Key Points:

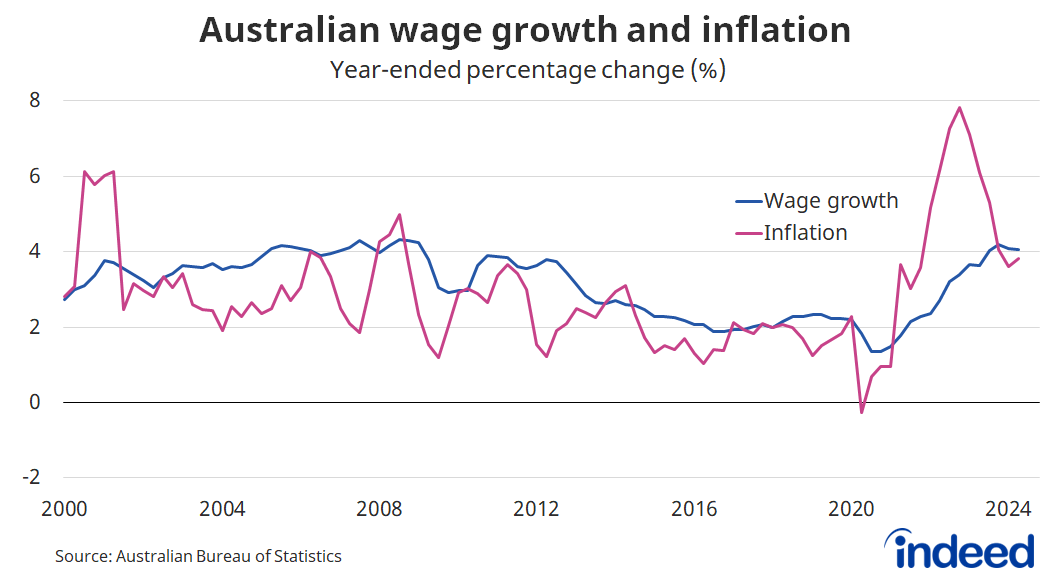

- Australian wages rose 4.1% over the past year, outpacing the 3.8% rise in consumer prices.

- Wage growth has been highest in the healthcare & social assistance industry, ahead of utilities and education.

- High wage growth has been difficult to justify based on Australia’s productivity performance, creating a headache for the Reserve Bank of Australia (RBA).

Australian wage growth rose 0.8% in the June quarter – falling short of market expectations – but still 4.1% higher than a year ago. Private sector wages rose by just 0.7% in the June quarter, compared to a gain of 0.9% in the public sector. Those public sector gains were higher than usual due to the recent synchronisation of Commonwealth public sector agreements, which caused gains to be more concentrated than usual in the June quarter.

Annual wage growth will likely fall sharply in the September quarter, as the historically strong growth from last year’s September quarter drops out of the annual figure. This could cause annual wage growth to drop into the 3.5% range, well below current levels.

Wage growth varies considerably across industries and by region. Over the past year, wage growth has been highest in healthcare & social assistance (5%), ahead of utilities (4.3%) and education (4.3%). In fact, wage gains over the past year have been above 3% in every industry. At the state level, annual wage growth was highest in Tasmania at 5.1% and lowest in Victoria at 3.3%.

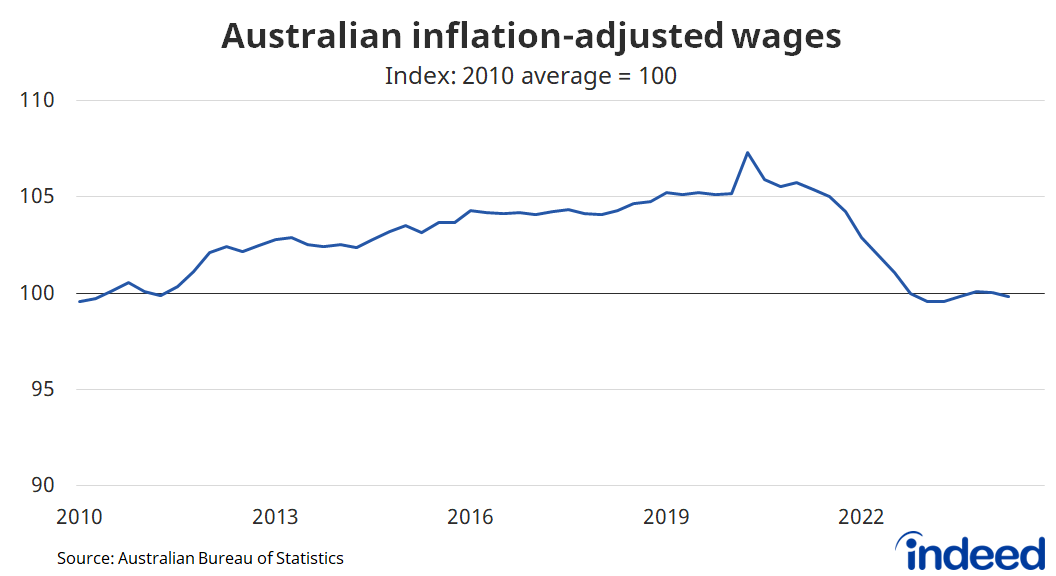

Over the past year, Australian wage growth has outpaced the 3.8% increase in consumer prices. Nevertheless, inflation-adjusted wages are still down 7% from their peak, and at levels last seen around 14 years ago. While wage growth should exceed inflation quite comfortably throughout 2024, a full wage recovery may take up to five years, or even longer.

Newly negotiated wages

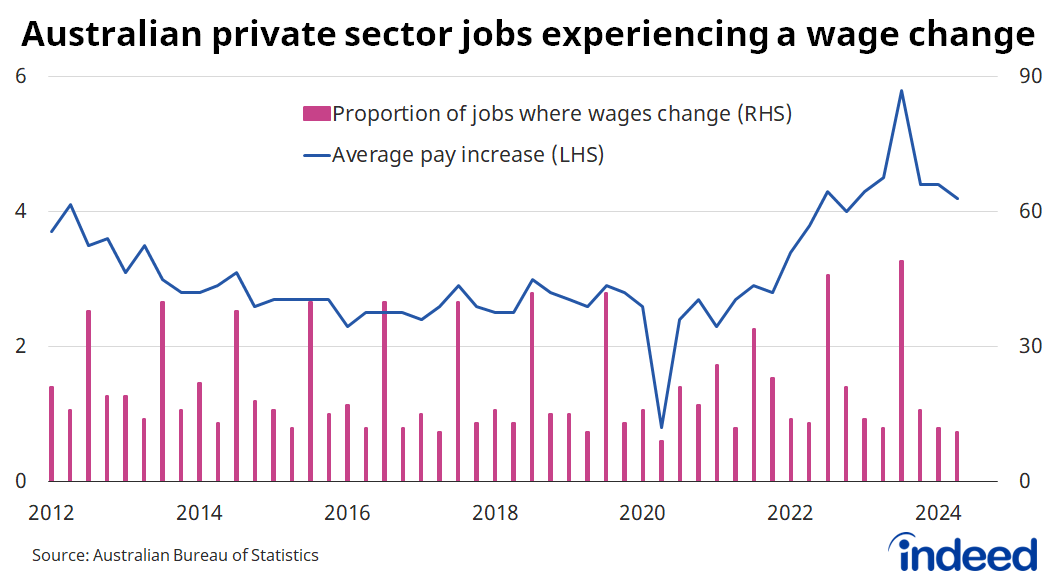

Australian wage growth is driven partly by the size of the change in wages, and partly by the share of jobs where wages changed. In the June quarter, wages changed in 11% of Australian private sector jobs, and the average increase across those jobs was 4.2%. By comparison, wages changed in 19% of public sector jobs, with an average increase of 3.8%.

Newly negotiated wage growth is a useful indicator of where wage pressures are strongest, as well as the type of wage gains that workers can anticipate. In the June quarter, 67% of jobs have received wage gains of 3% or higher over the past year, compared to 53% of jobs over the same period a year ago.

Assessment and implications

While the Australian labour market remains tight, we continue to see signs of cooling, and the latest wage growth figures are consistent with that trend. That wage growth is softening should come as little surprise given Australia’s pitiful productivity performance as of late. Strong wage growth, while certainly welcome for households, was hard to justify on a productivity basis, and arguably unsustainable going forward.

In fact, the disconnect between wage growth and productivity growth remains one of the biggest challenges for the RBA. It may not stop inflation from returning to the RBA’s 2-3% inflation target, but it will be pivotal in determining whether inflation stays there. Ideally, you’d want to see productivity growth improve significantly and quickly to ensure that the eventual correction doesn’t take place via a big reduction in wage growth.