Key points:

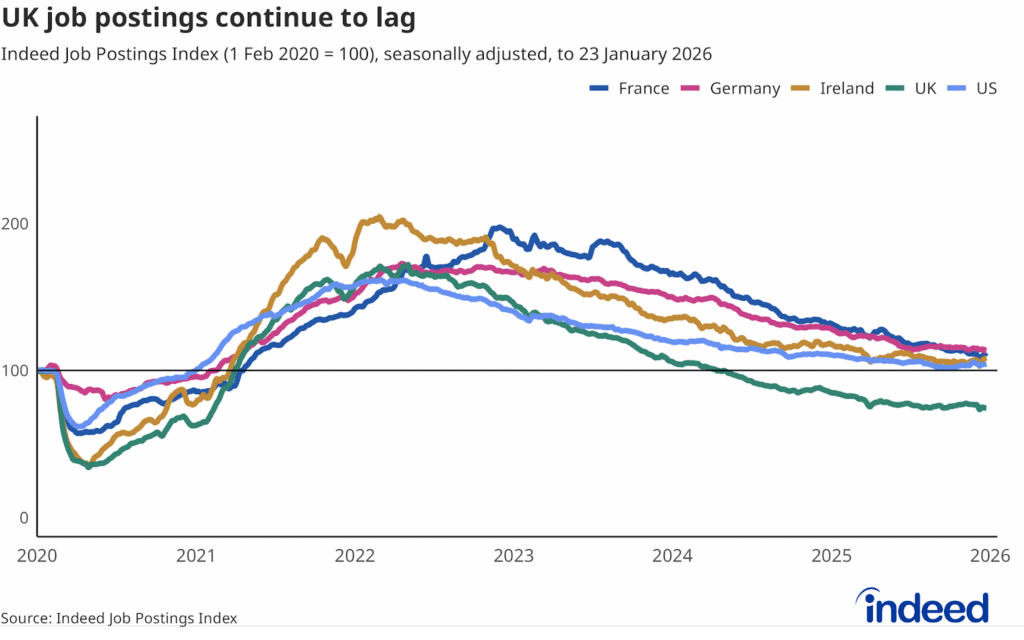

- UK job postings continued to gradually soften into early 2026 and stand more than 25% below their pre-pandemic baseline.

- The cooling labour market is belatedly translating into a meaningful deceleration in posted wage growth – significant for Bank of England policymakers.

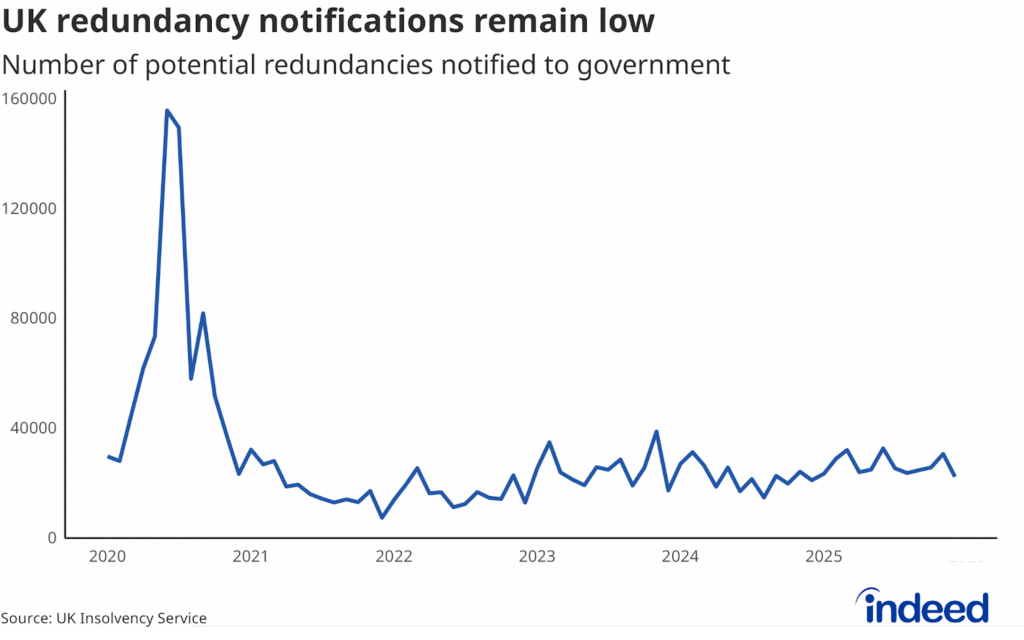

- Sustained weakness in hiring is showing up in rising unemployment, though low redundancy notifications suggest no imminent spike in job losses.

Our Labour Market Updates examine important trends using Indeed and other labour market data. Our European Labour Market Overview chartbook provides a more comprehensive view of the European labour market. Other data, including the Indeed Wage Tracker, is regularly updated and can be accessed on our data portal.

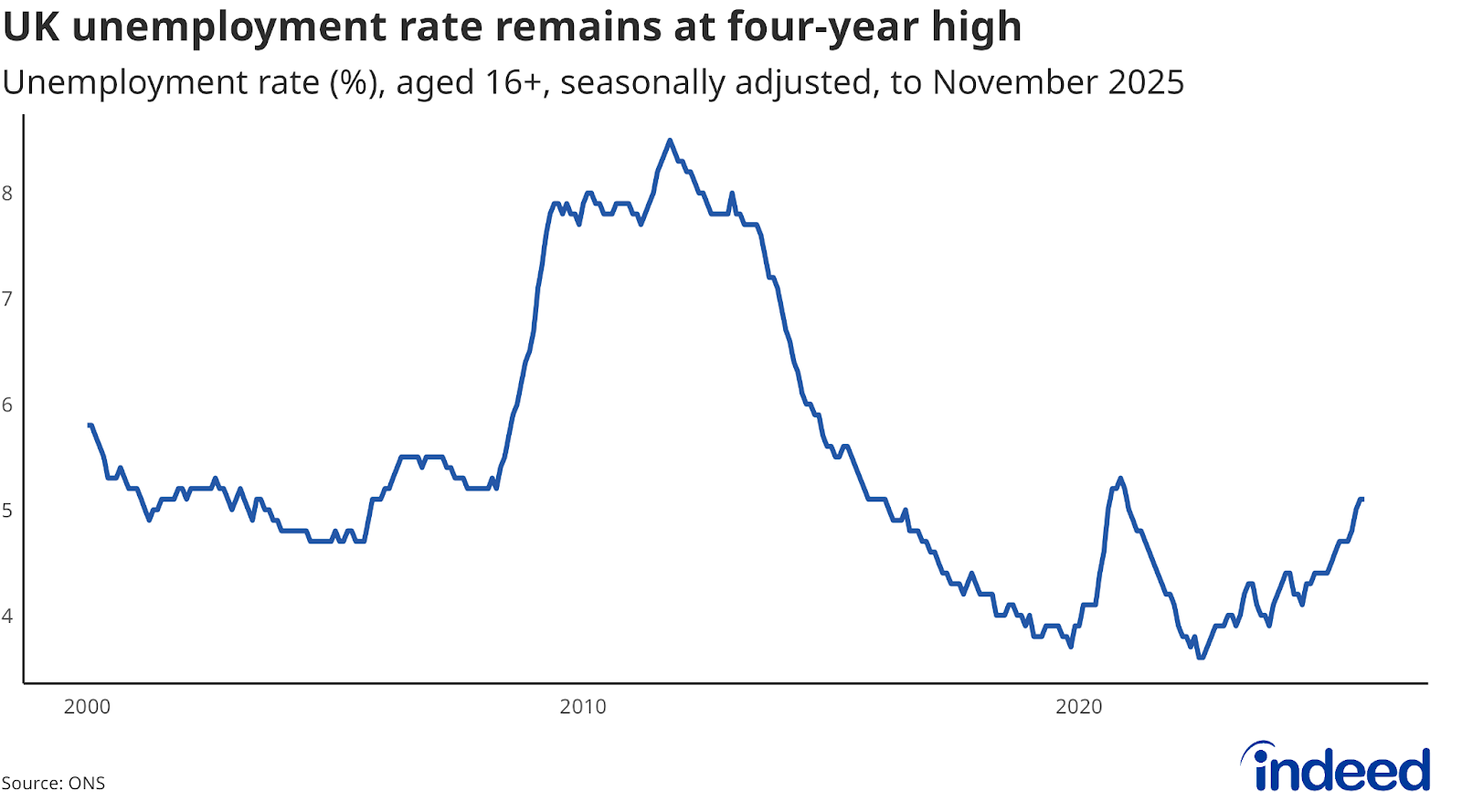

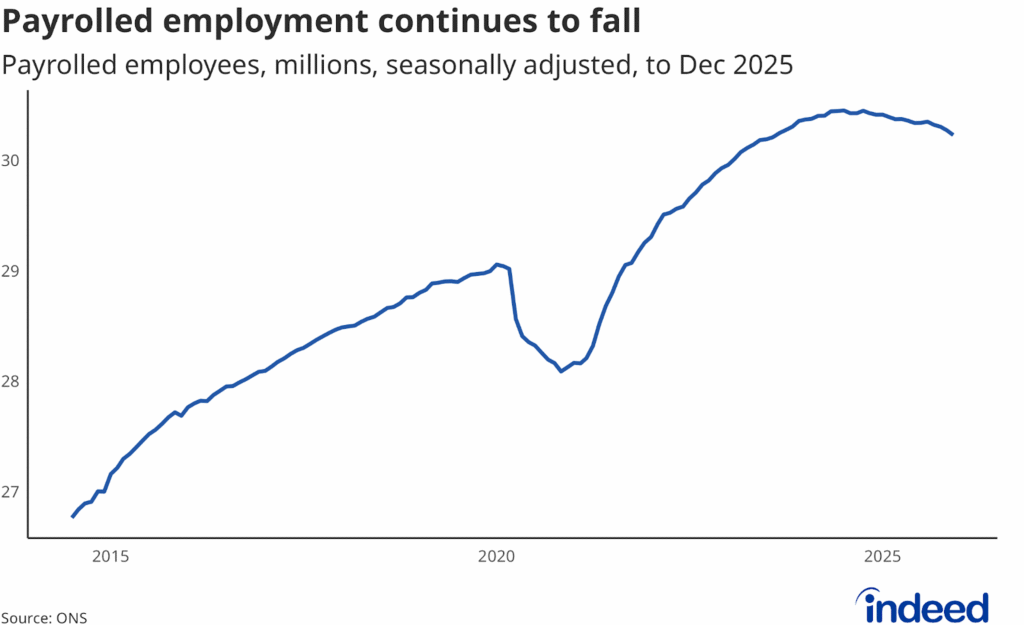

One month into 2026, the UK labour market continues to soften amid persistently weak hiring demand. Job postings aren’t crashing but have continued to gently decline in recent weeks. Payrolled employment has continued to fall and the jobless rate has hit a four-year high, though there remains little sign of an impending marked uptick in layoffs – a continuation of the established low-hiring, low-firing pattern.

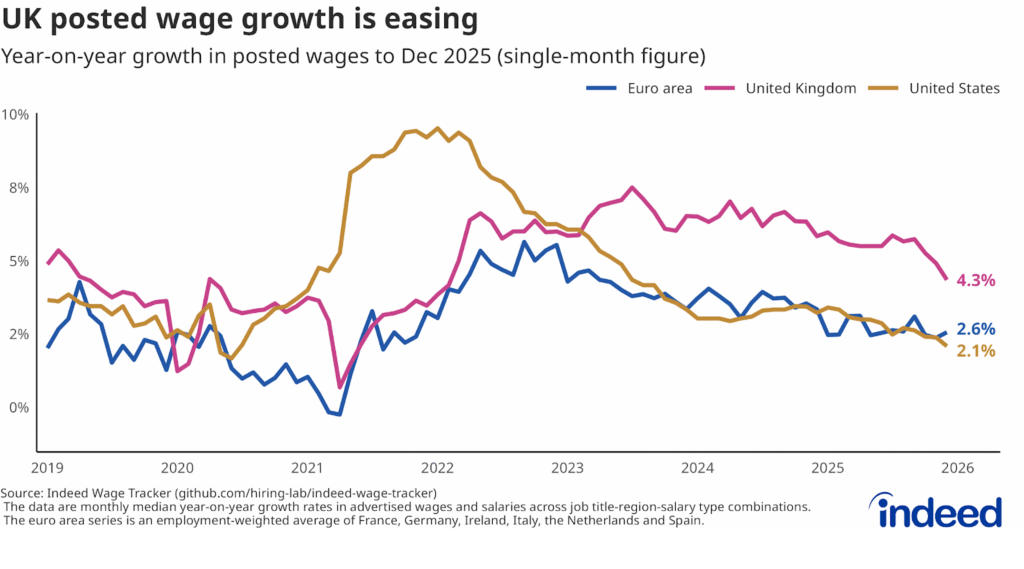

Pay pressures are finally reflecting the underlying weakness of hiring demand. Robust wage growth in the UK has been an outlier among other advanced economies for some time, but that’s beginning to change. A sustained fall in wage growth may help persuade policymakers at the Bank of England that risks of inflation persistence are dissipating, tipping the balance in favour of further interest rate cuts intended to support the economy.

Spotlight: Slowing wage growth

For the past three years, the UK labour market has been characterised by persistently high wage growth. That’s been in contrast to both the slowing seen in other countries and the UK’s own comparatively weak hiring demand. Policy changes, including large increases to the country’s minimum wage, have contributed to some of the robust pay growth, though part of the strength has been a puzzle.

While wage growth remains above levels consistent with sustainably on-target inflation (wage growth closer to 3% is generally thought of as consistent with 2% inflation), the recent trajectory of wage gains suggests a decisive shift. Annual UK wage growth as measured by the Indeed Wage Tracker slowed to 4.3% in December, its lowest since early-2022 and down sharply from 5.7% just three months prior.

That echoes official labour market data, which showed average earnings growth easing to 4.5% in the three months to November. Significantly, private sector wage growth – closely watched by monetary policymakers – dropped to 3.9%, its lowest in almost five years.

The Bank of England’s interest rate-setting committee has been divided in recent months between inflation risks and worries over soft growth and a weak labour market. It narrowly voted to lower rates by 25 basis points to 3.75% in December, and economists are split on whether it will follow up with another rate cut in Q1. If wage growth continues to come down, that could be enough to allay the concerns of the more hawkish members of the committee and tip the balance in favour of further rate cuts.

Hiring appetite remains weak

UK job postings remain weak and continued to gradually decline in January. As of 23 January, postings had fallen 3.1% from a month prior and stood around 26% below their pre-pandemic baseline. Measures of employer confidence remain muted, though improved slightly following the Chancellor’s Autumn Budget.

Weakness in low-paid occupations remains a striking feature of the UK job postings landscape. Job-postings for low-wage categories are trending below that for high-paid jobs, in contrast to other European countries, including France, Germany and Ireland, underlining the impact on low-wage sectors following the Chancellor’s tax hike in late-2024.

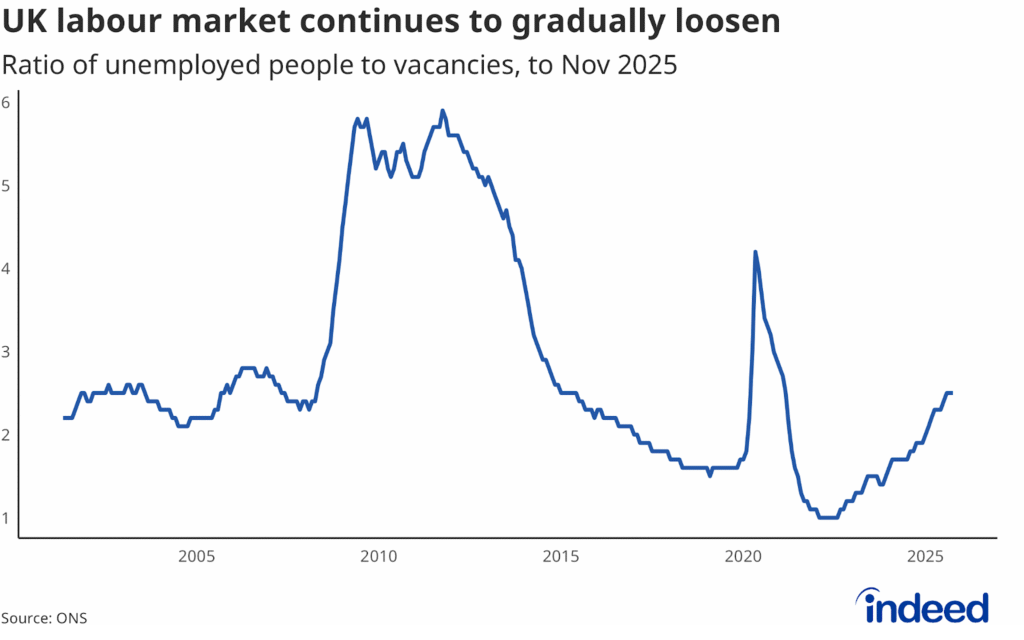

Loosening labour market

The latest Office for National Statistics figures point to an ongoing softening of the UK labour market, with payrolled employment falling further and the unemployment rate standing at a joint four-and-a-half-year high.

Vacancies have been broadly stable in recent months but remain well down from peaks. Combined with higher unemployment, that means there are now 2.5 unemployed people for every vacancy, up from a low of 1 in 2022 and higher than pre-COVID norms.

Redundancy notifications, meanwhile, have remained modest in recent months, suggesting unemployment isn’t likely to spike higher soon.

Conclusion

The UK labour market is loosening gradually rather than sharply deteriorating. Hiring demand remains weak, wage pressures are easing and unemployment has risen, but the absence of widespread layoffs means conditions are unlikely to shift suddenly in either direction.

For recruiters, this points to a market where candidate availability is improving at the margin, particularly in lower-paid and entry-level roles. With wage growth slowing, employers may find slightly more room to manoeuvre on pay.

With other factors beyond pay also important to candidates, firms that can move decisively, communicate clearly and offer stability will be best placed to secure talent – especially while broader confidence in the economic outlook remains fragile.

Hiring Lab Data

Job postings data is available on our Data Portal. We also host the underlying job-postings chart data on GitHub as downloadable CSV files. Typically, it will be updated with the latest data one day after this blog post is published.

Methodology

Data on seasonally adjusted Indeed job postings are an index of the number of seasonally adjusted job postings on a given day, using a seven-day trailing average. Feb. 1, 2020, is our pre-pandemic baseline, so the index is set to 100 on that day.

To calculate the average rate of wage growth, we follow an approach similar to the Atlanta Fed US Wage Growth Tracker, but we track jobs, not individuals. We begin by calculating the median posted wage for each country, month, job title, region and salary type (hourly, monthly or annual). Within each country, we then calculate year-on-year wage growth for each job title-region-salary type combination, generating a monthly distribution. Our monthly measure of wage growth for the country is the median of that distribution.

The number of job postings on Indeed.com, whether related to paid or unpaid job solicitations, is not indicative of potential revenue or earnings of Indeed, which comprises a significant percentage of the HR Technology segment of its parent company, Recruit Holdings Co., Ltd. Job posting numbers are provided for information purposes only and should not be viewed as an indicator of performance of Indeed or Recruit. Please refer to the Recruit Holdings investor relations website and regulatory filings in Japan for more detailed information on revenue generation by Recruit’s HR Technology segment.