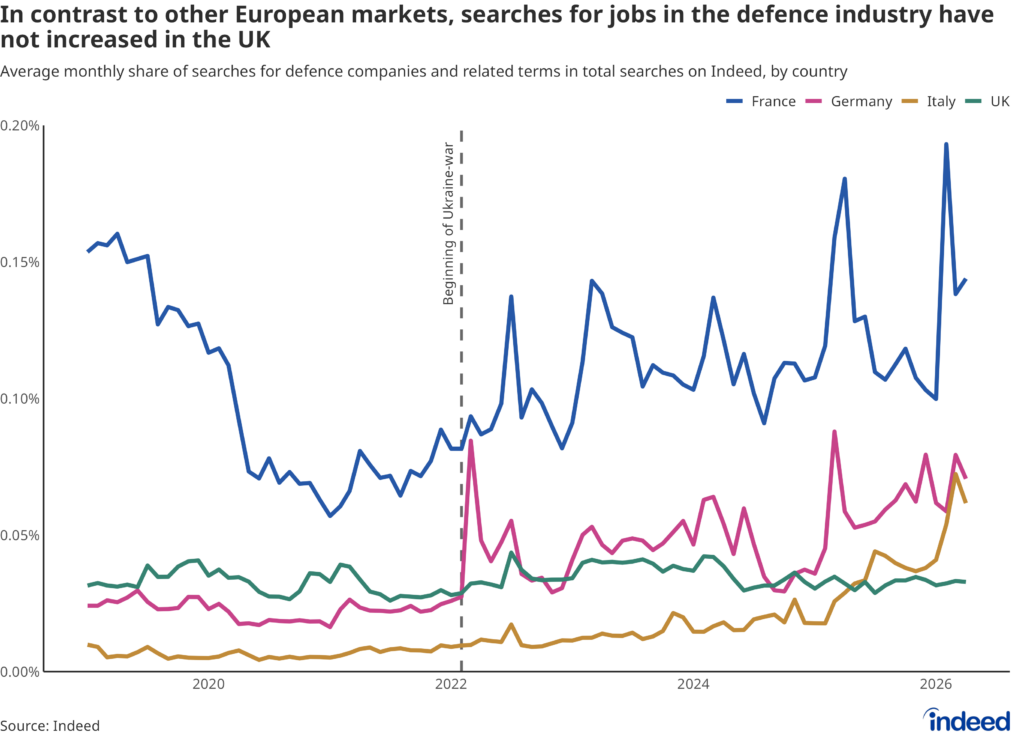

- Job seeker interest in defence roles has continued to grow on the continent, but not in the UK. In April, the share of searches for defence jobs in total searches was more than twice as high in Germany and almost five times higher in France than in the UK.

European governments have significantly increased their defence spending in recent years. The UK’s defence expenditure reached 2.3% of GDP in 2024 and is expected to amount to 2.4% in 2025. EU member states spent 1.9% of their GDP on defence in 2024 and likely spent about 2.1% in 2025, up from 1.6% in 2023. In the longer run, NATO allies have committed to allocating at least 3.5% of their GDP annually by 2035. As a result, the industry’s economic importance has grown. An update of the Hiring Lab Analysis of job postings of the largest European defence companies shows that they continue to seek new employees. As of April 2026, job postings were approximately 65% higher than in 2021.

Job opportunities at European defence companies remain elevated

Beginning in 2022, job postings at Europe’s defence companies decoupled from overall market trends, peaking in 2022 at more than twice the 2021 pre-Ukraine war average and far outpacing overall job posting growth. After falling somewhat in 2023/2024, European defence job postings generally stayed between 25% and 45% above pre-war norms before spiking again at the start of this year. By April 2026, they stood 65% above the 2021 average and were up 14% compared to April 2025. In contrast, the overall market has continued to soften, with total job postings across the EU, Switzerland, and European NATO member states falling 12% over the past year and currently sitting 15% below the 2021 baseline.

The largest share of defence industry job postings (roughly a third, on average, from January to April 2026) is located in France. But France’s share of the defence job pie has been shrinking while other countries have grown; as recently as 2020, some 55% of European defence jobs were in France. Over the same period, the share of European defence jobs in Italy, for example, has grown from just 1% to roughly 13% through the early part of the year. Germany and the United Kingdom each accounted for a relatively stable 20% of job postings throughout the entire observation period.

Help wanted: Software and hardware specialists

Interestingly, the share of defence job postings in software development (14.7%, on average, from January through April) is roughly the same as the share for technical manufacturing staff like machine operators, metalworkers and industrial mechanics (14.6%). Engineering follows, accounting for 11.5% of job postings. However, there is an overlap between some software development and engineering roles; many sought-after profiles lie at the intersection of software and hardware, which is why positions like systems engineers or systems architects often require either an (often electrical) engineering or IT background.

Defence firms are fishing for talent, but UK job seekers aren’t biting

The rise in defence hiring has been matched by an increase in job seeker interest in many European markets. The highest share of defence-related searches (0.144% of all searches in April) is in France, where interest has been volatile but generally growing over the past few years. In Germany, defence-related job searches on Indeed more than tripled at the start of the war in Ukraine and have remained elevated since. Interest in Italy has surged since early 2025, reaching 0.062% in April 2026. But the story is different in the UK. The defence-job search share has generally remained flat over much of the past decade and stood at 0.033% in April 2026. Prior to the pandemic, British job seekers showed somewhat more interest in defence roles than their German and Italian peers. By 2026, that had reversed.

Conclusion

One explanation for the UK’s muted change in search interest may be that the rise in defence spending has been less contentious here than elsewhere on the continent. Defence spending in the UK has been at or above the NATO-agreement recommended threshold of 2% of GDP for several years. But until recently, German defence spending, for example, failed to meet that threshold — it took a controversial reform of its constitutional debt brake to fund increased German defence spending. The political debate surrounding this decision likely increased public awareness of defence spending, potentially driving interest among job seekers as well.

Yet the UK’s broadly stable share of European defence job postings shows that employer demand for defence workers is alive and well. With sustained geopolitical conflicts and defence budgets set to rise further over the coming years, this is unlikely to change. The challenge may therefore shift from funding to staffing: if job seeker interest does not pick up alongside rising budgets, companies could find themselves competing for candidates. To ensure that ambitious spending plans are not hampered by labour supply constraints, defence firms — and perhaps policymakers — may need to invest more actively in raising the profile of careers in the sector.

Methodology

Job Postings

The analysis includes job postings from 25 of the largest European defence companies listed in SIPRI’s Top 100 ranking(two additional European firms in the Top 100 had no data available: JSC Ukrainian Defence Industry and Czechoslovak Group). We capture postings in all EU and European NATO countries, where an Indeed site exists, including the UK, as well as Switzerland. For most companies, relevant postings were identified using Indeed’s proprietary company taxonomy. For a few subsidiaries of larger conglomerates, whose arms sales account for less than 20% of total revenue (Thyssenkrupp Marine Systems, Safran Defence, Airbus Defence and Space), postings were retrieved via keyword-based extraction so as to only capture job postings at the defence-related business units.

The sample includes the following companies: Airbus, Atomic Weapons Establishment, Babcock International, BAE Systems, CEA, Dassault Aviation, Diehl, Fincantieri, Hensoldt, KNDS, Kongsberg, Leonardo, MBDA, Melrose Industries, Naval Group, Navantia, PGZ, Qinetiq, Rheinmetall, Rolls-Royce, Saab, Safran, Serco Group, Thales, ThyssenKrupp.

Search Queries

To measure job seeker interest in the defence industry, we calculated the share of searches on Indeed for the companies included in our sample and for variations of the terms “defence/arms/weapons industry/sector/company” in German, English, French, Italian and Dutch.