Key points:

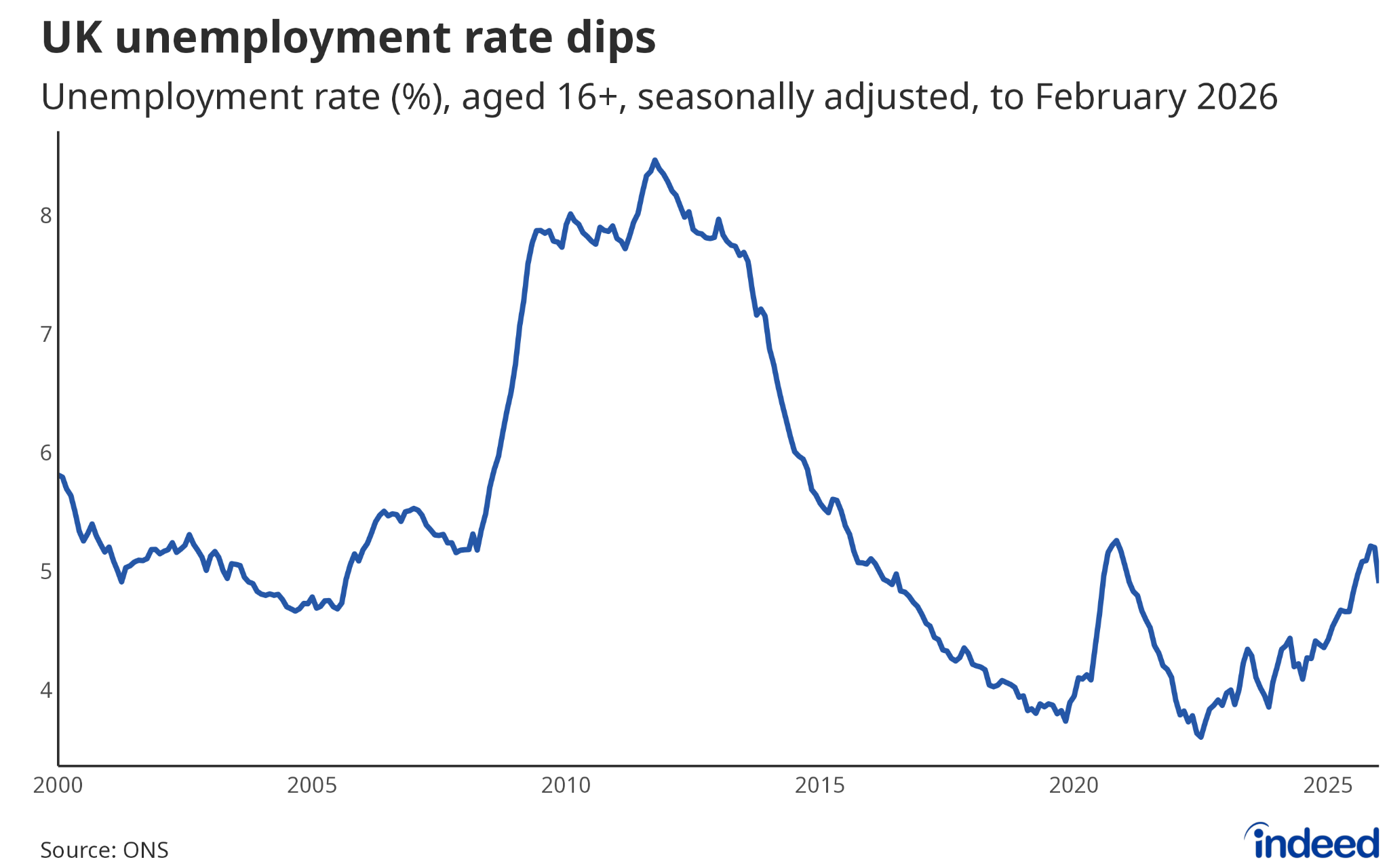

- Unemployment fell from 5.2% in January to 4.9% in February, but the drop was driven almost entirely by a rise in economic inactivity rather than people moving into work.

- Wages grew 3.6% year-on-year, faster than the rate of inflation. But with prices set to rise further on the back of elevated global energy prices, real pay is under threat.

- The Bank of England faces a deepening bind: inflation keeps rate cuts off the table, yet a quietly deteriorating labour market also makes hikes increasingly hard to justify.

A surprise dip in the unemployment rate in the three months to February offered a rare flicker of good news, and it is reassuring that the labour market shows no signs of collapse – but the underlying picture remains one of softness.

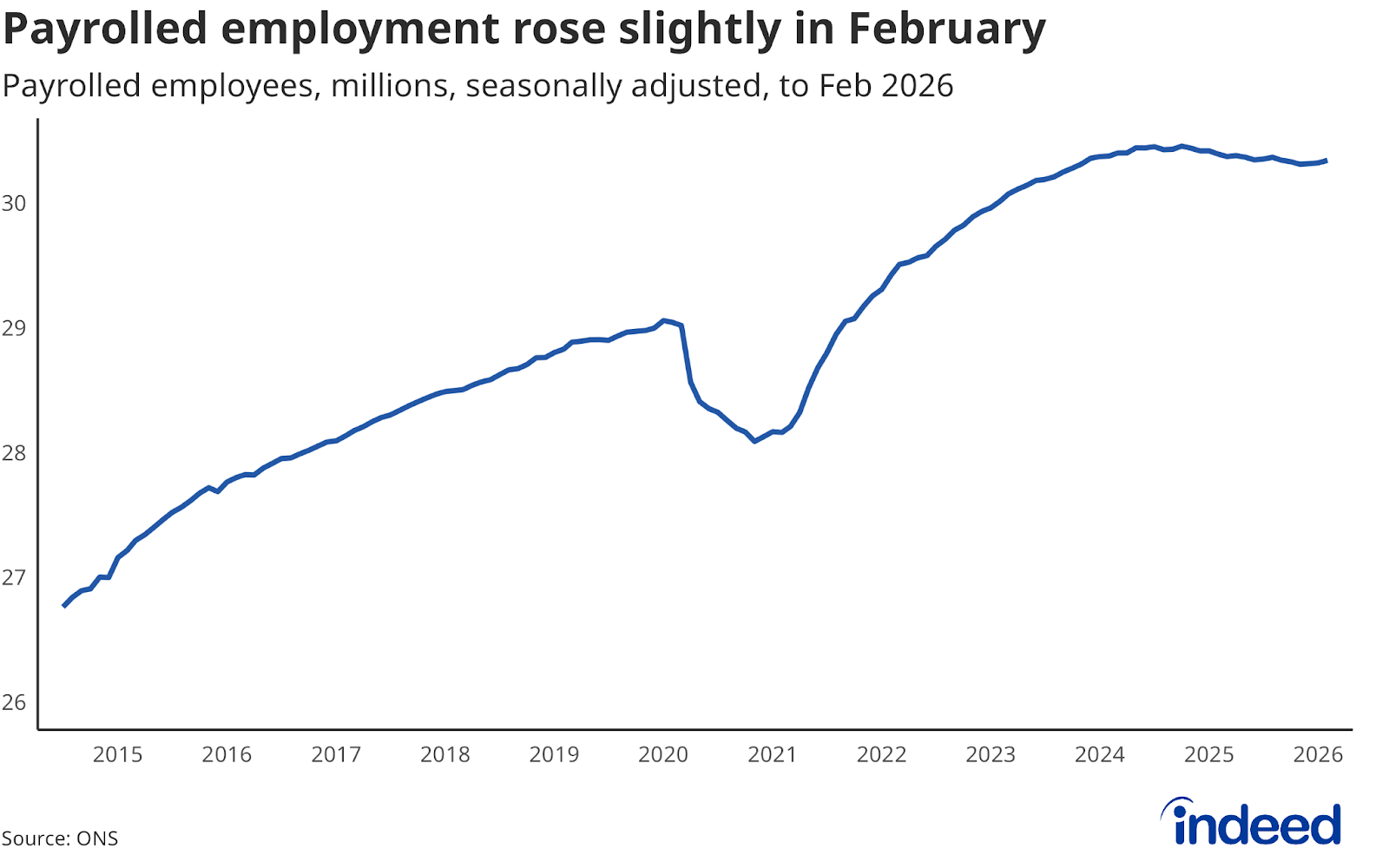

The headline figure, with unemployment falling from 5.2% to 4.9%, looks encouraging at first glance. Dig into the details, however, and a more complicated picture emerges. Employment was little changed over the quarter, meaning the drop wasn’t driven by a big shift of people into work. Instead, the fall in the jobless rate is almost entirely explained by a rise in economic inactivity: people who are neither employed nor actively looking for work. The ONS notes this was particularly visible among students. The headline flatters to deceive.

Wage growth continues to recede. Annual regular pay growth of 3.6% still edges above inflation (which ran at a 3.2% pace over the same period), but not for long. With inflation projected to rise on the back of elevated global energy prices, real pay packets are set to come under renewed pressure.

The sudden increase in energy prices is reminiscent of a similar surge in early 2022, driven by the invasion of Ukraine. But unlike a few years ago, workers are far less well-placed to fight back this time. The labour market was tight during the 2022 energy shock; today, with hiring demand weak and employers holding the whip hand, bargaining power has drained away.

That leaves the Bank of England in an increasingly uncomfortable bind, weighing upside inflation risks against a labour market that is quietly deteriorating. Rate cuts are off the table, but a fragile jobs market makes the case for hikes increasingly hard to sustain.

The deeper concern is that weakness doesn’t just persist, but accelerates. Already soft hiring could give way to more widespread, outright job cutting if businesses buckle under the combined weight of rising costs and deepening economic uncertainty. The floor, for now, is holding. But it bears watching.