Key points:

- Employment growth has been solid throughout the first three months of 2026, outpacing last year’s sluggish growth.

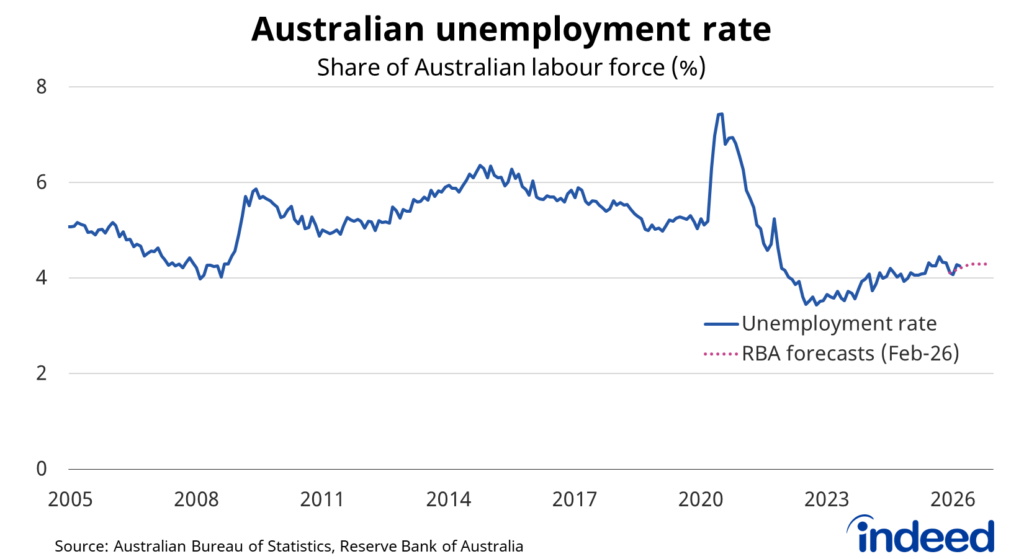

- Australia’s unemployment rate held steady in March, at 4.3%, although it feels like the calm before the storm.

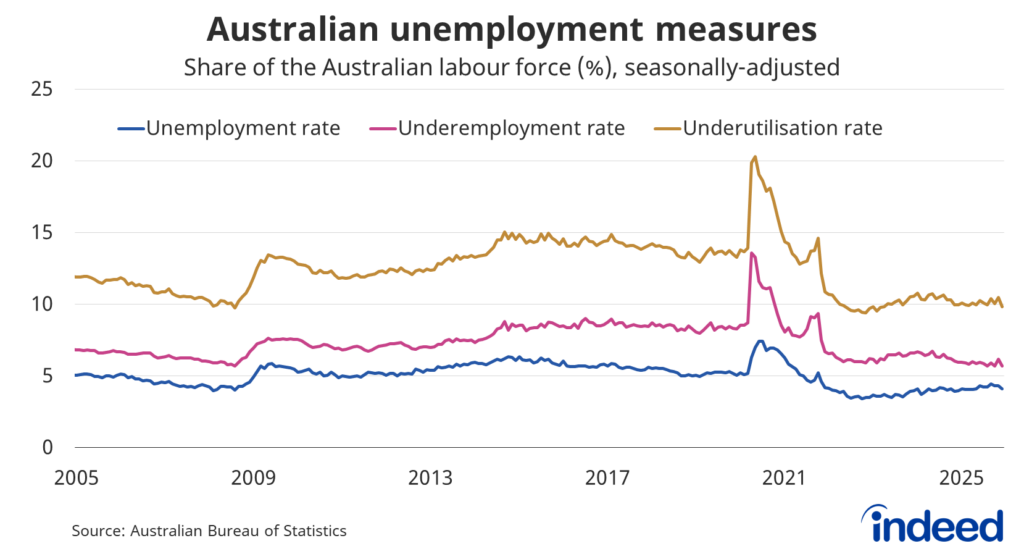

- Broader measures of labour market conditions, such as the underemployment and underutilisation rates, remain much stronger than their long-term average.

Australian employment rose by 17,900 people in March, broadly in line with market expectations, while the unemployment rate remained at 4.3%.

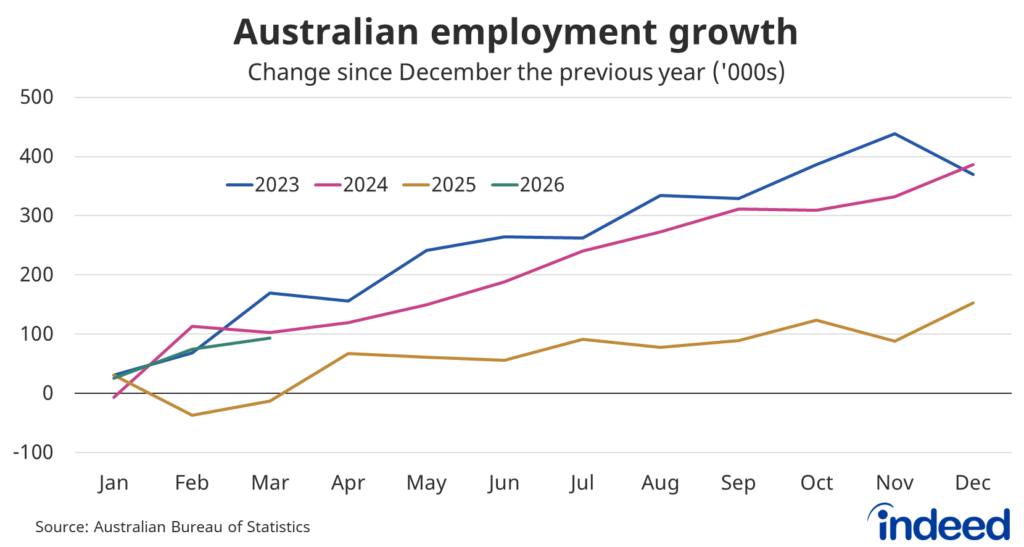

Employment growth this year has actually been quite good, climbing by around 93,000 people since the end of last year. Though that’s much improved over the sluggish growth seen last year over the same time period, that momentum will be difficult to continue if the global economic outlook continues to sour.

Australia’s job market is still tight

Australia’s unemployment rate remained at 4.3% in March and, outside of a brief dip, we’ve essentially remained at this level since June last year. Labour market conditions remain somewhat tight, contributing to ongoing wage and inflationary pressures. The latest forecasts from the Reserve Bank of Australia (RBA), published in February, indicated that the unemployment rate would remain at 4.3% until the end of the year.

Obviously, those forecasts will now be revised up in response to changes in the economic outlook. We expect the unemployment rate to drift higher over the remainder of the year, pushing above 4.5%.

Broader measures of labour market conditions remain healthy. Australia’s underemployment rate was 5.9% (2 percentage points below its 2010-2019 average), with the underutilisation rate ticking up slightly to 10.2% (3.2 percentage points below average). This highlights how tight the job market continues to be.

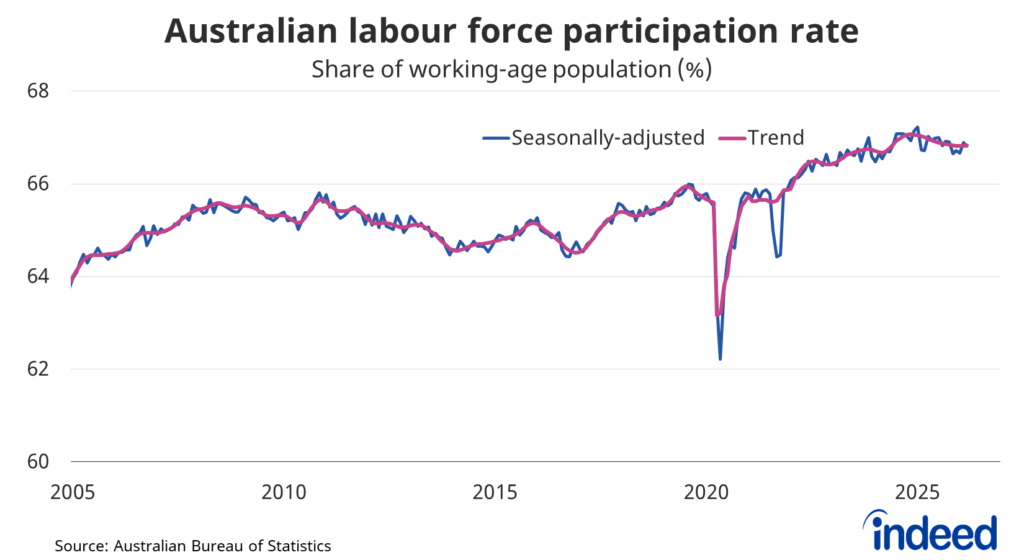

Participation rate fell in March, but should remain high in the near term

Australia’s participation rate eased slightly in March to 66.8%, from 66.9% last month. Renewed cost-of-living pressures may push participation higher in the near term, as households seek more work and, in some cases, another income source. This will help offset the ongoing drag of Australia’s ageing population, much as it has over the past few years.

Assessment and implications

Australia’s job market has proved remarkably resilient in recent years, but another series of rate hikes, along with global supply-chain disruptions, will test that resilience. It’s still too early to see any impact from this, even in more timely measures of labour demand such as Indeed’s job postings. Still, businesses are certainly feeling the pressure, with NAB business confidence collapsing in March.

The latest labour market figures, by being uneventful in March, won’t be a major discussion point when the RBA meets in early May. Instead, discussions on inflation and the ongoing conflict in the Middle East will dominate that meeting. In truth, there isn’t much the RBA can do about overseas supply-chain disruptions and a surge in petrol prices. However, even ignoring that, they face broad-based, domestically driven inflationary pressures that still need to be addressed.

Some of that excess demand will be addressed via slower economic growth, and the RBA will obviously know that. The key question, though, is whether that’s sufficient to bring persistently high service sector inflation to a level consistent with the RBA’s inflation target. We expect the RBA to decide in May that their job isn’t yet done and to increase the cash rate by another 25 basis points.