Key points

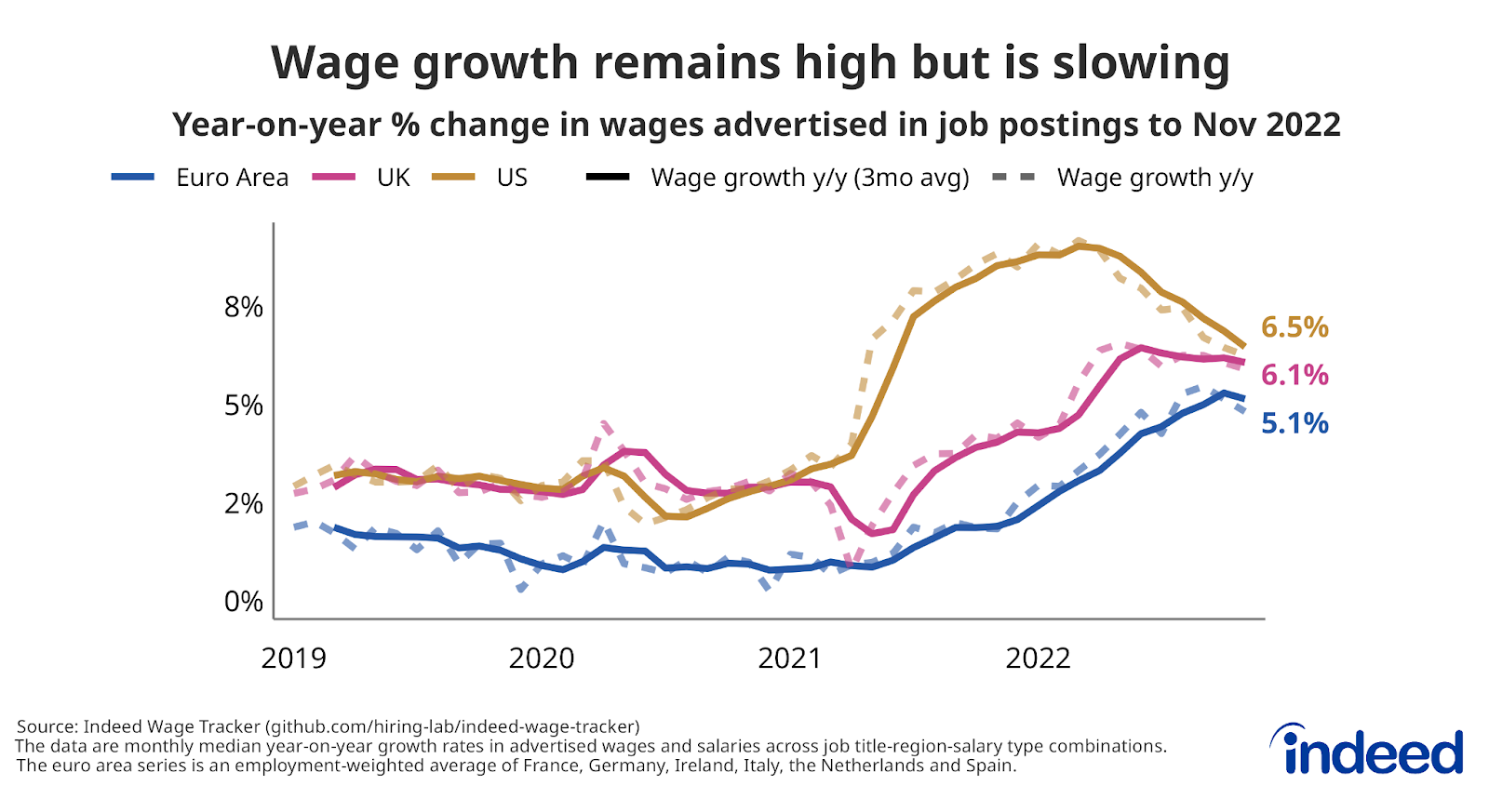

- While growth in wages advertised in Indeed job postings remained high in the euro area and the UK in November, it showed early signs of peaking.

- Average wage growth across the six euro-area countries we track fell from 5.2% year-on-year in October to 5.1% in November, the first decline in 19 months, though it’s too early to tell if this represents a turning point.

- The slowdown was more pronounced in the UK, where wage growth fell from 6.2% to 6.1%, continuing its slide from the peak of 6.4% in June, driven by slowing wage growth in low-paid jobs.

- Wage growth has also slowed considerably in the US, where it fell from 6.9% in October to 6.5% in November, following a peak of 9% in March.

- Slowing wage growth reduces the risk of wage-price spirals, giving central banks more leeway to moderate the pace of interest rate hikes.

The November 2022 Indeed Wage Tracker measures growth in wages and salaries advertised in Indeed job postings in eight advanced economies. This month, for the first time, the US is included in addition to the UK and six euro-area countries which we started tracking in October. Our research paper describes the data and methodology.

Wage growth remains high but is no longer accelerating

In 2022, growth in posted wages in job ads on Indeed accelerated sharply as labour markets in the euro area, UK and US continued their recoveries from the pandemic. Wages grew much faster than in previous years, reflecting tighter labour market conditions.

November data suggest the period of accelerating posted wage growth could be coming to an end. Year-on-year growth in posted wages remained high at 6.1% in the UK, 6.5% in the US, and 5.1% on average across the six euro-area countries we track. But the latest UK and US figures are below their early-2022 peaks of 6.4% and 9%, respectively.

The deceleration is especially noteworthy in the US. Rapid slowdowns in the growth of wages for new hires are not unusual, as we see for job switchers in the Atlanta Fed Wage Growth Tracker during past recessions. To date, our tracker has been a good indicator of trends in the Atlanta Fed data, with a lead time of around three months that reflects lags inherent in the hiring process and the collection of data on job switchers. At the current pace of deceleration, posted US wage growth could return to its pre-pandemic rate of 3-4% by the second half of 2023. Hiring Lab’s US team delves deeper into these trends in an accompanying post.

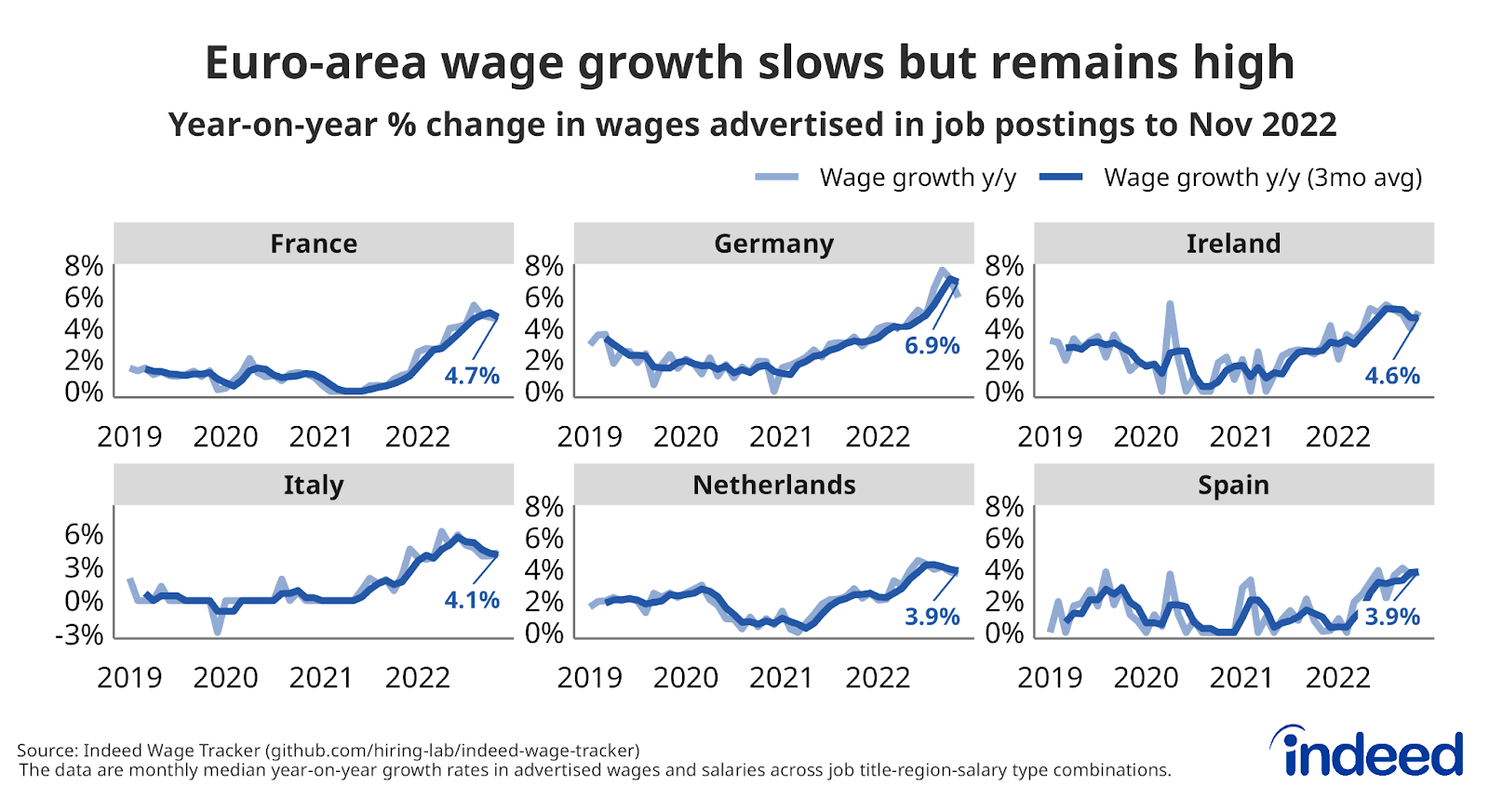

In Europe, average posted wage growth weighted by employment levels in the six euro-area countries we track slowed for the first time in 19 months, from 5.2% in October to 5.1% in November. The slowdown was most apparent in Ireland, Italy and the Netherlands, while France, Germany and Spain held fairly steady. It is too early to say whether this small shift represents a turning point in wage growth.

Does slowing wage growth signal a moderation of wage demands?

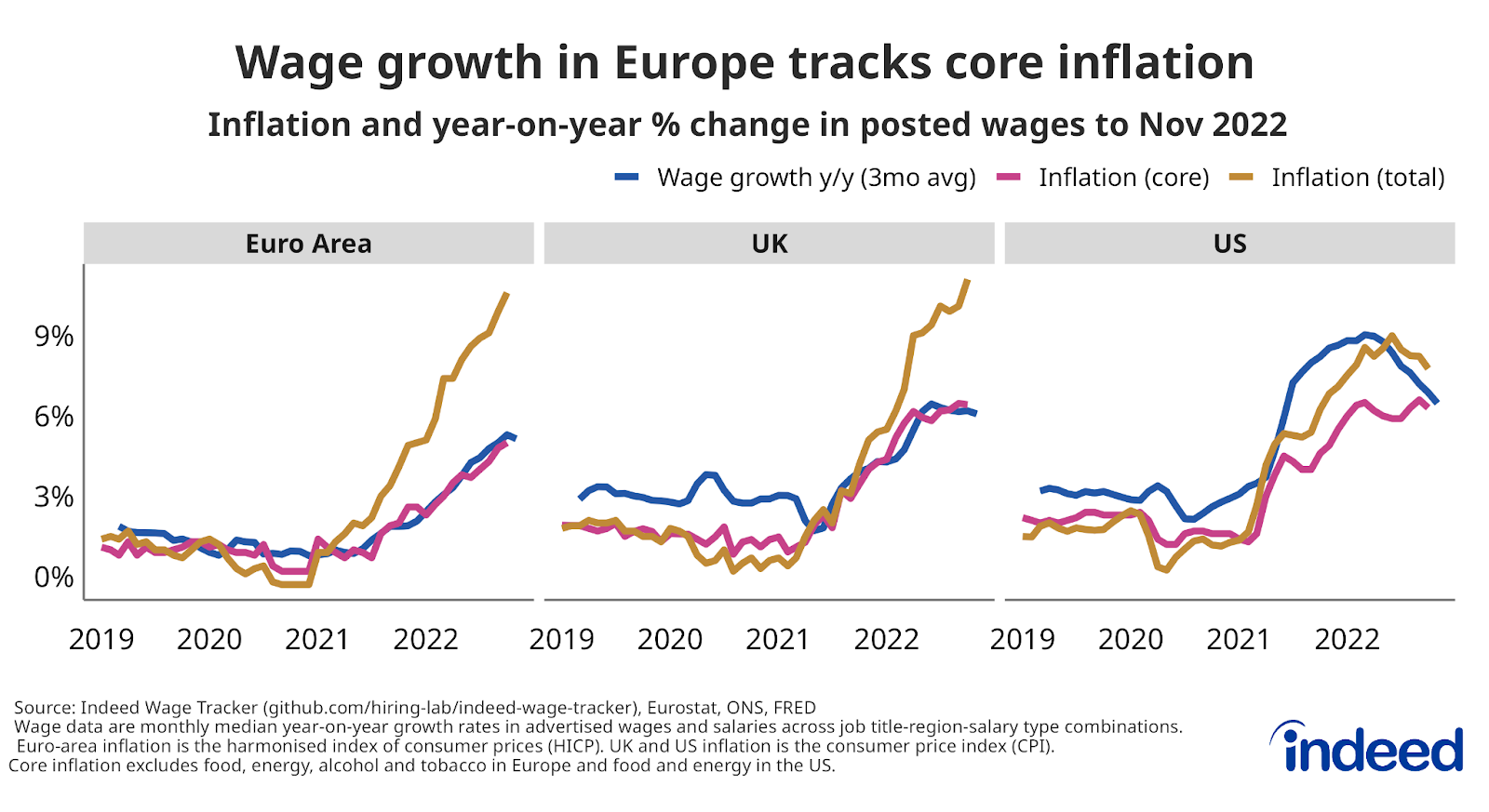

Neither our tracker nor the aggregate employment and unemployment figures have found significant labour market weakening in any of the countries we follow. But wages posted in job ads on Indeed may be significantly forward-looking. Their slowing growth hints the uncertain economic outlook could be starting to weigh on labour markets. That would be consistent with the gradual cooling in job openings and wage growth for job switchers in the US, as well as the slight decline in job vacancy rates in Europe. These trends could lead to a moderation of worker wage demands in 2023, even as inflation remains high.

In addition, European posted wage growth appears to be peaking at a rate well below consumer price inflation. Instead, it is tracking core inflation, which excludes food and energy. In other words, wage increases appear to overlook fast-rising food and energy prices, perhaps because those shocks are perceived to be temporary.

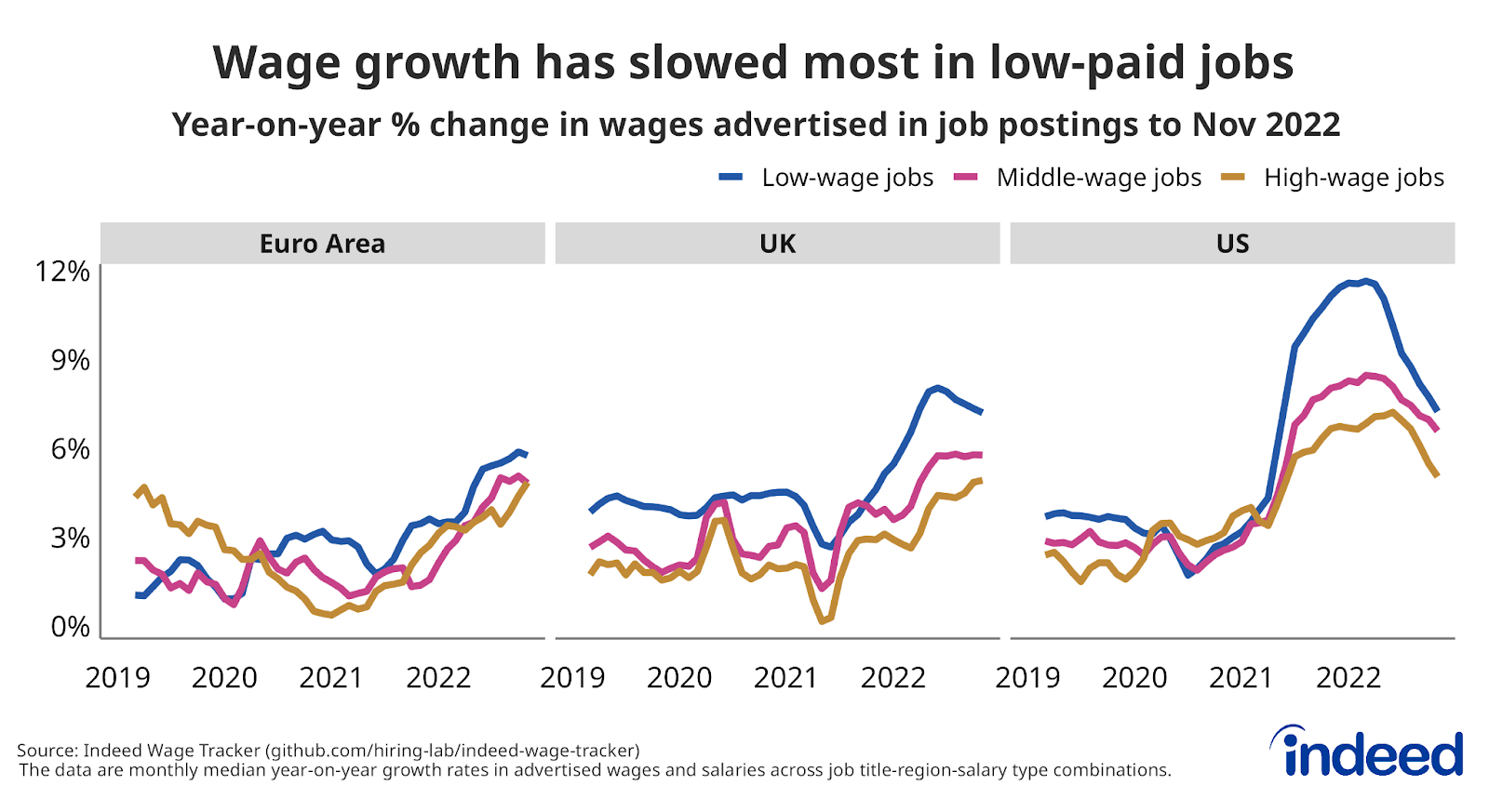

Wages have decelerated most in low-paid jobs

Is the slowdown in posted wage growth confined to a few sectors where labour demand has slackened or is it broad-based? A broad decline would suggest a more widespread impact potentially affecting a larger pool of new hires.

To answer this, we split occupations into three tiers based on their posted wage levels in 2019. Until recently, wages were accelerating most strongly in lower-paid jobs. This was consistent with post-pandemic labour shortages in many non-remote occupations in which face-to-face contact is common and in jobs that tend to be lower-paid. In the past few months though, posted wage growth in the US and the UK has slowed most in these lower-paid jobs. In the US, growth has also come down in middle- and higher-paid jobs, indicating a fairly broad-based decline.

The picture is more mixed in the euro area, where pay gains are still accelerating in high-wage jobs. In contrast, in low-wage jobs, wage growth fell from 5.9% in October to 5.8% in November, while growth for middle-wage jobs fell from 5.1% to 4.8%.

Conclusion

In September and October, wage growth of US job switchers slowed from its post-pandemic highs. The Indeed Wage Tracker suggests this slowdown could continue over the coming months, perhaps signalling pay gains could also moderate for workers staying in their current jobs.

In the euro area and UK, our tracker shows signs post-pandemic wage growth may have peaked, but is not necessarily poised for an imminent decline. It is too early to say with certainty whether we are at a turning point, but slowing posted wage growth in some countries suggests the risk of wage-price spirals is limited.

Methodology

To calculate the average rate of wage growth, we follow an approach similar to the Atlanta Fed US Wage Growth Tracker, but we track jobs, not individuals. We begin by calculating the median posted wage for each country, month, job title, region and salary type (hourly, monthly or annual). Within each country, we then calculate year-on-year wage growth for each job title-region-salary type combination, generating a monthly distribution. Our monthly measure of wage growth for the country is the median of that distribution. Alternative methodologies, such as the regression-based approaches in Marinescu & Wolthoff (2020) and Haefke et al. (2013) produce similar trends.

More information about the data and methodology, as well as additional country-specific wage growth results, are available in our accompanying research paper, ‘Wage growth in Europe: evidence from job ads’, published in the Central Bank of Ireland’s Economic Letter series.